After falling to a nine-month low in June, US housing starts rebounded slightly and less than expected in July, suggesting the housing market will likely remain flat for the remainder of the year. Despite solid jobs numbers and wage growth, housing activity appears to have has stalled due to rising mortgage rates and an increasingly tight supply of homes that has driven prices ever higher.

Housing Starts, Permits & Completions

After dropping 12 percent in June, US housing starts rose just 0.9 percent in July to a seasonally adjusted annual rate (SAAR) of 1,168,000 units. Data for June was revised down to show starts declining to a 1.158 million-unit rate, the lowest level since September 2017, instead of the previously reported 1.173 million-unit pace.

Single-family starts accounted for 862,000 units, which is 0.9 percent above the revised June figure of 854,000, and starts for the volatile multi-family housing segment gained 0.7 percent to a rate of 306,000 units in July. Privately-owned housing authorizations inched up 1.5 percent to a rate of 1,311,000 units in July. Single-family authorizations increased to 869,000, which is 1.9 percent above the revised June figure.

Privately-owned housing completions were flat at a SAAR of 1,188,000 in July. Regional performance was down across the board as confirmed by the US Census Bureau report. Seasonally-adjusted total housing starts by region included:

- Northeast: -4.0 percent (-6.8 percent last month)

- South: +10.4 percent (-9.1 percent last month)

- Midwest: +11.6 percent (-35.8 percent last month)

- West: -19.6 percent (-3.0 percent last month)

Seasonally-adjusted single-family housing starts by region included:

- Northeast: -5.7 percent (+3.1 percent last month)

- South: +2.0 percent (-6.8 percent last month)

- Midwest: +22.3 percent (-29.1 percent last month)

- West: -10.0 percent (-3.6 percent last month)

The 30-year fixed mortgage rate decreased from 4.57 to 4.53 percent in July, and the National Association of Home Builders (NAHB)/Wells Fargo builder sentiment index ticked down by one point to 67 in early August.

Market analysts were unimpressed with July’s numbers: “The bigger picture, though, is less encouraging. The trend in permits is flat, at best, and the downward trend in the NAHB index of homebuilder sentiment and activity suggests that no near-term recovery is likely,” said Ian Shepherdson, economist at Pantheon Macroeconomics. “Housing is the sole weak spot in the economy right now, and that’s probably not going to change,” he added.

Peak Housing?

Although single-family starts appear to be maintaining a relatively linear upward trend, multi-family starts peaked in mid-2015 and have undulated lower since. As a result, total starts have been increasing along a decelerating trend since 2013. Delphi Advisors provide analytical insights about this topic in Forest2Market’s most recent issue of The Economic Outlook:

June’s sharp falloff in both single- and multi-family starts followed by July’s lackluster gain has prompted a rash of speculation, including references to “peak housing,” over whether construction has topped out for this cycle. Aaron Terrazas, senior economist at Zillow, interprets the slump in starts as “a sign that builders aren’t anticipating as much demand from buyers going forward, and/or that mounting cost headwinds are finally taking their toll.”

Based on the behavior of the exchange-traded fund iShares US Home Construction (ITB), which tracks a basket of 47 US homebuilders and construction-related companies, investors apparently agree. As of August 3, ITB’s share price had fallen nearly 19% from mid-January’s peak. Real private residential investment (PRI) declined for a third quarter in 2Q2018; as a percentage of total GDP, the decline has been in place since 1Q2017. Although both metrics have receded only modestly from their corresponding recent peaks, they nonetheless paint a potentially disconcerting picture.

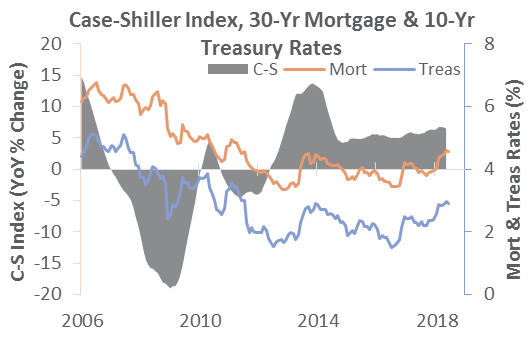

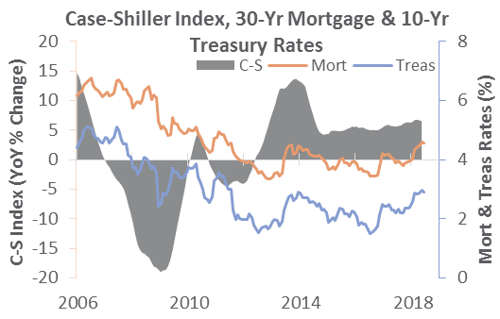

The drops in starts and sales may be indicating that high home prices and rising mortgage rates have caused demand to tip over. June’s median new-home sales price ($302,100) was 12.0% below November 2017’s record high, but the median resale price (a new high of $276,900) was up 5.2% YoY. The resale YoY change was slightly lower than the 20-city Case-Shiller Index, which rose 6.5% in May, but still nearly double the YoY change in the CPI. And, to paraphrase a point made by economist Joel Naroff, as (especially new) home sales go, so goes ancillary retail spending.

Last month, we highlighted research by Delphi Advisors showing housing supply has not kept up with population growth. Delphi has subsequently added to those initial findings, and estimated that population growth might have supported construction of an additional 380,000 single-family and 450,000 multi-family units. “Perhaps this is a piece in the puzzle that explains why purchase- and rental-price affordability continue to be issues in many parts of the country,” concluded Delphi Advisors’ analysts.

Additional multi-family construction seems justified. The Urban Institute released results of a study quantifying several reasons why the Millennial cohort continues to wait longer than previous generations to own a home, including: delayed marriage and child bearing, education debt, and high rent. Another factor may be that 68% of Millennial homebuyers are experiencing buyer’s remorse. It seems plausible to imagine that communicating these regrets may be encouraging acquaintances to continue renting. In any event, more rental units would help reduce the growth rate of rents, in turn improving the ability—for those ultimately desiring to buy—to save for a future down payment

.