Gordon Culbertson

Gordon Culbertson

Global demand for goods teaches us a lot about the malleability of market trends and developments, as well as new opportunities that exist to service these markets. The forest products industry is no different; if we know where to look, markets for forest raw materials exist in every corner of the earth. The advent of the export wood pellet industry in the US South, for instance, is a market that has grown from zero in 2008 to 3.6 million tons in 2014 due to European demand.

This reality also holds true for the industry in Baltic States (Estonia, Lithuania, and Latvia), a region with a combined timber harvest of about 30 million cubic meters annually, which is roughly equal to the annual harvest in the state of Alabama in the US South. The Baltic States have developed foreign partnerships and established outlets for their wood raw materials, but due to limited in-country market availability and capacity, the forest products industry in the region thrives in large part due to this export dependency.

Ownership Profiles

Though the industry in the Baltic States is robust, it is also subject to many of the same timberland ownership challenges that affect neighboring countries. Government or State-owned lands are substantial, and these lands are integral to the forest products industry in the Baltics. State forests supply about half of the log supply, sponsoring direct supply contracts with the industry that includes mill operators and log marketers.

But the Baltic States also have an interesting history concerning private land ownership that is still unfolding in the wake of the fall of the Soviet Union. For example, during the first few years of the Soviet occupation in Estonia (1940-41 and after World War II), land, real estate and other agricultural assets were entirely nationalized and/or collectivized by the regime. When national independence was restored in the early 1990s, a majority of Estonians supported the idea that unlawfully confiscated property must be returned to former owners and/or their successors, and be re-privatized.

The total number of parties entitled to restitution was 230,000—roughly 18 percent of the present population of Estonia— and the procedures for returning and compensating property began in 1991 in earnest. Most of the property to be returned or compensated fell under the category of land, including urban, agricultural and forestland, which made up 86 percent of the total value of all returned or compensated assets. Today, 1.5 million hectares (3.7 million acres) of agricultural and forestland, as well as 28 million square meters of urban lots, have been returned and privatized—over 99 percent of the estimated final number.

This recent and unique history has made the management of newly-privatized forestlands throughout the Baltic States difficult to say the least. Small parcels and the fragmented ownership have created production challenges, as a typical forest parcel is roughly 15 hectares (37 acres), and many parcels frequently include tillable farm or pasture land. While there are many private landowners that manage their own small parcels, an increasing portion of these tracts are owned by forest investors, who actively seek out these “new” owners and purchase their lands. This has resulted in a situation where a handful of TIMOs and mills manage a growing portfolio of forestland for marketing commercial timber.

Forestry Profile

Baltic States forests are slow-growing, northern latitude forests with an average annual growth increment of less than 8M³/hectare/year. These slow growth characteristics produce light colored, dense, high-quality wood that is prized for its attractive appearance and strength grades. Primarily composed of coniferous species such as Spruce, Pine and Birch hardwoods, State lands are sustainably harvested and carefully reforested and maintained due to the slower growth rates of these native trees.

The gentle terrain of the territory allows mechanized harvesting, and a good forest and highway transportation infrastructure makes hauling efficient. Due to largely favorable weather conditions for timber harvesting, logging and hauling can take place virtually year-round. Logs flow easily to mills or to ports by truck averaging 100-150 KM distances, and some pulp logs flow to the ocean port facilities via very reliable rail systems.

Not unlike other forest raw materials markets, the Baltics have standardized softwood saw log sizes and grades, including high-quality, knot-free standards as well as a variety of strength and visual grades for the manufacture of construction lumber.

Baltic States Market Profile

While the industry has a robust in-country forest harvest capacity, roughly 15 percent of harvests are pulpwood—a product that has very limited capacity for consumption in the region. Wood raw materials outside of valuable sawmill and plywood logs typically find their way to just a few outlets:

- Two Baltic States pulp mills utilize pulpwood and occasionally residual chips

- Most residual sawmill chips go to regional pellet mills

- Timber harvest residues are processed in the woods for heat and energy use

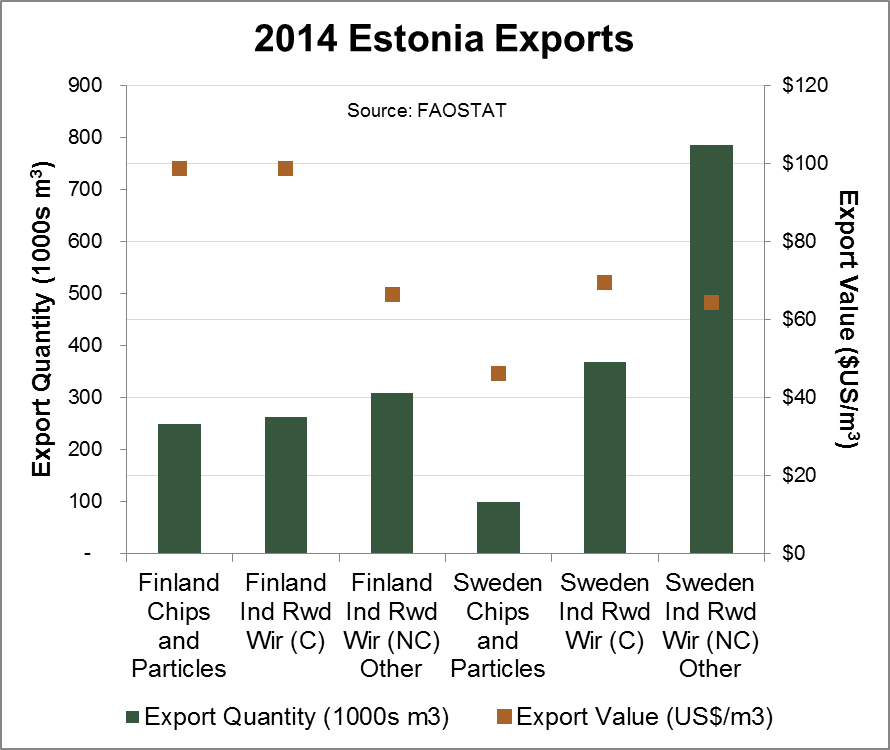

This abundance of pulpwood has created market challenges and opportunities in the Baltics. As noted above, the export market—especially to Sweden and Finland—is critical to the success of the industry in the region. Roughly 80-85 percent of pulpwood is exported to Sweden and Finland. Dedicated vessels for pulpwood and wood chip transportation deliver wood fiber to Scandinavian countries at a cost of around $22.5/cubic meter.

The Baltics have modern, well-developed sawmill, birch plywood, pellet and wood-based panel industries as well as an effective harvesting and transportation infrastructure. The focus on these industries is further evidenced by the fact that some “rough” Russian lumber actually flows into the region for additional processing, and lumber exports from the Baltics are significant; the UK is the largest lumber export partner, as well as other European countries, North Africa and Asia.

While pulpwood exports to Scandinavia are critical, the forest products industry in the Baltic States is demonstrating that mutually-beneficial partnerships are an efficient method for maintaining open markets while keeping the forests healthy and the industry profitable. Ongoing investments in pulp capacity in both Finland (MetsäGroup Äänekoski) and in Sweden (Södra in Mörrum and Värö) are likely to strengthen these partnerships in the future.