5 min read

Despite the uncertainty surrounding the Brexit vote and what it will mean for UK (and European Union) biomass use in the future, the Lynemouth power generation station has received Contracts for Difference (CfD), MGT Teeside has obtained financing, and 20 percent of the UK’s renewable energy is produced by Drax. As these (and other) projects come to fruition, the global wood pellet industry appears to be in a relatively stable place—all things considered. In fact, new demand for industrial wood pellets is on the horizon as directives from the Paris climate agreement begin to take effect.

Asian markets—particularly the Japanese and South Korean markets—represent new opportunities for wood pellet producers, including those located in the US South. The Japanese government (mindful of the extensive damage caused by the Fukushima Daiichi nuclear disaster in March 2011) has approved nearly 3.2 GW of biomass-fired capacity, and approximately 500+ MW are already commissioned. South Korea has been consuming roughly 1.5 to 2 million tons per year for the last several years under its renewable portfolio standard (RPS), which has thus far resulted in co-firing pellets alongside coal to meet its binding renewable obligations.

Policy Developments

Japan

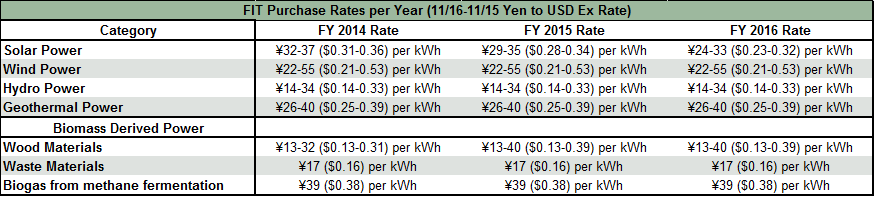

According to Organisation for Economic Co-operation and Development (OECD)[1], Japan has the second largest electricity market and the third largest economy in the world. Prior to the Fukushima Daiichi event, Japan’s power was primarily generated from fossil fuels and nuclear reactors. Soon after the disaster, Japan increased its use of, and dependence on, fossil fuel imports for thermal generation, leading to an increase in electricity prices and in Japan’s greenhouse gas emissions. The Japanese government has since established a renewable electricity goal, pledging that between 25 - 35 percent of its electricity will be generated from renewable sources by 2030. In order to reduce fossil-fuel reliance, Japan also introduced a feed-in tariff (FIT) system in 2012 to promote the introduction of renewable energy.

The FIT system forces power companies to buy electricity generated from renewable energy sources at set rates provided by the Minister of Economy, Trade and Industry (METI) for a period of 10 to 20 years. Operators of electric utilities can recover costs incurred by the purchase of renewable electricity by invoicing consumers a surcharge in addition to the amount usually charged for the supply of electricity. The following table highlights the METI FIT annual rates and specified periods.

Since the introduction of the FIT system, the number of power generating facilities using renewable energy has steadily increased. Approximately 28 coal power stations are currently operating and 4 power stations are under construction. Only a handful of those power stations co-fire biomass in the form of wood material (i.e. wood pellets, palm kernel shells, waste wood, etc.). In addition, several new power units with the capability to co-fire biomass have either been announced, are currently permitted for future construction, or are in pre-permit development . Unfortunately, however, complexities with the FIT system are causing project developers with long lead times (including biomass power plants) some degree of uncertainty regarding the annual FIT revenue they will receive. This uncertainty is making it difficult for biomass power developers to secure financing and, not surprisingly, no large projects have yet commenced.

South Korea

In January 2012, the Renewable Portfolio Standard (RPS) replaced the previous feed-in tariff system in order to accelerate South Korea’s goal to create a competitive market environment for renewable energy. The RPS program requires 13 of the largest power companies (those with installed power capacity larger than 500 MW) to steadily increase their renewable energy mix in total power generation from 2012 - 2024.

RPS targets are reviewed and adjusted every three years and can be met by electricity generated from wind, solar, biomass, biogas, waste-to-energy, landfill gas, tidal, hydro and integrated gasification combined cycle. Power producers in the RPS system receive Renewable Energy Certificates based on the technology used and, in order to meet their RPS targets, can either invest in renewable energy installations or purchase RECs on the market. Power companies are obligated to submit gathered RECs to the New and Renewable Energy Center (KNERC) on an annual basis.

The government of South Korea has expressed concerns about power generators’ heavy reliance on co-firing to fulfill their RPS obligation. Therefore, it has proposed a 30 percent limit on the proportion of the RPS quota that each utility could achieve through co-firing in order to encourage investment in a wider portfolio of renewable technologies.

Supply

Japan

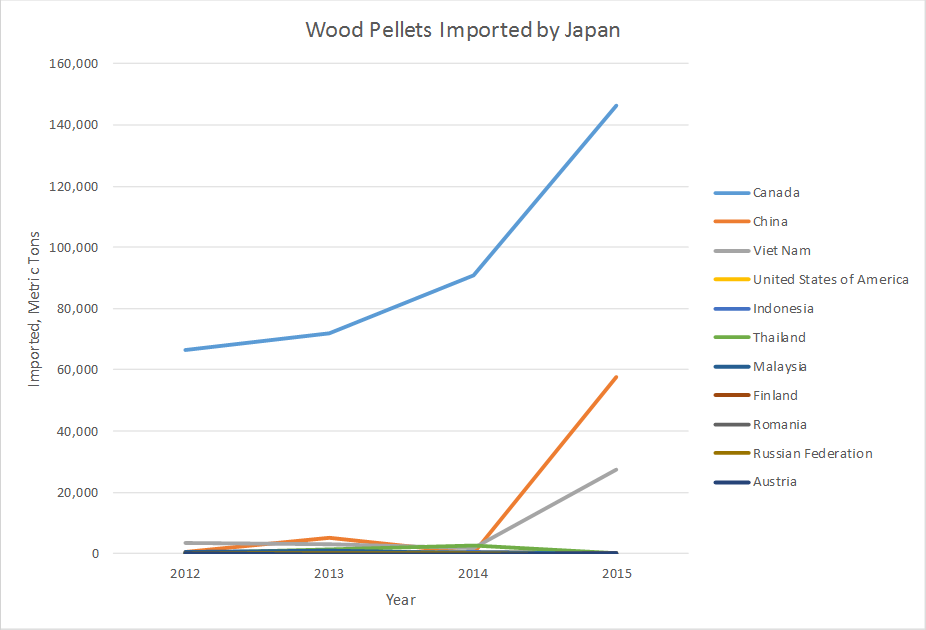

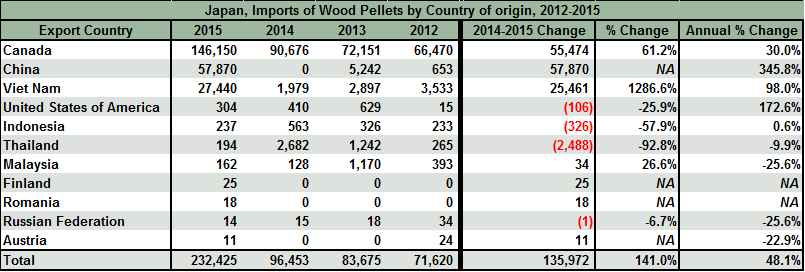

Japan’s production and import of wood pellets has increased since the FIT system was expanded to include biomass and other renewables in 2012. In 2014, Japan was home to 142 operating pellet facilities that produced 126,000 metric tons; most facilities produce between 100 and 1,000 metric tons annually, which is a very small quantity compared to export wood pellet facilities in the North America and Europe.

Canada has remained Japan’s biggest source of wood pellets, supplying approximately 63 percent (or 146,000 metric tons) of Japan’s imports in 2015. Other Asian suppliers such as Malaysia, Indonesia and Vietnam can all compete on a cost-per-metric ton basis; however, Japanese buyers maintain strict criteria for pellet sustainability and quality. Japan, concerned with reliability of supply, is willing to sign long-term contracts with producers able to guarantee supply quality and stability.

South Korea

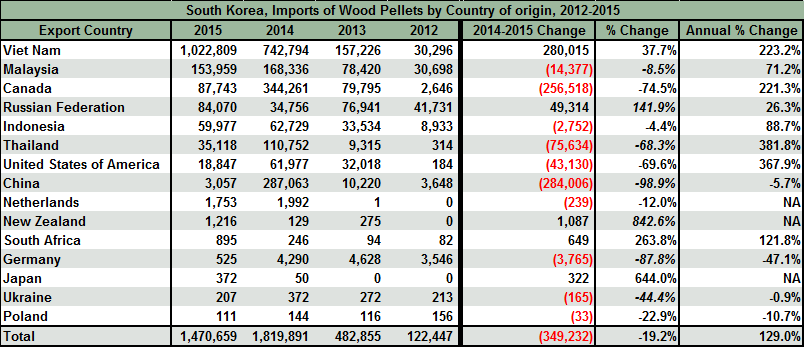

Vietnam has been South Korea’s primary source for imported wood pellets over the last three years, with amounts steadily increasing on an annual basis since 2012. In 2015, Vietnam supplied 70 percent of South Korea’s wood pellets at the lowest USD$ per-metric-ton cost. However, the market is young and South Korean power generation companies are still on a bit of a learning curve, as much of the Vietnamese product is of questionable quality. This has led South Korean electricity generators to establish new tender invitations that distinguish between “wood pellets” and “woody biomass from short-rotation forests (SRF).” This change gives the generators the opportunity to source lower cost, non-woody biomass if they so wish, while allowing them to account for the varying quality of the two categories when evaluating the price of the tender. This two-category arrangement should create a more level playing field between suppliers of wood pellets, who won’t be forced to compete with suppliers of lower-priced woody biomass from SRF.

South Korea has also reportedly entered into agreements with other low-cost producers in Indonesia, which provides further regional access to wood pellets.

Competition

Japan

An abundance of domestic biomass exists in Japan, though most of it cannot be sourced economically. As Japan adds more biomass to its energy portfolio to meet its 2030 goal, it will need to rely on imports . Currently, the major consumers of wood biomass are power generation companies; demand is primarily concentrated to two co-firing stations, Tokyo Electric Power 1GW Hitachinaka power station and Kansai Electric Power 1.8 GW Maizuru plant. But there are others that are either operational, or entering, the market:

- Shikoku Electric Power’s Saijo Power Station co-fires biomass with coal.

- Nippon Paper Fuji Power Station plans on co-firing biomass and coal for its 100 MW facility.

- Sumitomo owns and operates two biomass power plants: Itoigawa Biomass Power Plant (50MW) and Handa Biomass Power Plant (75MW).

- Showa Shell Sekiyu K.K. has a 49MW biomass power plant that uses wood pellets from Canada and palm kernel shells from Southeast Asia.

Palm kernel shells (PKS) are the major competition to wood pellets in terms of imported biomass used for power generation in Japan. PKS is a fibrous material and can be easy handled in bulk directly from the product line to the end use. In 2015, Japan imported 456,000 metric tons of PKS from Indonesia and Malaysia, which was nearly twice as much raw material volume than its imported wood pellets (232,000 metric tons). Future demand from wood pellets and other biomass is expected to grow, as at least 10 facilities, in various stages of development are expected to come on line over the next seven years.

South Korea

South Korea has access to wood residues from its domestic sawmilling industry that could be used for the manufacturing of pellets. However, this domestic supply will not be sufficient, and South Korea will need to increase pellet imports to meet its 6 percent goal in 2020. The government estimates that by 2020, 75 - 80 percent of pellets consumed in the country will need to be imported.

The companies obligated to participate in the South Korean RPS include six wholly-owned subsidiaries of its state-owned Korea Electric Power Corporation and seven independent power producers. Currently, a handful of power companies co-fire coal and biomass. Korea South-East Power plans on converting its Yeondong Thermal Power Plant Unit 1 to biomass in the future; it will have the capability of burning 100 percent coal or 100 percent biomass (95 percent wood pellets and 5 percent wood chips or PKS).

All reports show that Japan and South Korea are the most likely emerging markets for increased global wood pellet and fuel chip demand. While Europe is the largest consumer of wood pellets to date, both Japan and South Korea continue to increase their consumption. While these new pellet markets are in their infancy and will take time to develop, policies, supply and demand all point strongly to the establishment of substantial and stable markets for wood pellets over the next 10 years.

For an expanded version of this post:

[1] https://data.oecd.org/energy/electricity-generation.htm, November 1, 2016.