2 min read

Mill inventory issues are nothing new in the Lake States. Forest2Market has been tracking fiber inventories and benchmarking prices in the Lake States for nearly three years. Over this time, the data shows that maintaining adequate system-wide inventories has been difficult across all species and products. As a result, price has increased significantly, making the Lake States the highest wood cost region in North America. The seasonality of wood supply in the region is the most significant factor mills take into consideration when planning for a consistent supply. While the specific inventory plan at each mill depends on a variety of other factors as well, the wood production system must not only generate a sufficient volume of supply, but the timing of the volume coming to market is also critical.

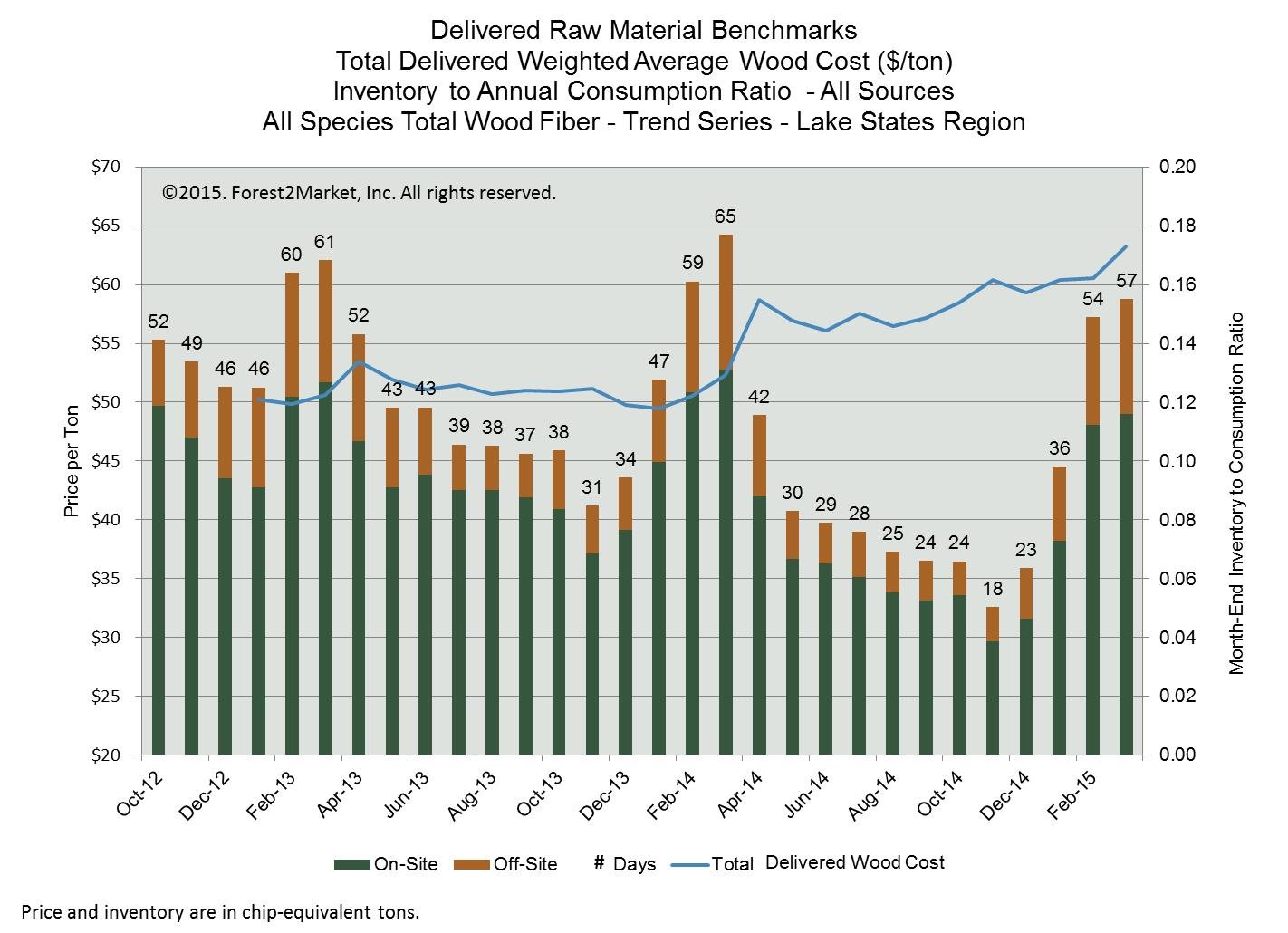

Declining Inventory Levels

The graph below shows all pulpwood species combined and demonstrates clearly that inventory levels have steadily declined since October, 2012. The graph also clearly demonstrates that adequate logging force surge capacity exists to build winter inventory for spring breakup. It is also apparent, however, that this surge capacity has limitations.

Three Causes of Inventory Declines

Drivers for this steady inventory decline include:

- Summer Harvesting Restrictions: While these vary by state and even county, summer harvesting restrictions create a bottleneck in the wood supply and inhibit the ability of the logging force to surge to needed levels during the summer. Again, the necessary level will vary by mill, but the winter surge capacity does not appear to be large enough to make up shortfalls in summer inventory. Examples of seasonal harvesting restrictions that contribute to this situation include Oak wilt, threatened and endangered species, invasive species and Annosum root rot.

- Land Ownership Changes: Changes in land ownership, which took place in the 2000s, have led to modifications in timber management regimes, and—to a degree—relationships between landowners and mills have changed as a result. Timber management is an art and a science, so no one method is correct for achieving sustainable forests. However, TIMOs, REITs and the next generation of small landowners have different management philosophies and objectives than previous generations, and this changes the nature of the wood supply chain. Prior to the changes in land ownership, integrated forest product companies owned their land base for the primary purpose of providing raw material to their mills. Following the sale of these lands to TIMOs and REITs, competing objectives focused on land value or real estate. This is not to say that the former integrated companies did not value the land or that wood production is unimportant today; the current landowners simply have different priorities for the land base they own. In addition, as ownership of non-industrial private forests transitions from parents to siblings, management objectives may change or just become unclear, and the result is often that small lots are less likely to be managed for timber harvesting.

- Development and Maintenance of Infrastructure: Since these changes in land ownership have taken place, the Lake States have seen a decline in the development of new—and maintenance of existing—infrastructure like wood roads; as a result of this lack of investment in the land base, bringing wood—especially hardwood—to market can be a challenge. This decline in infrastructure investment is a function of the change in land ownership, as different ownership objectives funnel investments in other directions.

Since none of these situations are likely to change in the near future, mills in the Lake States will need to become more adept at managing their supply to avoid inventory level issues. By taking steps to optimize their supply chains, mills can minimize the effects of seasonality and bring supply and demand closer to equilibrium.

Learn more about the Forest2Market Delivered Cost Benchmark.