Daniel Stuber

Daniel Stuber

As we recently noted in our detailed study of the wood residuals market, it’s nearly impossible to overstate the impacts—both immediate and long-term—that the Great Recession of 2008 had on the North American forest products industry. The effects in the US South, in particular, have created a market situation with both advantages and disadvantages for various stakeholders in the supply chain.

In the aftermath of 2008’s financial collapse, southern sawmills were forced into survival mode. The mills that survived invested in new technology that improved efficiency and lowered costs. At the same time, as demand dwindled and log prices collapsed, landowners simply chose not to sell timber, opting instead to wait out the down cycle. A strange thing happened as a result of this confluence. As landowners waited for a recovery, trees grew larger and larger and mills—owing to their new-found efficiency—simply used fewer trees.

The net result after 10 years: Southern forests have more and larger trees, and sawtimber prices in the region are virtually unchanged since 2007.

There are signs that things are beginning to change, however. With forecasted slow, steady increases in housing starts and increased sawmilling activity across the South, what does the future for lumber look like?

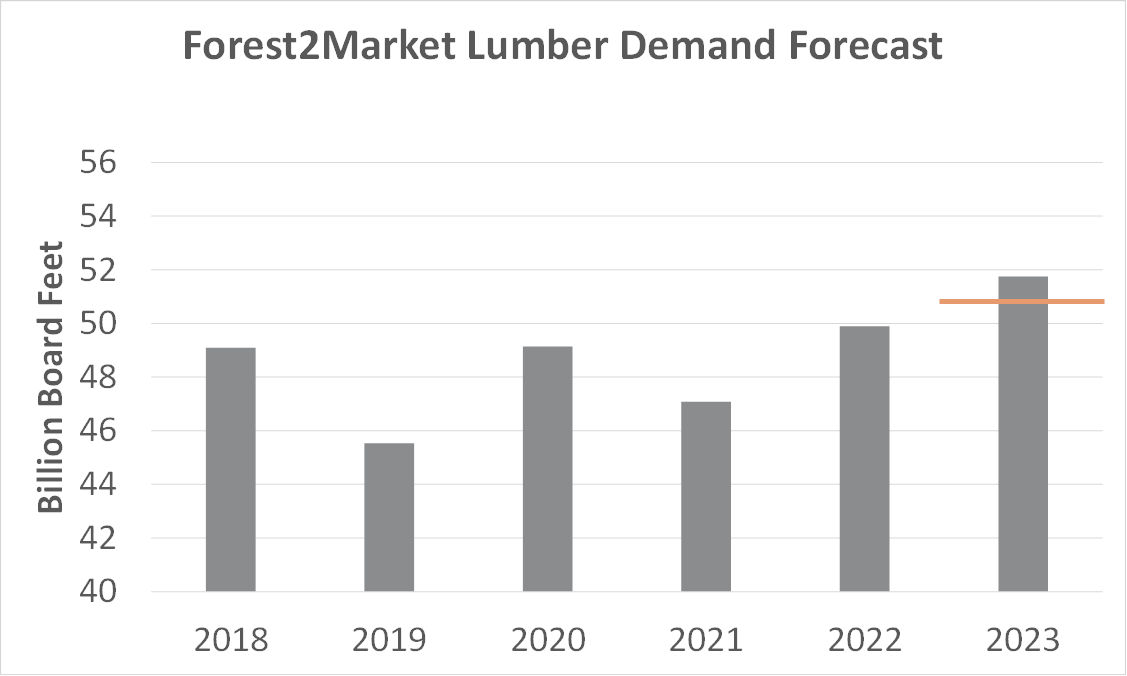

Lumber Forecasts

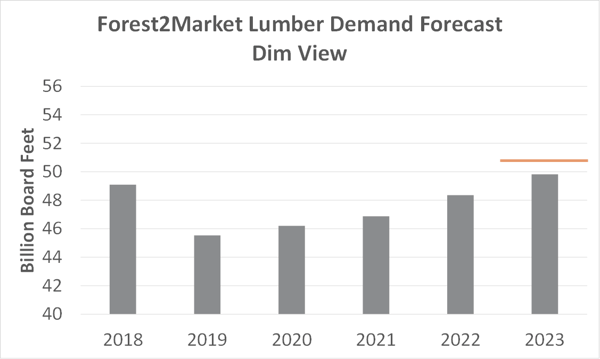

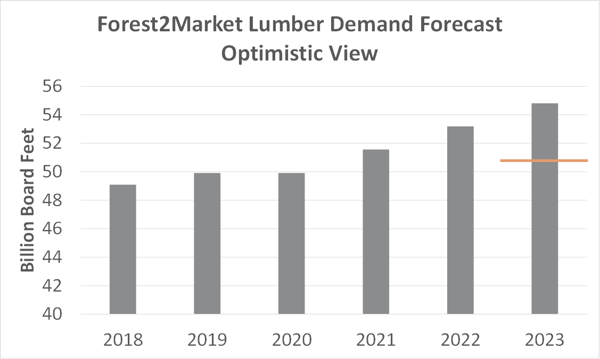

With all of the uncertainty surrounding global markets of late, we have to build some degree of variability into forecasting lumber demand over the next few years. Forest2Market created three different models to account for this variability: A view based on current performance and market trajectory, a dim view that accounts for decreased demand and an optimistic view that accounts for increased demand.

Our current trajectory model suggests that by 2023, housing starts will average 1.262 million units, remodeling will increase at 4.8 percent annually and GDP will increase at 2.3 annually. In this scenario, annual demand for lumber will increase to just under 52 billion board feet (BBF). When considering current southern capacity plus new greenfield/upgrade announcements, the market will be about 1.0 to 1.5 BBF short—equivalent to the production volumes of roughly 6 or 7 mills.

If, however, housing starts are fewer (1.25 million units), remodeling shrinks (2.5 percent) and GDP growth is just 2.0 percent, we will have an oversupply of roughly 1 BBF in capacity.

In the optimistic view with less market volatility, housing starts will average 1.350 million units, remodeling growth will be 4 percent and GDP growth will be 2.5 percent. Current mill outputs plus announced capacity will subsequently be roughly 3.5 BBF short of demand—equivalent to the production volumes of roughly 15 mills.

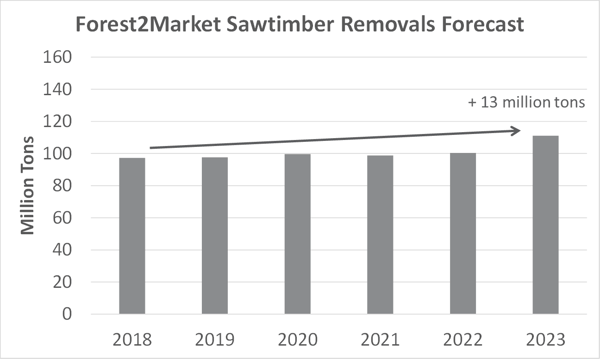

Sawtimber Removals Forecast

All of these scenarios are likely to affect sawtimber prices in the future—some more than others. Any increase in removals in combination with expanding mill capacities will drive regional sawlog prices higher, especially in areas with increased local competition for the pine resource. To meet the jump in demand, we project at least 13 million additional tons of removals over the next 5 years.

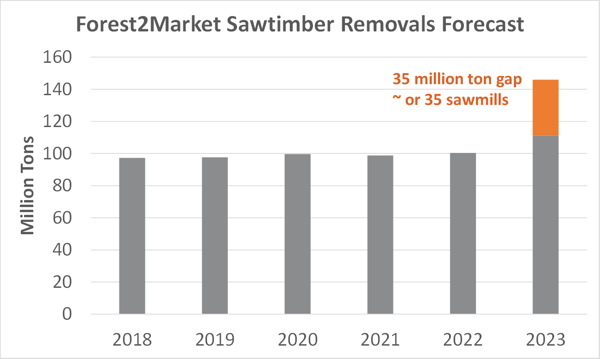

However, regional growth will still outpace demand (and removals). We project a 35 million ton gap where we would need 35 new sawmills—or equivalent exports—to make a significant dent in the growth-to-removals rate.

What will these forecasts mean for those stakeholders in the southern forest supply chain? In the next installment, I’ll look at the supply dynamics that make the US South home to such a vibrant forest industry as well as the future implications for both landowners and mill facilities.