5 min read

As we head into the throes of summer, we’ve enjoyed a much cooler and wetter weather cycle than this time last year, particularly here in the Inland region of the Pacific Northwest (PNW). But with the hot temperatures of wildfire season on the horizon, it’s a good time to reflect on industry developments in the region during the first half of 2016.

As we noted last year, fire season in this part of the world can really have an impact on timber availability and access, which will in turn affect regional mill operations, exports, prices and other sectors that support the forest products industry. For example, while many areas of the Inland region will continue to see wildfire salvage dimension logs as mill fodder well into 2017, Ponderosa Pine salvage has hit the end of its acceptable shelf life.

The forest products industry in the PNW continues to respond to some of these wildfire-related developments of 2015, as well as industry trends, economic challenges and continued regional consolidations. What have been the primary industry movers during the first part of the year, and what does 2H2016 look like at this juncture?

Consolidations

- Arguably the biggest story of 2016 thus far has been Weyerhaeuser’s acquisition of Plum Creek, which closed earlier this year and further consolidated the industry. This event will have wide-ranging effects that will continue to ripple throughout the timber industry for quite some time. Most notably for the PNW, this consolidation will directly affect the Inland region where Weyerhaeuser has not had a significant presence in either the timberland or the conversion sectors.

- This spring, coastal Western Red Cedar (WRC) log suppliers faced fewer market opportunities with the sudden announcement of Mary’s River Lumber closing its sawmills after many years of producing a wide array of WRC products. Constrained WRC log supply has being cited as the primary reason for these closures.

- Inland sawmill consolidation continues with the recent purchase and subsequent closure of the Blue North sawmill in Kamiah by Idaho Forest Group.

- The recently announced Nippon purchase of the Weyerhaeuser Longview liquid packaging operation came as little surprise to those familiar with the Japanese segment of the paper industry. We now see one of the smallest pulp and paper mills (Port Angeles) linked with one of the largest in the PNW region under Nippon ownership.

- Sierra Pacific continues building its new “super stud mill” in earnest at the former Simpson Mill 3 site in Shelton.

- The Olympic Panel Product transition to Swanson’s new veneer plywood plant in Springfield OR is complete, and Willis Enterprises announced the purchase of nearby Hoquiam Plywood to augment their local veneer plant.

- Willamette Valley’s integrated forest products company Rosboro is currently available for sale.

- At the time of this writing, the announcement by Weyerhaeuser that it will close two of the newly-acquired Plum Creek mills in Columbia Falls, MT—a sawmill and plywood plant—have added to the ongoing debate surrounding log availability, particularly public timber supply.

Uncertainty

- Currency: Global markets have continued to disappoint, and the relative strength of the dollar has also declined during 1H2016. As of this writing, the American dollar is worth $1.27 Canadian dollars, 6.57 Chinese yuan, .88 Euros, and 65.5 Rubles. While this decline in relative value of the USD would otherwise improve export leverage for US producers, the global economy seems to be barely chugging along. The recent jobs report was less than stellar, and Fed Chairwoman Janet Yellen has stated that the Federal Reserve will not be raising interest rates until some of the current uncertainty can be understood. Ms. Yellen also said that a number of “considerable and unavoidable” uncertainties could affect the economic outlook, as well as the future of interest rates, including sluggish global growth, weak business investment, low US productivity growth and uncertainty for inflation. “The uncertainties are sizable, and progress toward our goals and, by implication, the appropriate stance of monetary policy will depend on how these uncertainties evolve,” she added.

- Global Politics: With the recent “Brexit” development in the United Kingdom, Great Britain has effectively voted to leave the European Union, which has sent shockwaves of further political and market uncertainty throughout the globe; the Dow Jones Industrial Average was down over 600 points the day after the vote. While it’s simply too early to tell how this will affect markets and geopolitical relations around the world, it will be an ongoing story with multiple layers and potential outcomes in the coming months and years. For now, the uncertainty about the future of both the UK and the EU is adding to an already tense climate of uncertainty.

- National Politics:

- Suffice it to say, the US political climate has just begun to simmer in the run up to the November, 2016 presidential election. Financial markets typically react with some degree of trepidation during election season, and this cycle promises to be no different. Domestic and export markets will likely remain in a holding pattern through November; what happens thereafter is anyone’s guess.

- The recent “bombshell” announcement by current WA DNR Commisioner Dr. Peter Goldmark that he will not seek a third term in the upcoming fall 2016 election has left many in the forestry community scrambling to endorse a qualified contender amongst an otherwise green candidate pool. Thank you, Commissioner Goldmark, for your eight years of service.

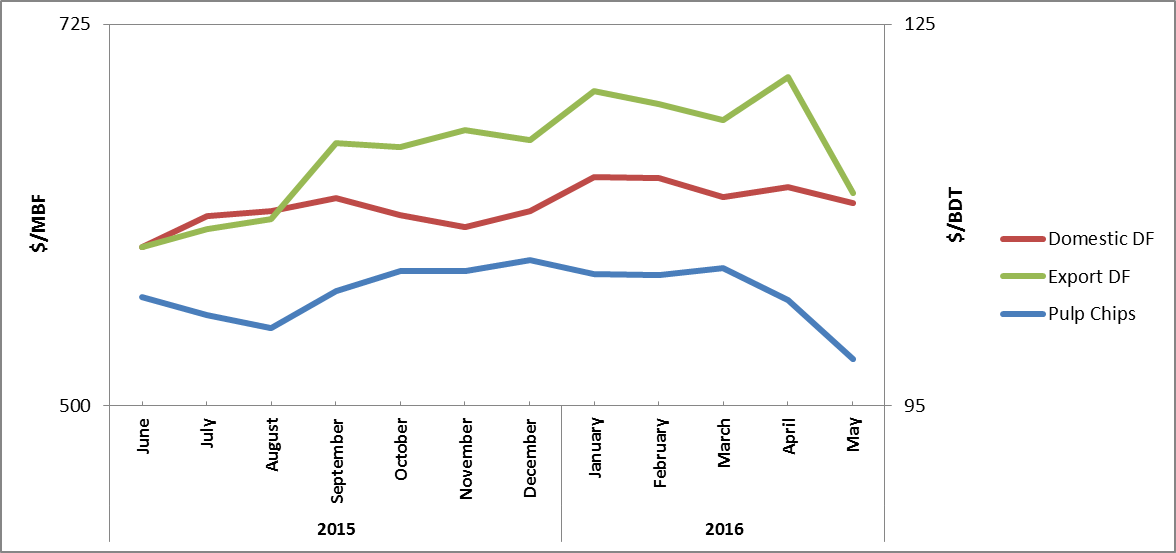

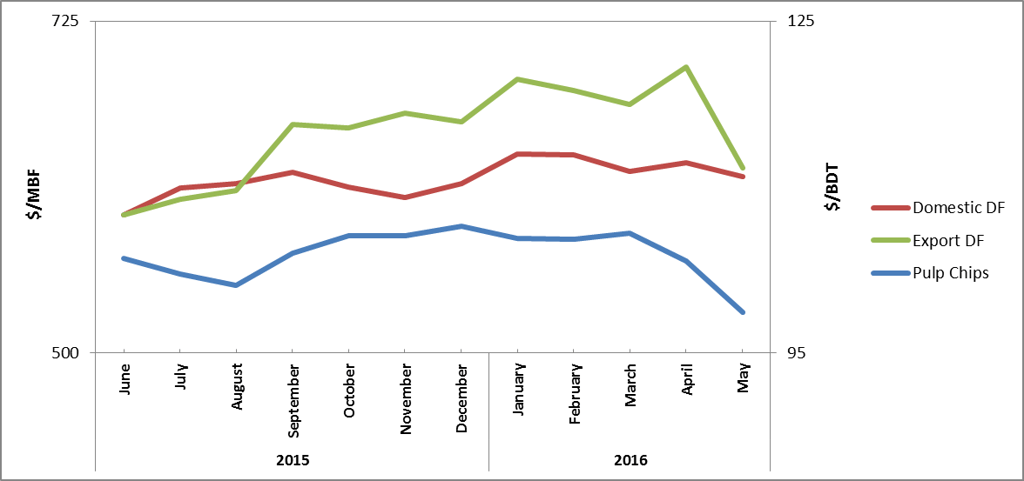

PNW Fiber and Log Costs Still Unstable

Anyone that has spent long enough in the timber industry knows the truism, “the only thing you can count on is change.” And while many throughout the region feel that fiber costs have stabilized in recent months, the chart below tells a different story for export and domestic Douglas Fir log prices, as well as pulp chips.

To that end, there are a few developments on the horizon that may continue to affect what appear to be stabilized market prices:

- Softwood Lumber Agreement: With the expiration of the Softwood Lumber Agreement (SLA), a significant increase in Canadian lumber imports into the US (and its lackluster housing market) have had a double-edged effect on stabilizing lumber and fiber availability within the PNW. Recent negotiation updates aiming for a swift resolution look dismal; Canada continues to struggle with consensus amongst its east and west provinces, while the US holds a hard line on import policies.

- Log pricing in wildfire zones: 2015 fire salvage efforts are well underway, but what will the 2016 fire season bring? At the time of this writing, the PNW looks cool and wet but not for long, as the summer heat is just around the corner. As fire salvage continues, residual chip quality will suffer with some regional suppliers scrambling to find alternative markets for charred chips.

- Scheduled upcoming PNW pulpmill downtimes may cause significant supply chain backlogs creating both challenges and opportunities within an already tense supply chain.

- Availability of Red Alder and Cedar logs at conversion facilities: These two “secondary” specie groups are more riparian in timber management regimes and their availability to markets is subsequently tied directly to Douglas Fir and Hemlock harvest levels. Procurement managers for these mills must be more creative in offering market solutions to landowners to help ensure focus on these valuable species as part of their overall harvest and silvicultural operations.

- Cross Laminated Timber (CLT): The prospect of the developing markets for a sought-after building technology for multi-family and commercial projects could certainly be a significant development for sectors of the PNW lumber industry. With the Portland and Seattle metro areas being the lead architectural markets for CLT, our industry is well positioned to help ensure success.

As noted above, the impact of the current political uncertainty on global trade and markets—including the forest products industry—cannot be overstated as we approach the second half of 2016. "China continues to face considerable challenges as it rebalances its economy toward domestic demand and consumption and away from export-led growth," added Ms. Yellen. “Considerable uncertainty about the economic outlook remains,” she stressed. “The latest readings on the labor market and the weak pace of investment illustrate one downside risk — that domestic demand might falter.”