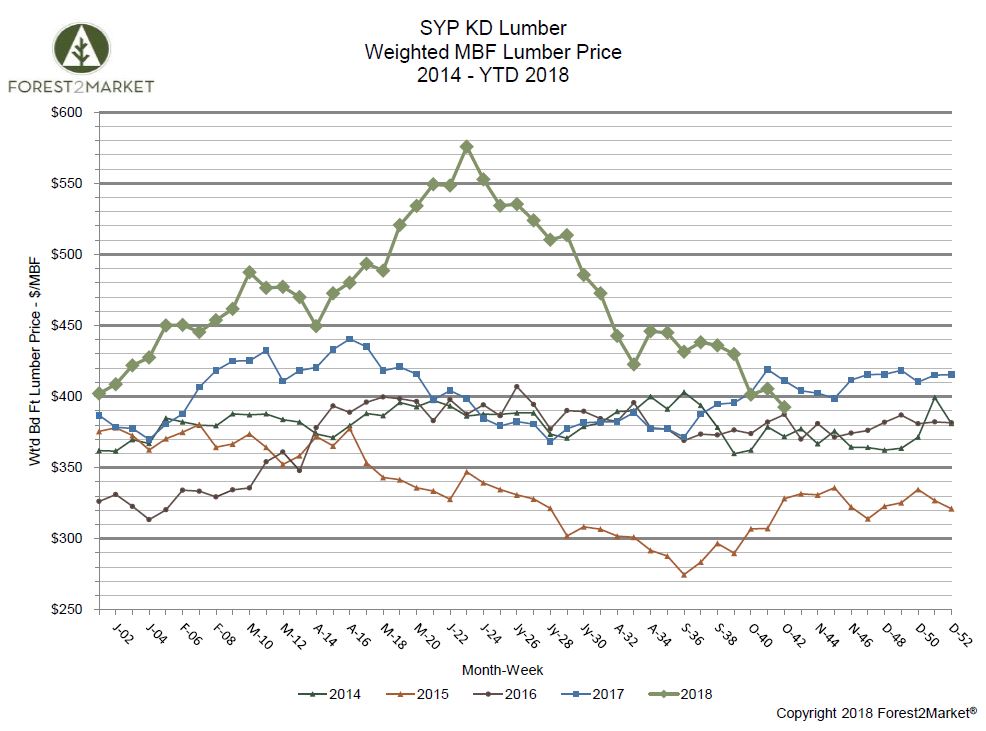

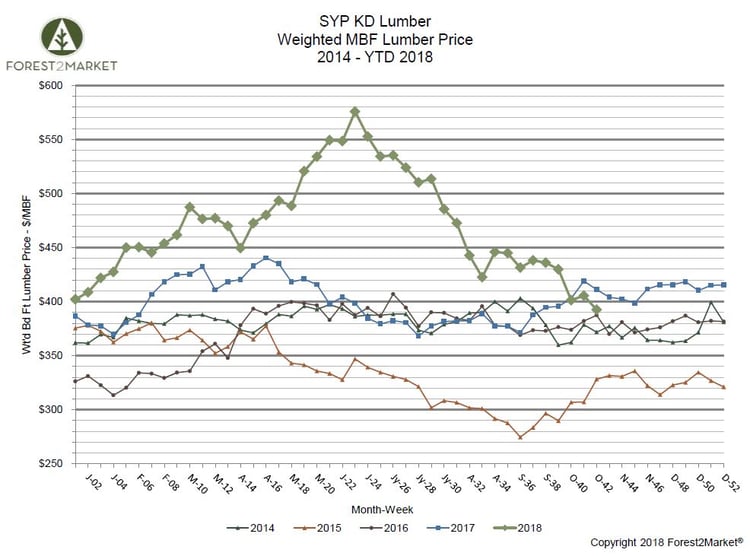

Southern yellow pine (SYP) lumber prices leveled out in September before plummeting to a new 2018 low in mid-October. Forest2Market’s composite southern yellow pine lumber price for week 42 was $392/MBF, a 3.2% decrease from the previous week’s price of $405/MBF and a 4.6% decrease from the same week in 2017. This is also the third week in a row that prices in 2018 have been below prices in 2017.

Price volatility decreased in September as prices were range-bound between $430/MBF and $438/MBF. After reaching a record high price of $576/MBF in late June, SYP prices declined rapidly before bottoming at their lowest point of the year in week 42.

A closer look at some of the prices we have seen since the beginning of the year:

- 1Q2018 Average Price: $449/MBF

- 2Q2018 Average Price: $523/MBF

- 3Q2018 Average Price: $486/MBF

- YTD Average Price: $471/MBF

Erratic Prices all Around

The North American lumber market seems plagued by a high degree of uncertainty combined with lackluster US housing starts. In the South specifically, new orders ticked up but shipments were down in week 42, as the regional market and supply chain adjust in the aftermath of two major hurricanes. The cleanup effort will take some time before rebuilding can begin across much of the devastated South, which should drive an increase in demand in the near term.

The producer price index (PPI) declined 0.1 percent in September (+2.8 percent YoY). In the forest products sector, Lumber & Wood Products were down 1.9 percent (+6.5% YoY), and Softwood Lumber was down 9.6 percent (+5.0 percent YoY), demonstrating that the market has cooled significantly since the highs from just four months ago.

Other construction materials have followed a similar price pattern as lumber—which is to say erratic—in 2018. Per a recent report from the National Association of Home Builders (NAHB), residential construction goods input prices increased 0.2 percent in September after declining each of the prior two months; the index has risen 5.2 percent in 2018 and is 10.2 percent higher than it was in January 2017.

- From January to September of 2017, the index for gypsum products rose 7.2 percent and it has increased 8.1 percent over the same period in 2018. Gypsum prices also reversed trend in September, however, falling 0.1 percent after a combined increase of 6.1 percent over the prior two months.

- The index for oriented strand board (OSB) decreased 5.2 percent in September, the second consecutive month of decreased prices. Prices are down 16.4 percent since July and have declined in five of the past 12 months.

- The index for ready-mix concrete (RMC) prices increased 0.4 percent in September, reversing four months of declining prices. Prices for RMC skyrocketed surprisingly in March but have fallen back in line with long-run trends.

"Builders are motivated by solid housing demand, fueled by a growing economy and a generational low for unemployment," said NAHB Chairman Randy Noel. "Builders are also relieved that lumber prices have declined for three straight months from elevated levels earlier this summer, but they need to manage supply-side costs to keep home prices affordable."

In the near term, builders should benefit from the lean supply of homes for sale. However, newly built homes come at a premium price—especially with the high cost of residential construction goods we have seen in 2018. Higher prices for land, labor and materials have impacted builder profitability in the less-expensive home segment, which is why many continue to focus on the move-up market.