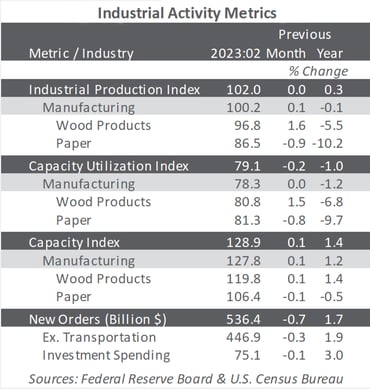

As a result of late-March revisions modifying the entire historical sweep of affected data series, total industrial production (IP) was reported as unchanged in February (+0.3% YoY; see table).

Interestingly, February’s initial, pre-revision print showed a 0.2% YoY decline—which would have constituted the first 12-month drop since February 2021. Manufacturing output edged up 0.1% in February 2022.

After January’s headline estimate was downgraded to -2.1% MoM (from 1.6%), new factory orders fell another 0.7% in February—the third decline in four months. Moreover, February’s +1.7% YoY was the slowest annual growth since February 2021.

In addition, transportation equipment was not the sole source of weakness. Non-transportation orders dipped 0.3% and business investment spending retreated by 0.1% (+3.0% YoY).

“With the surveys going from bad to worse and given the risks from the turmoil in the banking sector, we suspect that further declines in manufacturing activity still lie in store,” said Capital Economics’ Andrew Hunter. “Business investment is definitely a vulnerability for the economy in the event of a severe tightening in credit conditions,” Santander Capital Markets’ Stephen Stanley added.

We are forecasting QoQ changes in total IP to range between 3.1% and +2.6% annualized rates during the next 24 months. The overall average will balance at 0.0%.

Manufacturing Surveys Reflect Ongoing Contraction

The Institute for Supply Management’s (ISM) monthly sentiment survey of U.S. manufacturers reflected more-rapid erosion in the sector in March 2023.

The PMI registered 46.3%, down 1.4PP from February and the lowest print since the Great Recession (besides the pandemic lockdown). 50% is the breakpoint between contraction and expansion. Subindexes with the largest changes included new orders (-2.7PP), inventories (-2.6PP), and exports (-2.3PP).

Changes in S&P Global’s survey headline results were mixed relative to ISM’s. Both firms’ manufacturing reports showed contraction, and both services reports exhibited expansion. However, the two S&P Global reports showed rising PMI values whereas both ISM reports exhibited falling PMIs.

“The U.S. manufacturing sector continued to signal concerning trends during March,” wrote S&P Global’s Siân Jones. “Weak demand for inputs resulted in some relief for manufacturers as input cost inflation slowed again... inflationary concerns weighed on business confidence once again amid pressure on margins.”

The news isn’t all doom and gloom, though. As Jones continued, “Encouragingly, firms were able to expand factory workforce capacity again, albeit at only a marginal pace, as skilled candidates for long-held vacancies were found.”

Consumer and Producer Price Indexes, Forestry Feels the Pinch of Bank Turmoil

The consumer price index (CPI) rose 0.4% in February (+6.0% YoY—the smallest 12-month increase since September 2021). The index for shelter (+0.8% MoM; +8.1% YoY) accounted for over 70% of the all-items MoM increase.

Meanwhile, the producer price index decreased 0.1% (+4.6% YoY). Final-demand prices declined 0.2% in December 2022 and advanced 0.3% in January. February’s MoM decline was led by prices for final demand goods ( 0.2%).

Relative to the forest products sector, the price indexes show a mixed basket for year-over-year differences:

- Pulp, paper & allied products: +0.1% rise (+5.6% YoY)

- Lumber & wood products: No change at 0.0% (-14.9% YoY)

- Softwood lumber: +3.5% increase (-45.1% YoY)

- Wood fiber: -0.9% decrease (+0.2% YoY)

Banking turmoil and speculation about contagion risk dominated the March financial news cycle. The main focus was the Fed’s role in both creating the crisis and defusing perceived dangers to U.S. and global financial systems.

Trying to calm the markets on March 22, when announcing another 0.25PP federal funds rate hike, the Fed’s Open Market Committee (FOMC) maintained “the U.S. banking system is sound and resilient” while acknowledging that “recent developments… likely to result in tighter credit conditions for households and businesses.”

As long as unemployment remains low and inflation exceeds the target range, we see the Fed attempting to “thread the needle” on its dual mandate via further rate increases and other measures. After holding steady through February 2024, we expect the Fed to begin a series of rate cuts in March 2024.

Key Economic and Forestry Insights from Forest2Market

Forest2Market, a ResourceWise company, publishes specialized forecasting products tailored to those within the forest value chain.

This post was a small excerpt from our monthly Economic Outlook report. The EO is a macroeconomic indicator forecast highlighting general economic trends and related data. It also includes our experts’ insights and predictions about what to expect in several critical economic areas.

By understanding these economic indicators, you’ll get direct insight into elements such as potential future stumpage prices, buying and selling windows and more. Your business can develop more informed strategies on how to manage sales, negotiate purchases and better manage inventories in times of uncertainty.

Get in touch with our team to learn more about the EO and other forecasting tools to help your business do more.