Pete Coutu

Pete Coutu

We often evaluate performance by determining whether a particular process, product or service is in the top quartile or top 10 percent of its peer group. Benchmarking, in this respect, is an effective way of evaluating current performance. But how do we take top-tier performance to the next level and achieve truly superior performance? By focusing on the details, on the pennies, and on incremental gains. In the raw material supply chain, how does a company gain an additional 1% in efficiency to reduce cost? With the application of reliable, granular data.

On an annual basis, the average North American sawmill consumes roughly 600,000 tons of sawtimber (larger, modern sawmills consume nearly twice as much), and the average pulp mill consumes in excess of 1.5 million tons. When purchasing wood raw material on this scale, pennies matter.

Forest2Market’s deep databases of actual transaction data equip our customers with the most accurate and precise raw material pricing data available – down to the penny. Using our benchmarks and reports, our customers are able to pinpoint individual cost component inefficiencies in their supply chains including origin, destination, volume, price, species, product and a host of other unique attributes of individual loads of wood. They can then use this market intelligence to implement new strategies, eliminate inefficiencies and track improvements over time.

Identifying savings opportunities and lowering your unit cost ($/ton) by pennies can have a tremendous impact on your bottom line: a 1% reduction in cost will pay for the cost of your Forest2Market subscription fee many times over.

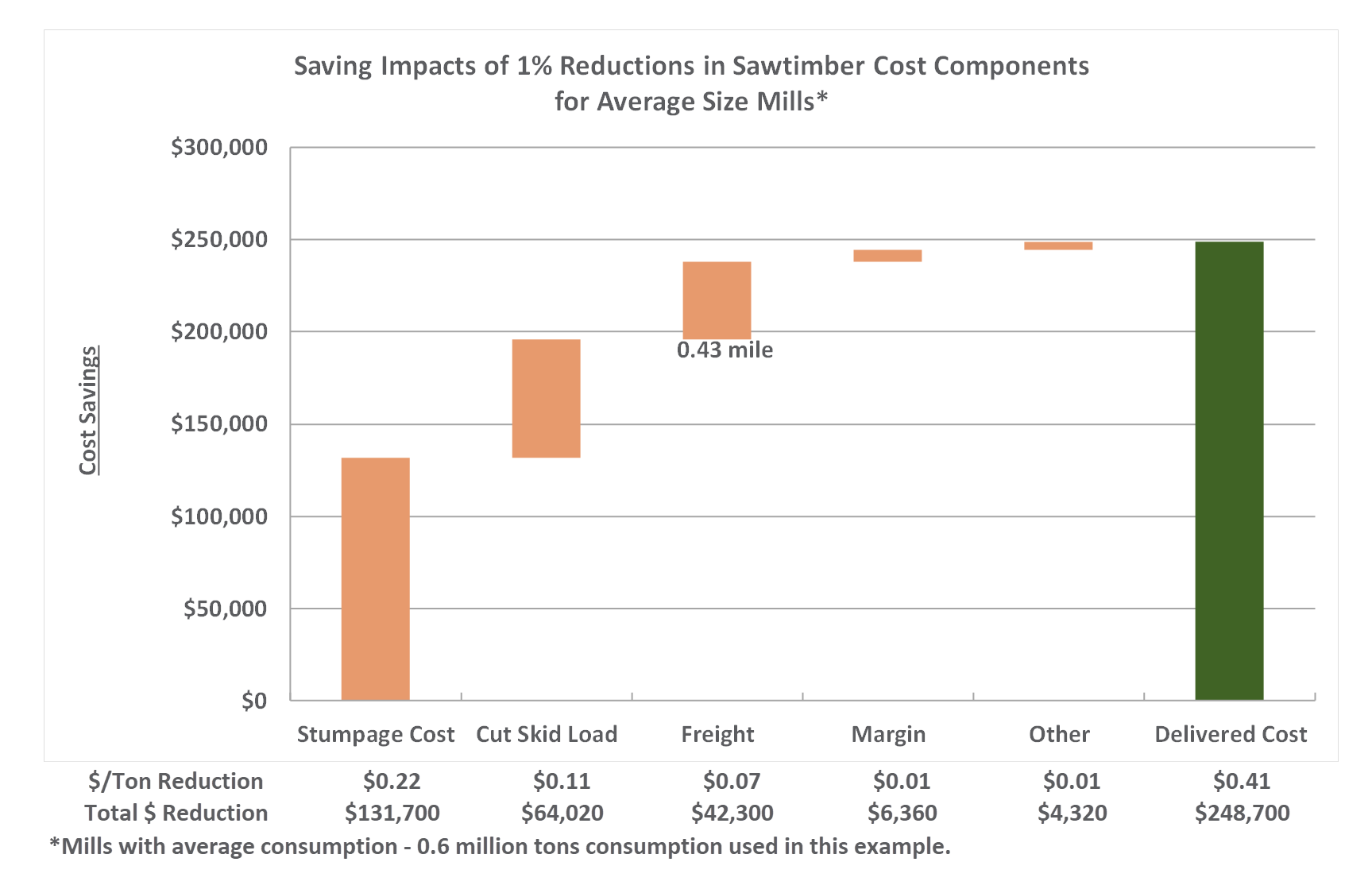

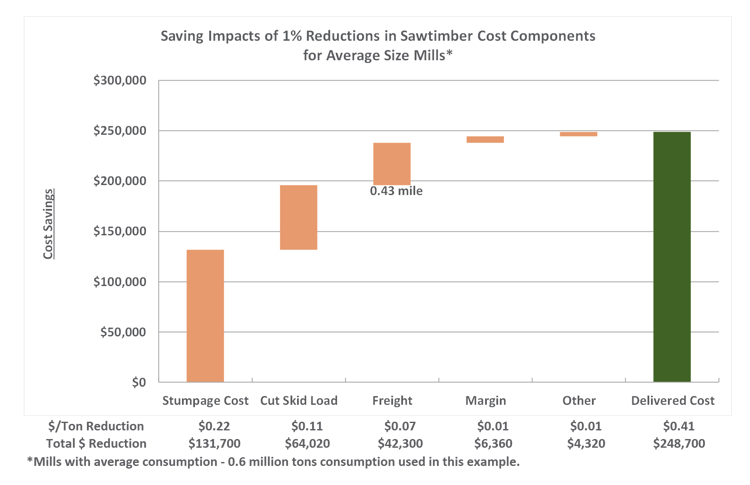

Sawmill Savings

When breaking down the total delivered cost for an average-sized sawmill, stumpage is clearly the largest cost component (roughly half). However, a 1% reduction in the average freight cost ($0.07/ton) for the average-sized sawmill results in $42,300 of savings.

Applying this same methodology to the other cost components yields similar savings that, when combined, establish substantial cost-cutting measures totaling nearly $250,000. For the average-sized sawmill, this kind of savings creates real value with a lasting impact as noted in the chart below.

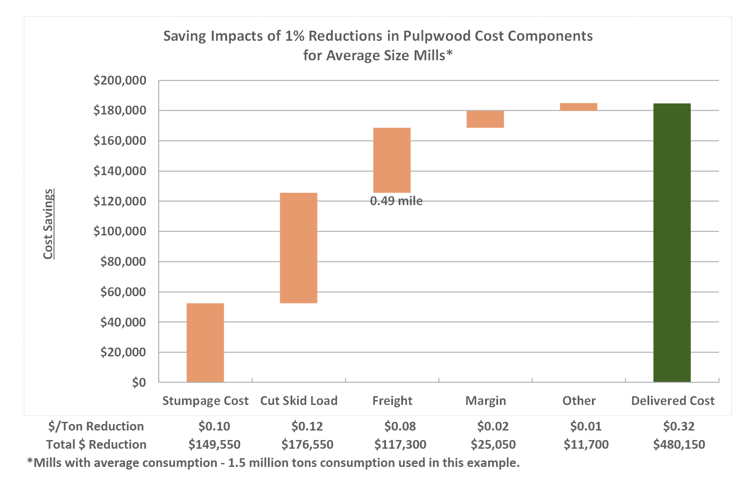

Pulp, OSB, Pellet Mill Savings

When breaking down the total delivered cost for a large pulp mill, OSB or pellet facility, the cut-skid-load cost component is nearly the same as the stumpage component; together, these two components make up roughly 70% of the total delivered price for the facility’s wood raw materials.

A 1% savings on the average freight cost ($0.08/ton) equates to $120,750 in annual savings. As a freight rate ($/ton/mile) this suggests that a half-mile reduction in the average haul distance can contribute to total savings in this case of over $480,000.

As illustrated above, pennies do matter. But how can a company armed with a deep knowledge of its supply chain truly affect its bottom line by optimizing its cost components? There is no easy, “one-size-fits-all” answer to this question because every organization is different. However, a continuous process of improvement that involves collecting the right datasets, analyzing this data and acting on this data is the sure path to superior performance.