Suz-Anne Kinney

Suz-Anne Kinney

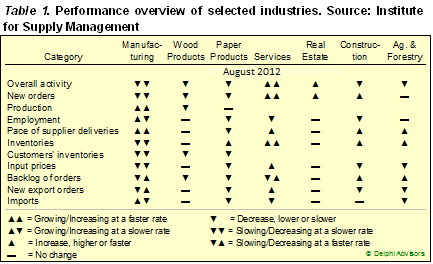

In August, ISM’s PMI ticked down to 49.6 percent, from 49.8 in July (50 percent is the breakpoint between contraction and expansion). Bradley Holcomb, chair of ISM’s Manufacturing Business Survey Committee, concluded with, “Comments from the [respondent] panel generally reflect a slowdown in orders and demand, with continuing concern over the uncertain state of global economies.” The mix among the sub-indices was also disheartening, as new orders, new export orders and order backlogs shrank in the face of rising producer inventories and input prices (Table 1). Interestingly, ISM reported expanding hiring for the manufacturing sector.

By contrast, the service sector grew at a faster clip in August, reflected by a 1.1 percentage point rise (to 53.7 percent) in the non-manufacturing index. Comments by Anthony Nieves, chair of ISM’s Non-manufacturing Business Survey Committee, were almost identical to Holcomb’s. “Respondents’ comments continue to be mixed,” said Nieves, “and for the most part reflect uncertainty about business conditions and the economy.” The mix of service sub-indices was somewhat more upbeat; at least new orders, order backlogs and new export orders increased (even if, as in some cases, only barely); however, the proportion of firms facing higher input prices rose dramatically.

Wood Products remained unchanged in August, with the good news of shrinking customer inventories offset by rising imports. Paper Products expanded, but some clouds may be on the horizon from falling new orders, new export orders and order backlogs; some of that bad news may be mitigated by declining imports. Real Estate and Ag & Forestry both reported expansion in overall activity, thanks primarily to new orders. Construction, by contrast, is facing an uphill battle from falling new orders and shrinking order backlogs.