2 min read

While some forest products companies still maintain a land base, large integrated pulp and paper companies owning a significant land base in order to secure a portion of their raw material is largely a business model whose time has passed. One can argue whether this is a positive or negative change, but this reality has dramatically altered the way wood products companies source their raw materials; it has also created opportunities for improving supply chain efficiencies and profitability.

When forest products companies began to divest themselves of timberlands—and in turn, their access to on-demand timber—it created a new operating environment for securing wood fiber in the Great Lakes. As the integrated land base model is now passé, wood products companies have essentially been left with two primary methods for securing wood fiber: they either hold it contractually, or they hold it in the form of inventory.

To gain dependable access to fiber, mills can rely on four primary methods of obtaining secured wood:

- Stumpage from Non-Industrial Private Forests (NIPF)

- Supply Agreements

- Long-term Contracts

- Landowner Assistance Programs

In the Great Lakes region, weather can significantly impact wood flows, which in turn affect mill operations. Mills must account for this normal variation in the weather and adequately plan for rolling minimum and maximum inventory targets. To plan effectively, mills in the region can alter their strategies to better achieve minimum and maximum inventories at critical times of the year.

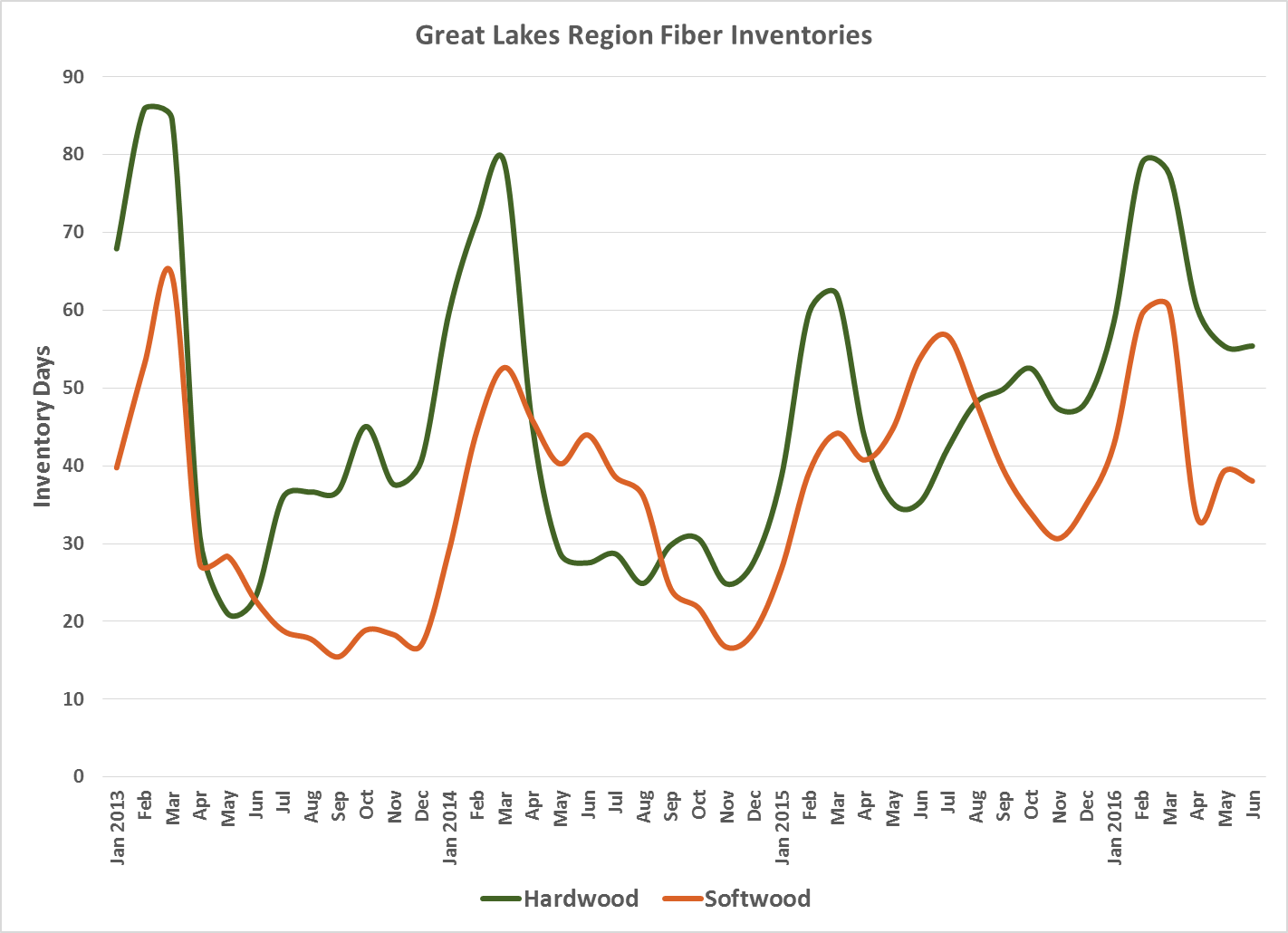

Forest2Market data indicates that in the Great Lakes region, achieving 80 days of system-wide inventory in the spring (March) is a key driver to reducing pricing volatility throughout the summer months, which typically require 30 days of inventory. When winter weather is ideal for harvesting, logging capacity is typically adequate to hit this target.

But a warm winter or an early, wet spring can drastically affect seasonal inventory building that can have lasting effects through the summer months. To ensure mill efficiency and profitability, inventories should include a percentage of “secured” wood from the sources noted above. That percentage will vary by mill and circumstance, but a good rule of thumb is to maintain 10 - 30 percent, which is similar to the percentage once supplied from company-owned timberlands prior to divestment. Maintaining this level of secured wood fiber will help mills manage the flow of wood between the minimum and maximum peak periods, as well as provide a level of stability to the wood suppliers and landowners within the region.

It’s important to note that this is a proactive approach—as opposed to a reactionary lurch—to dealing with a degree of uncertainty in the supply chain. While we do not control the weather and will always be at the mercy of it to some degree, the Great Lakes forest products industry can change strategies to better mitigate the impacts on wood flow, cost and price volatility.