3 min read

The modern forest supply chain is without guidance for operating in the current pandemic-driven economic environment, but we do have the next best thing: Historical data and context.

Though the drivers were completely different, the Great Recession that began in 2007 is the closest example we have for reference based on the economic downturn we find ourselves navigating today. At this point, we can hope that the effects do not last nearly as long as those associated with 2007, but it’s still too early to tell how things will play out.

One thing is certain, however: Southern timber markets will react.

What Drives Timber Prices in the South?

The two primary factors that drive timber prices at both the mill gate and on the stump are the general economic principles of supply and demand.

- Log supply (standing timber): While many mills were forced to adapt and improve efficiencies in the immediate aftermath of the Great Recession, many landowners simply pulled their timber off the market in hopes of driving prices higher in the future. This combination has caused the total volume of logs on the stump throughout the US South to rise unimpeded for the last decade. This oversupply combined with improved mill efficiencies has kept log prices on the historically low side, even as demand for lumber and sawmill production has increased amid an improving housing market.

- Mill demand: Over the last decade, sawlog demand from mills has not tracked with the rising demand for lumber. During the years immediately following the great recession, the surviving mills became much more efficient at sawing timber, which ultimately allowed them to use less wood in the lumber-producing process. These mills adapted to the market and learned to do more with less, which has kept log demand muted despite an improving housing market.

What can supply/demand relationships and historical transaction data from the Great Recession tell us about how southern timber prices react in a severe downturn, and what we might expect over the course of the next several quarters?

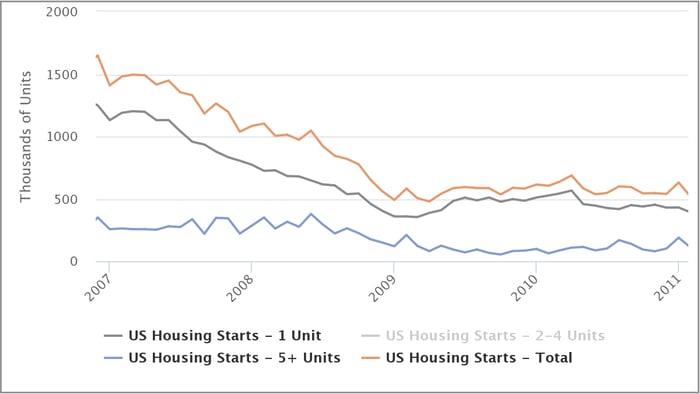

Stumpage prices plummeted in tandem with housing starts as the Great Recession gripped the entire global economy. Starts began dropping precipitously in 2007 and bottomed at just 500,000 units in 2009, as demand for finished lumber and panels dried up.

Housing Starts from 2007 to 2011

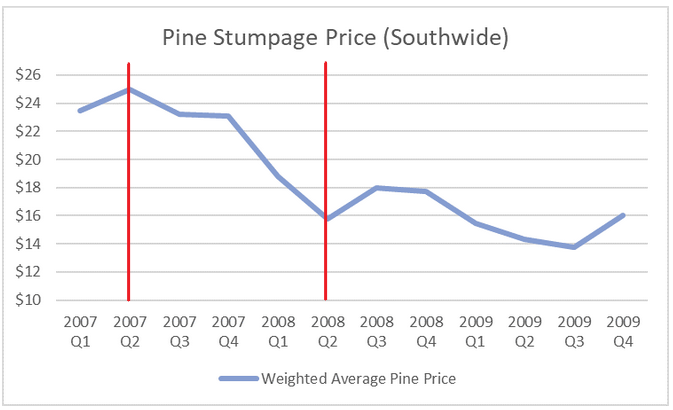

Timber prices reacted quickly to market signals early on in the recession; notice the quarter-over-quarter decreases in price as the situation grew more dire. Weighted average pine stumpage prices demonstrated a 25% drop from 2Q2007 to 1Q2008, plummeting from $24.99/ton to $18.63/ton.

Historical vs. Current Market: Similarities

From the onset of the Great Recession in 2007 and its immediate aftermath, the market for southern timber shrank due to lack of demand. The tremendous reduction in demand for lumber and other building products sent shockwaves through the entire forest supply chain, resulting in the current oversupply of timber on the stump throughout southern forests.

WATCH: Mike Powell discusses COVID-19 impacts on southern timberland owners

As I wrote late last year, timberland owners continue to face another challenging situation based on the abnormal weather events of the previous 18 months. Prolonged periods of wet weather made timber tracts that were previously purchased simply unworkable by the end of 2018; the markets reacted accordingly and sent stumpage prices soaring in 1Q2019. Harvesting crews put these tracts on the back burner and moved to workable tracts to maintain production. However, when the wet weather subsided, these crews simply circled back to work the previously-purchased tracts that had dried out.

Fast forward to the current market: As a result of those surpluses of wood on their books, many procurement teams aren’t actively buying nearly as much timber and are still working to get rid of what they already have. Now, add in a global recession and record levels of near-term uncertainty and it’s enough to make southern timber markets grind to a halt.

Outlook

Stumpage prices across the South are once again suppressed as demand is poised to remain low for the next several months.

- Sawtimber: Relationships with big box stores and general home improvement has provided a glimmer of light, however overall production cuts on a regional scale have resulted in soft market conditions. With producers facing a prolonged period of uncertainty as the lumber market treads water, sawlog prices have dropped as procurement teams are seeking to maximize liquidity, only buying what is needed. Likewise, independent brokers are following a similar strategy as they’re unsure if they can find outlets for purchased wood. The effects have been localized, however, as not all areas have seen drastic production cuts.

- Pulpwood: As the nation has scrambled to buy a year’s worth of toilet paper, market demand has not been an issue for pulp markets. In fact, pulpwood harvests from southern timberlands have increased as manufacturers try to keep production levels high and consuming pulp/paper mills look to offset the decrease in residual chips typically generated from full production sawmills. While demand has been strong, there has also been ample supply, which has kept stumpage prices in check.

- Timberland Owners: Landowners are now dealing with three challenging dynamics: 1) repercussions of the oversupply of both sawlogs and pulpwood that date back to the Great Recession; 2) slack demand in the current market, which is keeping downward pressure on prices, and; 3) near record levels of market uncertainty and a high-stakes election on the horizon.

Many timberland owners simply pulled their tracts off the market during the Great Recession in hopes of riding out the worst of the downturn. We know this move directly contributed to the oversupply that has kept prices low over the last decade. With margins poised to get thinner and demand already shrinking, will owners repeat history or cut their losses and keep supplies flowing this time around?