Daniel Stuber

Daniel Stuber

Forest2Market’s Western Hemisphere Benchmark allows producers to compare their own raw material costs to the market average in one of many ways:

- By end-product segment. If you produce boxboard, you can compare your costs to the market average for all boxboard producers.

- By species. If you consume conifer (softwood), you can compare your costs to those of all other softwood consumers (the same is true for hardwood).

- By region. If you are in the US South, for instance, you can compare your costs to average costs in the US South.

- By global competition. Because markets for pulp and paper are global, you can understand your relative cost position compared with other producers in the Western Hemisphere.

Delivered Wood Fiber Prices for End-Product Grades

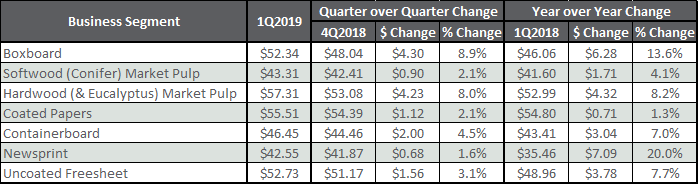

Wood fiber prices increased for all pulp and paper producers in 1Q2019, primarily driven by supply disruption in the southern US market and new demand in the US Northeast. Year-over-year (YoY), all segments saw increases in delivered prices, with double-digit percent increases for boxboard and newsprint producers. Costs for market pulp, containerboard and uncoated freesheet paper producers increased between 4 - 8 percent YoY. Fiber costs for coated paper producers were impacted the least, increasing by 1.3 percent.

Below are 1Q2019 delivered price results and average price changes compared to 1Q2018 and to 4Q2018 for various end-product segments:

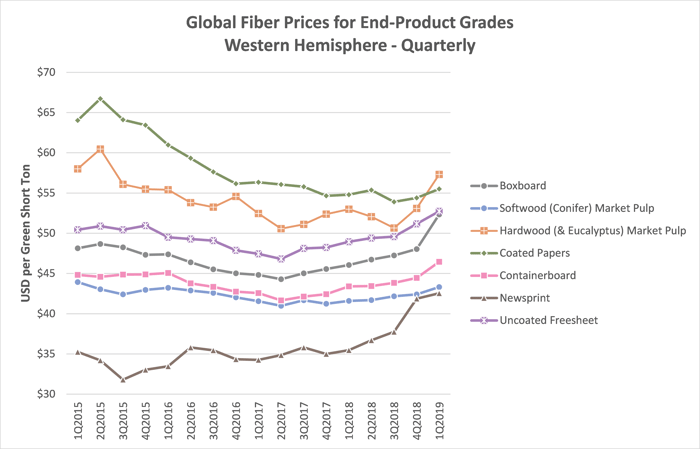

The following chart shows the trendlines for various end-product segments from 1Q2015 through 1Q2019. Prices were highest for coated paper and hardwood pulp producers, and prices were lowest for newsprint and softwood pulp manufacturers.

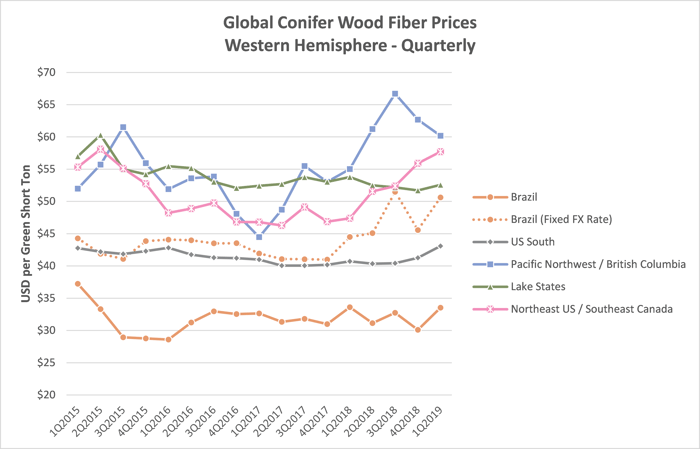

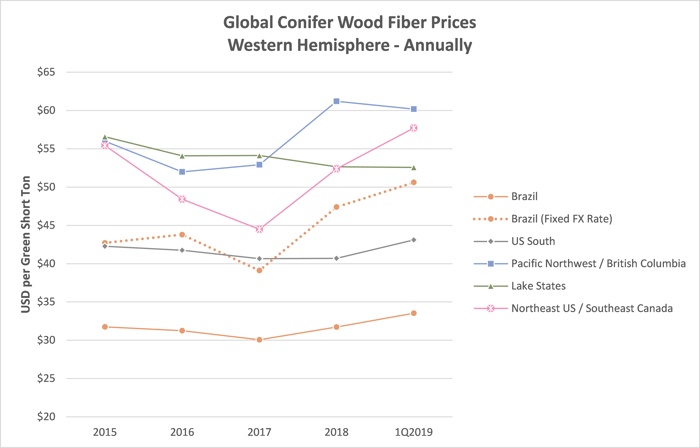

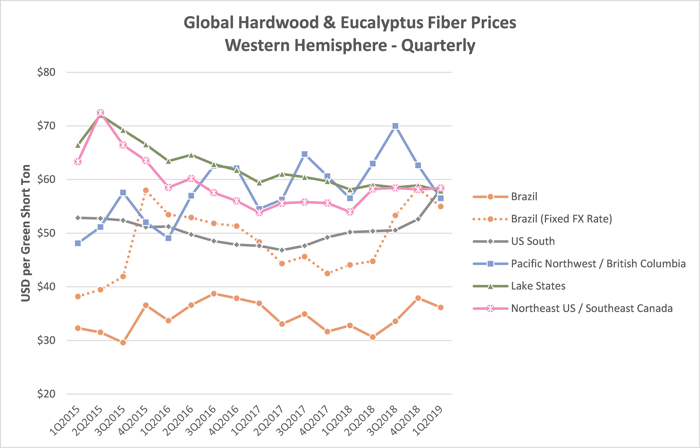

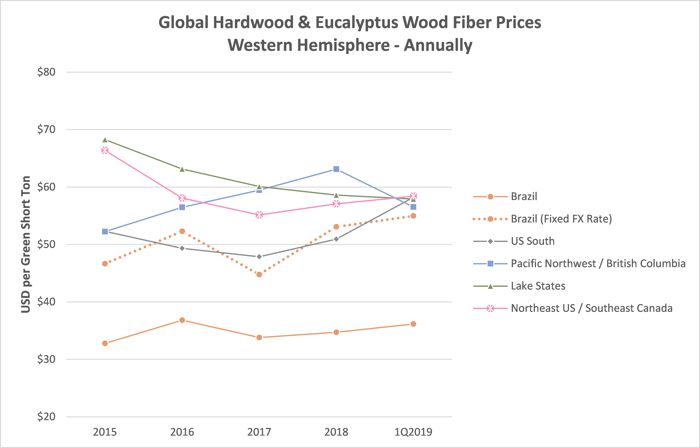

Delivered Conifer and Hardwood/Eucalyptus Wood Fiber Prices

Lowest Cost Regions: Brazil and the US South

On the Real basis, costs are increasing in Brazil due to increased demand for both conifer and eucalyptus. As Marcelo Schmid recently noted, eucalyptus stumpage prices per cubic meter (m³) in São Paulo have increased from R$37.05 in December 2016 to R$55.38 in March 2019, a 49 percent jump in just over two years.

While Brazil is still the lowest-cost region, this dynamic is primarily due to the depreciation of the Real against the US dollar (USD), which has kept the price of conifer relatively flat over the last five years on a dollar basis. In-country prices, however, have been on an increasing trend over the last five quarters since 4Q2017. For eucalyptus, prices over the last three quarters have increased substantially, even overwhelming the depreciation of the Real where dollar prices are now as high as they were in 2016 when the exchange rate was much lower. All of this is being driven by increased demand in the region.

Conifer price stability in the US South has been challenged in the last two quarters due to above-average rainfall levels that began during mid-2018—a period when mill inventories are typically low. Mills are just now beginning to show signs of inventory recovery and prices are expected to further decline. However, it is worth noting just how irregular prices were in 1Q2019, which marked a period where prices were the highest they have ever been since Forest2Market began reporting in 2007.

The extreme rainfall had the greatest impact on hardwood fiber in the US South. Prices have been on an increasing trend since a low in 2Q2017 but increased $2.07 per green short ton (GST) (4 percent) in 4Q2018 followed by a whopping $5.59/GST (11 percent) in 1Q2019, putting southern prices on par with hardwood prices in the other regions of North America. Like conifer, hardwood prices are expected to decline, but at a much slower pace as mills are still rebuilding severely depleted inventories.

Highest Cost Regions: Western North America West, Eastern North America

Conifer prices continue to trend higher in the Pacific Northwest (PNW) and British Columbia (BC) as demand remains strong amid the dwindling supply of residual chips in the region—particularly in BC, which continues to see sawmill closures and curtailments as more and more production exits the market. This has left some mills scrambling to find more expensive whole log chips, which is driving up price. Chip imports into BC from the US doubled in 2018 over 2017 as a result.

Conifer prices in the Lake States continue to slowly decline, however, prices are increasing in the Northeast as demand has expanded. Conifer prices had subsided in most of 2016-2017 as mill closures occurred, but demand (and competition) has reentered the market, most notably via Sappi’s conversion at its Sommerset mill in Maine. Hardwood pricing in the Lake States also continues to slowly decline as demand softens in the region. Since the beginning of 2018, however, prices in the Northeast continue to inch upward as demand strengthens in the region.

2019 Outlook

Volatility in the end product markets—a result of geopolitical tension, the US/China trade war and Brexit, among other issues—is creating a high degree of uncertainty in the global market. Early indications of a forthcoming recession in the US and an overall global economic slowdown are also factors. As a result, the dollar will weaken against the Brazilian Real. In-country prices are likely to retreat and will decline even faster on a dollar basis.

Conifer mills in the US South are expected to reduce production and will recover their inventories through the summer months, which will put downward pressure on fiber pricing as sawmills continue to reduce production due to decreasing demand for lumber. The reduction in sawmill byproduct chips will create additional demand for roundwood, which will slow the rate of decreasing prices. The southern hardwood market, however, remains a mystery. Keeping a careful watch on mill inventory levels will be the key to understanding price developments in the hardwood fiber market.

In the PNW and BC, sawmill curtailments and closures are accelerating, which will reduce supply of sawmill byproduct chips and drive demand for whole tree chips. This product mix change will cause total fiber prices to increase.

In the Lake States, we expect to see continued flatness (or a moderate decrease) in the market for both conifer and hardwood fiber. In the Northeast, we expect the market to settle as prices will decrease for both species.

Methodology

For the Western Hemisphere Benchmark, we report stemwood (i.e. tree-length pulpwood or bolts) and wood fiber chips (wood fiber chips only, not energy chips) delivered through the supply chain to the end producer’s mill gate. We then convert the price and unit of measurement to US dollars/short ton. For stemwood, we also convert the product to a wood fiber chip equivalent and add a cost of five US dollars/green ton for debarking and chipping to the chip pile. We then compute a weighted average price for all combined wood fiber.