Joe Clark

Joe Clark

US forest industry performance in November and December was recently reported by both the US government and the Institute for Supply Management.

Total industrial production (IP) rose 0.6 percent in November (+3.9 percent YoY) after a downward revision (from +0.1 percent to -0.2 percent) to October’s reading. Manufacturing production was unchanged (excluding autos: -0.1 percent), mining output increased 1.7 percent, and the index for utilities gained 3.3 percent.

The full report on November’s new orders was not published because of the partial government shutdown. However, a preliminary estimate of business investment spending (-0.6 percent MoM; +6.6 percent YoY) was provided in the Census Bureau’s advance report on durable goods orders. “The third decline in four months for business-equipment orders may add to concern… that corporate investment and factory activity are at risk of slipping into a more pronounced slowdown,” wrote Bloomberg’s Sho Chandra.

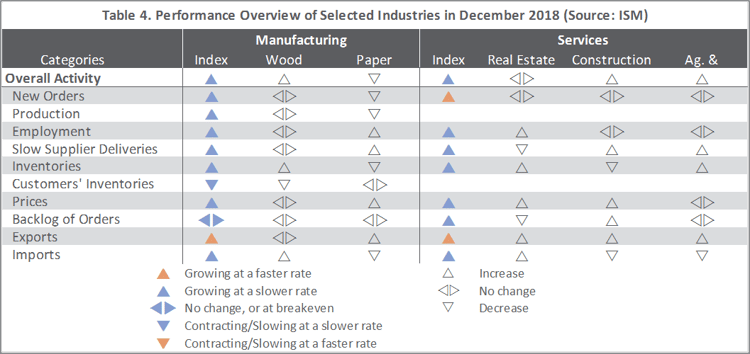

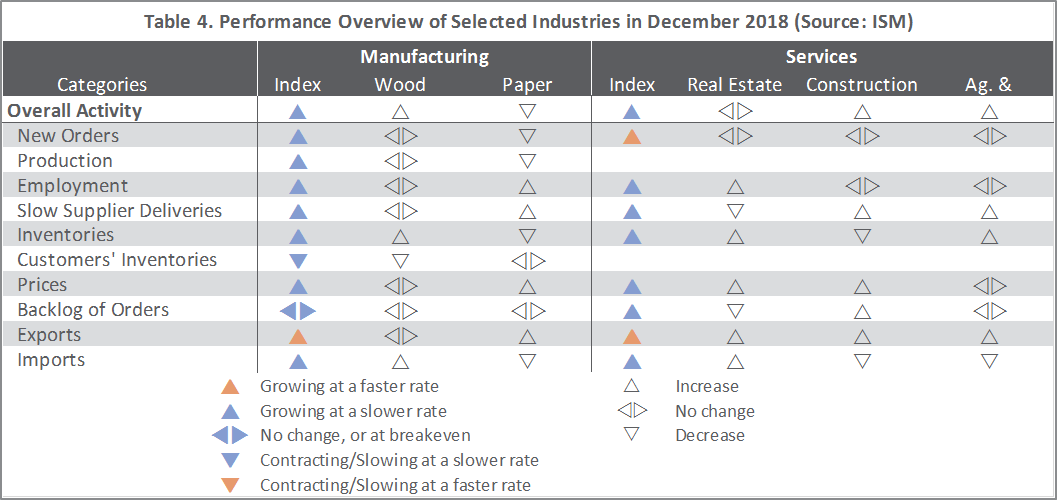

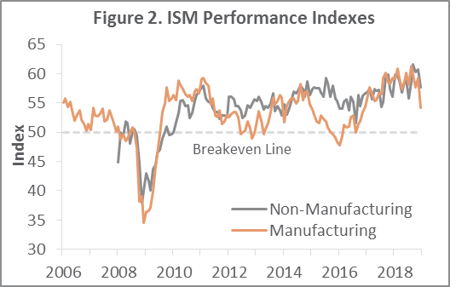

The Institute for Supply Management’s (ISM) monthly sentiment survey showed that in December the expansion in US manufacturing decelerated (-5.2PP, the steepest drop in over a decade) to 54.1 percent (Figure 2). The pace of growth in the non-manufacturing sector also lost some momentum (-3.1PP, to 57.6 percent). There was little indication in the data of trade issues weighing on business; export orders accelerated while imports eased only slightly (Table 4).

Of the industries we track, Paper Products contracted and Real Estate was unchanged; the rest expanded. “New residential home sales have slowed significantly,” one Construction respondent wrote. “Tariff delay has slowed material cost increases, but all indications are that January will bring price increases.” A Real Estate respondent was more upbeat: “Business is exceeding expectations; 2019 should [equal] or exceed 2018.”

The consumer price index (CPI) was unchanged (+2.2 percent YoY) in November, as a 4.2 percent decline in the gasoline index offset increases in an array of indexes including shelter (+0.3 percent) and used cars and trucks (+2.4 percent). The all items less food and energy index increased 0.2 percent (+2.2 percent YoY).

The producer price index (PPI) edged up 0.1 percent (+2.5 percent YoY). A 0.3 percent increase in prices for final demand services (led by fuels and lubricants retailing: +25.9 percent) offset a 0.4 percent decrease in the index for final demand goods (especially gasoline: -14.0 percent).

Forest products sector performance (Indices) included:

- Pulp, Paper & Allied Products: + 0.1 percent (+2.9 percent YoY)

- Lumber & Wood Products: -1.0 percent (+1.4 percent YoY)

- Softwood Lumber: -3.0 percent (-10.5 percent YoY)

- Wood Fiber: +0.1 percent (+3.8 percent YoY)