2 min read

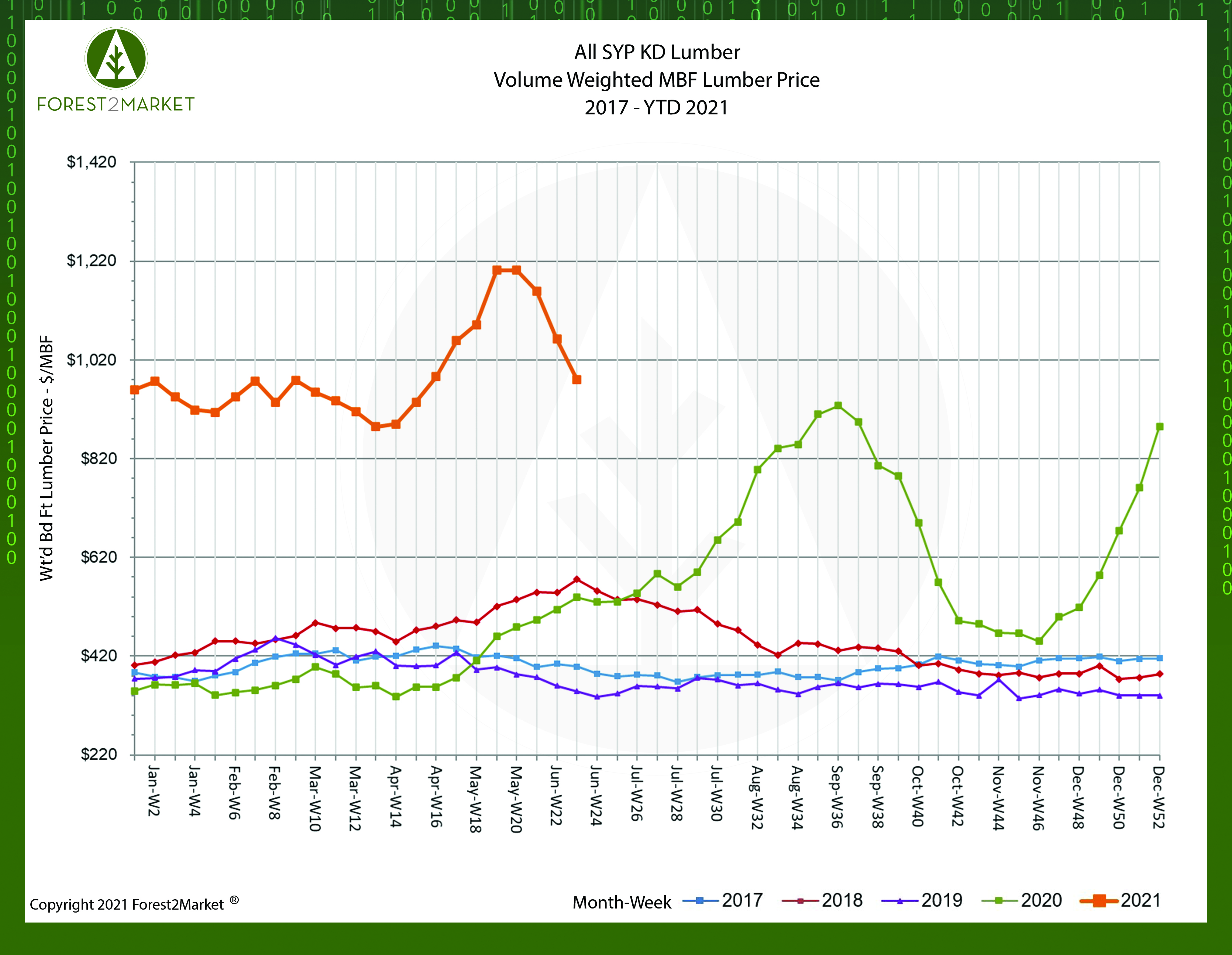

Last week, southern yellow pine (SYP) lumber prices continued to drop sharply—for the third week in a row—to the lowest level since mid-April. Forest2Market’s composite SYP lumber price for the week ending June 11 (week 23) was $979/MBF, a 7.8% decrease from the previous week’s price of $1,062/MBF.

Other price trends observed over the last several quarters in what has become the most chaotic lumber market in recent history include:

- 3Q2020 Average Price: $728/MBF

- 4Q2020 Average Price: $595/MBF

- 1Q2021 Average Price: $946/MBF

- 2QTD Average Price: $1,041/MBF

As some of the air is now being bled out of the inflated lumber market, the obvious question is: Going forward, where will prices settle… if at all?

Forest2Market’s composite SYP price chart above shows what can happen in a relatively short timeframe when unexpected forces cause an imbalance in supply and demand. After lumber prices peaked last September, they plummeted quickly and dropped by 47% over the course of the following six weeks. After temporarily bottoming in November, however, prices then skyrocketed 97% over the course of the next six weeks.

Will this roller coaster pattern continue into 2H2021?

Market View

No one knows where the “new normal” price of finished lumber will settle, but the futures market may provide some anecdotal guidance. Lumber futures for July delivery dropped more than 5% to $1,160/MBF early last week, which is down more than 30% from a record $1,711 in May.

“This pullback mostly reflects the unsustainable speculative peak that lumber futures experienced. While the series is volatile, the price surge that the futures saw was beyond anything we have seen before,” said Evercore ISI analyst Stephen Kim.

As we wrote earlier this year, the combination of strong (and surprising) lumber demand and pinched supplies from manufacturers resulted in a tremendous gap in the market, and the supply chain is just now beginning to rebalance. As the market continues towards equilibrium, two primary dynamics are now at work:

- Home builders have finally slowed pace; April housing starts declined by more than 9.5% and demand for lumber is waning as the construction sector simply backs off.

- Sawmills are incrementally increasing supply as the labor market slowly expands. New capacity in the form of both greenfield mills and existing mill expansions will help meet demand targets.

- In the near term, there are signs that inventories are catching up to demand patterns. During 1Q2021, US softwood lumber production ticked up slightly (+0.6%), US imports jumped 12.4%, and new orders inched down 0.3%.

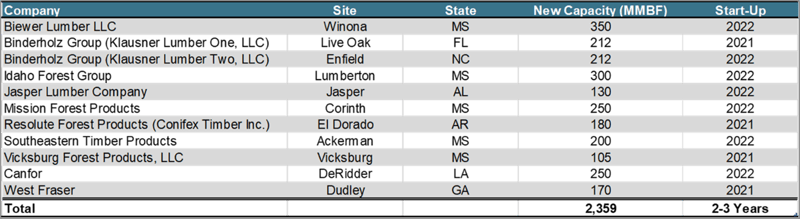

- In the longer term, additional capacity will help establish more surge flexibility in the supply chain going forward. In the US South, nearly 2.4 MMBF of new lumber capacity is scheduled to come online by the end of 2022.

Based on these developments, the market should see some relief over the next few quarters, albeit at prices that are still very much on the high side of the historical norm. Longer term demand patterns also portend a scenario where prices may continue to remain at more muted, yet elevated levels.

Weyerhaeuser CEO Devin Stockfish recently added: "I don't think $1,000 lumber prices are the new normal. With that being said, when you think about the amount of housing we're going to have to build in the U.S. over the next three, five, 10 years, that's just a significant amount of demand for wood products.”

This is a well-reasoned assessment based on what the market experienced in 2020. If we’ve learned anything at this point, it should be to expect the unexpected. However, barring another near catastrophic blow to the economy, the outlook for homebuilders remains strong as they seek to catch up with demand after a decade of persistent underbuilding.