4 min read

A recent article by Kai Merivuori, Managing Director of the Finnish Sawmills Association (Sahateollisuus Oy), outlines a number of serious issues that independent sawmills are currently facing in Finland—existential issues that have caused some mills to stop buying logs. Given the strong global demand for sawn softwood, this situation has resulted in Finnish sawmills being disadvantaged in an increasingly competitive market.

The Consequences of an Unbalanced Market

In most forest products markets, suppliers and consumers of wood raw materials work together. Timberland owners sell large logs to lumber and plywood manufacturers and smaller logs to pulp and paper, pellet and OSB manufacturers. Sawmills use the logs they buy to make lumber then sell what's left to pulp and paper, MDF, particle board, and pellet manufacturers and power producers. Because wood flows in multiple directions and to and from many different participants, those operating in the forest products supply chain are interconnected and interdependent.

As a result of these symbiotic relationships, forest products markets are generally structured in a way that balances the various sources of supply and demand and allows for the free operation of supply and demand economics. When working at peak performance, balanced markets tend to create efficiencies and healthy profitability for all. When markets become unbalanced, however, and when one segment wields outsized power in the market, overall conditions deteriorate and lead to negative consequences for all.

Finland is, however, a current example of an unbalanced market. In Finland, large integrated forest products companies operate some smaller-scale mills that require smaller annual log consumption volumes (roughly half of the market). Since pulp production is their main business, they are large consumers of pulpwood and clean chips. In 2017, these companies had an operating profit of more than 10 percent; operating profit at standalone sawmills, the source of the other half of sawn wood production in Finland, stood at zero. These mills consume at least half of the saw logs in the market and sell clean chips to pulp producers.

On the supply side are Finland's timberland owners. According to Indufor, about 67 percent of total roundwood is sold by private non-industrial owners on a standing basis. These owners, seeking to maximize their profits, sell the right to harvest a defined area to the highest bidder. Because their resources far exceed the resources of an independent sawmill, the highest bidder most often turns out to be one of the large integrated forest products companies. These companies harvest all species and assortments from the land, use the pulpwood themselves and then market the sawtimber to independent sawmills, at ever-increasing prices.

Kai Merivuori notes that, "As the demand for pulpwood grows, the price of the sawlog has been illogically increasing. The price increase of pulpwood has been non-existent. Forest owners are attempting to maximise their stumpage earnings. It is easier to put out to tender log prices on a market with dozens of buyers than pulp wood prices on a market of just three buyers. The independent sawmill industry is left to foot the bill."

"Integrated companies benefit from minimized pulp wood prices because they use up practically all of the pulp wood entering the markets. Conversely, their share of logs is just half, with independent sawmills utilizing the other half. Thus, integrated companies are stuck with the bill for any pulp wood price rise, but only with half of the price rise for logs. Integrated companies have tied the price of pulp chips created as a sawmill side-product to the price of pulp wood, which means that they are buying chips produced from high-quality, expensive logs at a 70% cost reduction compared to the price of the raw material."

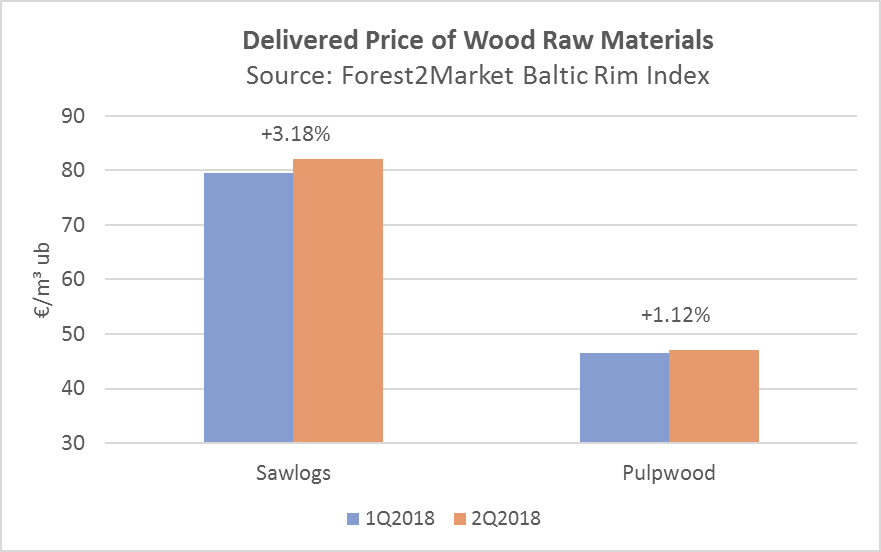

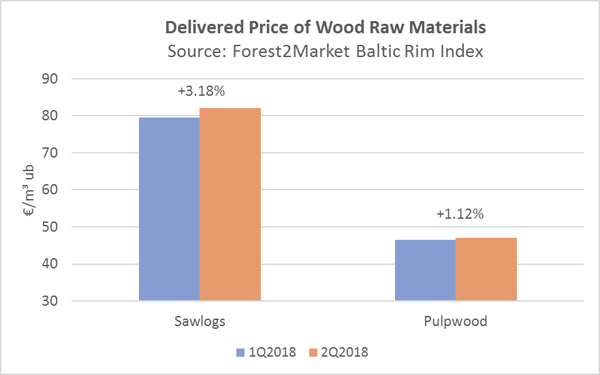

The effect in the market has been an escalation in the price of logs even as the prices for pulpwood and chips have remained flat. Though it is more muted due to the addition of harvesting and freight costs, these increases can also be seen in delivered prices. According to Forest2Market's data, log prices have increased 3.18% in 2018 and pulpwood prices have increased just 1.12%.

The result of the imbalance in the market is just starting to be felt. Recently, Junnikkala Oy, which operates sawmills in Kalajoki and Oulainen, announced it would suspend all timber purchases. In the announcement, Junnikkala specifically addresses the distorted market situation: if one compares the price for sawlogs in relation to the price of sawn timber to the price of pulpwood in relation to pulp prices, it is easy to see that the current market conditions are unsustainable. "The risks for the sawmill industry are high. That is why we told the public today that we will cease timber purchases." Word within the industry is that other independent mills may follow suit.

Importance of an Independent Market

This price dispute is partly due to the data that is used as a reference point when making wood raw material purchases. LUKE, the Natural Resource Institute of Finland, publishes the prices and volumes of stumpage purchases on a weekly basis. While this method provides some level of guidance to the market, it does not follow the modern best practices of other major forest producers around the world due to its:

- Lack of a representative sample: 80 percent of the data collected and aggregated for these statistics comes from the three largest integrated forest products companies. As a result, the sample is skewed toward the higher prices that these companies are extracting from independent sawmills.

- Pulpwood prices that are artificially low: domestic pulpwood prices have remained stable even though pulpwood imported from the Baltic region and Russia is typically more expensive.

Large integrated forest products companies supply the data then use the reported prices to negotiate their next contracts. The situation is advantageous for a handful of large companies, but it disadvantages the smaller producers (a majority of the market) who don’t participate. The situation, therefore, hurts rural development and the rural economy because it doesn’t foster a truly competitive and independent market.

A Path Forward

In the long term, the best way to ensure a balanced and transparent market is with high-quality data. To restore confidence and transparency to the Finnish sawmill industry, what is needed is a transaction-based pricing system—one that includes a representative sample of operators in the market. Forest2Market has deep expertise and 18 years of experience bringing transparency to markets around the world with its pricing services.

These services allow buyers and sellers in the market to clearly and confidently:

- Assess actual market prices and build strong partner relationships

- Compare their performance to market

- Define, measure and adjust strategic decisions based on real-time, actionable data

- Provide investors with transparent, high-quality data for reporting purposes

- Use data to assess acquisitions or dispositions and other investment decisions

For a long-term reprieve from high log prices, the independent sawmill industry will be best served by unifying to provide transaction data to an independent third-party that will aggregate the data and report it back to the market’s data contributors anonymously. Only then will the Finnish sawmill industry have the collective power to force a re-balance of the market, which will in turn drive the development of a healthy, independent and sustainable market.