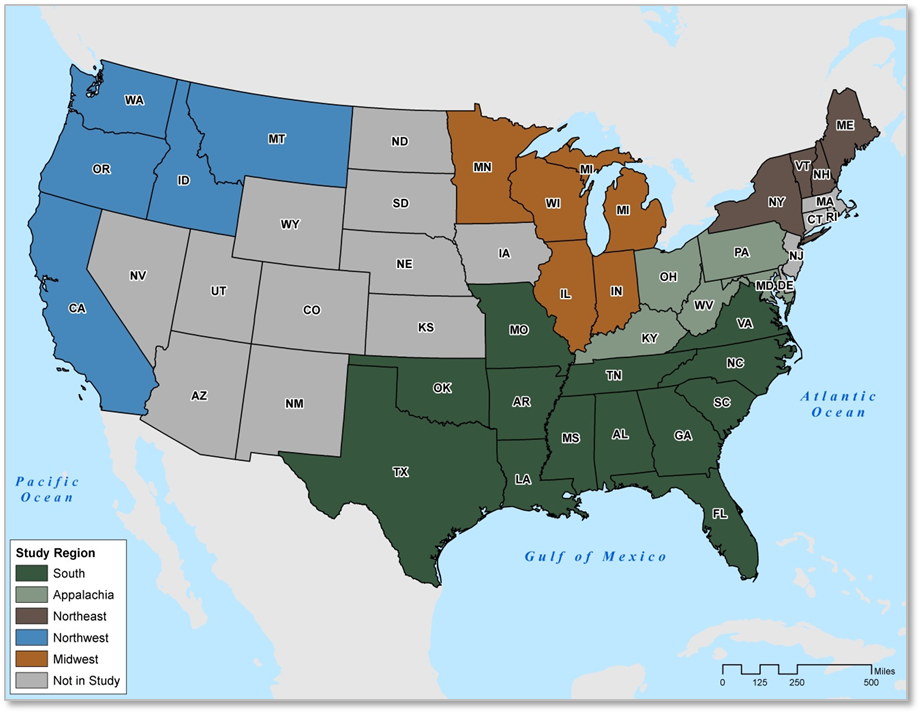

Forest2Market recently completed an economic impact study for the National Alliance of Forest Owners (NAFO), which quantifies the contribution that forestry-related industries make to state, regional and national economies, and analyzes the most forested regions of the United States based on the most recent year of data available (2016). The following map identifies the regions that were the subject of the study.

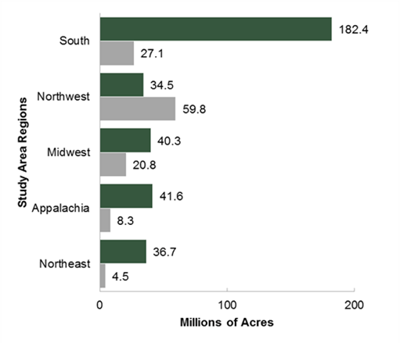

Of the 1.2 billion acres of land in the study area, 563.0 million acres (45%) are forested. Most (81%) of this forested land is classified as timberland according to the definition under the US Forest Service Forest Inventory and Analysis (FIA) program. Timberland covers 455.9 million acres (36.6%) of the study area. 46% of timberland is located in the South, which also contains 48% of all forested land.

Regional Timberland Ownership Profiles

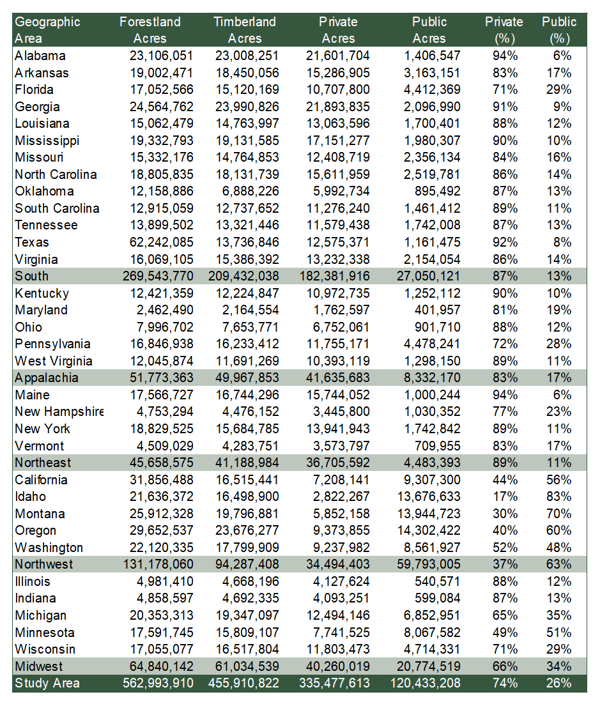

Of the 455.9 million acres of timberland within the 32-state study area, 335.5 million acres (74%) are privately-owned while only 120.4 million acres (26%) are publicly-owned. This translates into a much stronger economic impact associated with private timberlands.

As a whole, 74% of timberland in the study area is owned by private entities, such as Timberland Investment Management Organizations (TIMOs), Real Estate Investment Trusts (REITs), corporate entities and private landowners (Figure 2-5). Figure 2-6 shows the relative amounts of privately-owned timberland acres relative to publicly-owned timberland in each region.

Roughly 54% of privately-owned timberland in the study area is located in the South. Regionally, the Northeast and South have the highest percentages of private ownership at 89% and 87%, respectively. Appalachia has a slightly lower percentage of private ownership at 83%, and 66% of timberland is privately-owned in the Midwest. Only 37% of timberland in the Northwest is privately-owned.

The table below shows the total timberland acres, privately-owned acres, publicly-owned acres and the percent private versus public acres by state in the study area. In the South, Georgia has the highest number of private timberland acres at nearly 21.9 million while Oklahoma has the fewest at just under 6.0 million acres. Alabama has the highest percentage of privately-owned timberland acres at 94% and the second highest number of private acres (21.6 million). Florida has the lowest rate of private ownership at 71% and the second fewest private acres at 10.7 million.

In the Appalachian region, Pennsylvania has the most private timberland acres (11.8 million), and Maryland has the fewest (1.8 million). At 90%, Kentucky has the highest percentage of privately-owned timberland while Pennsylvania has the lowest percentage at 72%.

In the Northeast, Maine has both the most private acres (15.7 million) and the highest percentage of private ownership (94%). New Hampshire has the fewest private acres (3.4 million) and the lowest private ownership rate (77%).

In the Pacific Northwest, Oregon’s nearly 9.4 million acres make it the most prolific for private ownership, but Washington is a close second at almost 9.2 million acres of private timberland. At 52%, Washington has the highest rate of private ownership in this region. Idaho has the lowest at 17%.

In the Midwest, Illinois and Indiana have the fewest private timberland acres at around 4.1 million acres each. However, they also have the highest rates of private ownership in this region at 88% and 87%, respectively. Michigan has 12.5 million privately-owned timberland acres, which is the highest in this region. Minnesota has the lowest rate of private ownership at 49%.

Regional Timberland Class Profiles

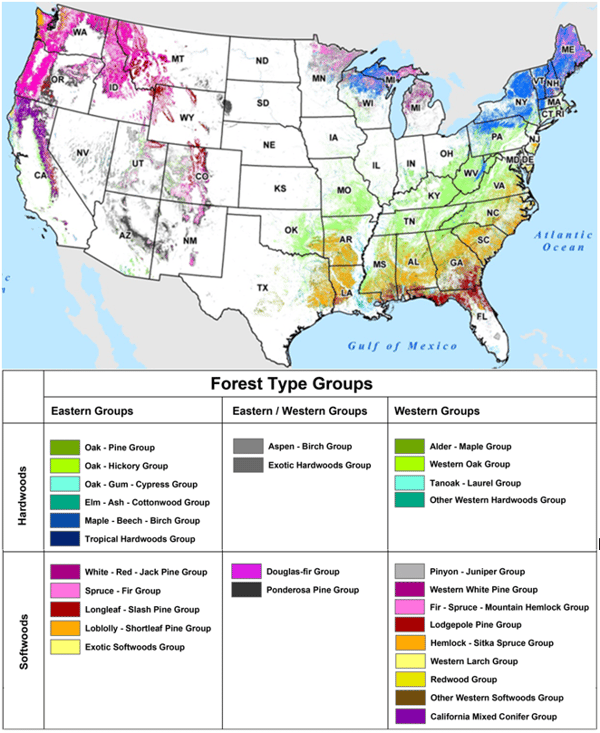

The map below, adapted from a U.S. Forest Service map, shows the types of forests that predominate in the contiguous (Lower 48) states.

Conifer (softwood) species are commonly used in manufacturing lumber, plywood, panels, paper and paperboard. Hardwood species are commonly used for making furniture, flooring, veneer, millwork, pallets and printing grades of paper.

Softwood forest types, such as Loblolly/Shortleaf Pine and Longleaf/Slash Pine, predominate in the coastal plain regions of the South while the Oak/Hickory hardwood forest type is more common in the northern, more mountainous areas. The Oak/Hickory forest type continues into Appalachia where scattered pockets of the Maple/Beech/Birch hardwood forest type also occur.

Extending north from Appalachia, the Maple/Beech/Birch hardwood forest type dominates the Northeast where the softwood Spruce/Fir forest type also occurs. Like the Northeast, the Midwest is a mixture of hardwood forest types, including Aspen/Birch and Maple/Beech/Birch, and softwood forest types, such as White/Red/Jack Pine and Spruce/Fir. Some scattered areas of Oak/Hickory exist in the lower Midwest.

Due to differences in climate and elevation, forest types in the Pacific Northwest vary from those in the other regions. The most common forest types are the softwood species of Douglas-fir, Fir/Spruce/Mountain Hemlock, Hemlock/Sitka Spruce, Ponderosa Pine and Mixed Conifer.

Read the full study and use the interactive state data feature on NAFO's website.