Pete Coutu

Pete Coutu

In his popular blog post published in early 2015, Daniel Stuber asked a question related to wood supply chain costs that is as relevant now as it was then: When oil hits $50 per barrel, shouldn’t delivered wood fiber prices fall? His conclusion—that other factors, including weather, demand and inflation exerted more influence on delivered fiber prices than oil and diesel prices—was well-reasoned and reinforced by data. But does the conclusion still apply in stumpage markets and economic conditions that may be significantly different than they were four years ago?

Forest2Market is in the business of helping companies make better operational decisions through the application of unique, proprietary datasets that drive efficiency improvements and profitability. To assist in this process, we benchmark price to help our customers manage their supply chain costs. In this capacity, I decided to revisit the topic and take a fresh look based on an additional four years’ worth of data using Forest2Market’s Economic Analysis tool available via SilvaStat360.

Oil & Diesel Prices

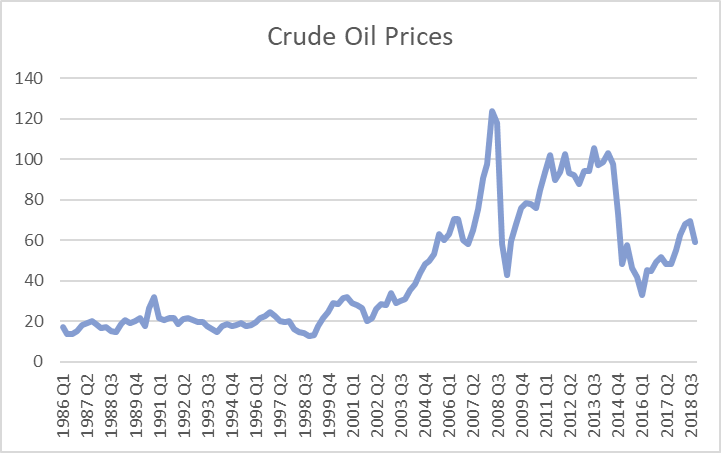

Oil and diesel prices vary on a monthly basis and over time, it seems as though volatility in these prices is higher now than it was 25 or 30 years ago. Analyzing crude oil from 1986 – 2018 in the chart below, prices look fairly stable from 1986 – 2002. Thereafter, we see some clear anomalies—the period surrounding the Great Recession of 2008 and again in 2014—but overall, crude oil prices appear to be significantly more volatile from 2006 – 2019.

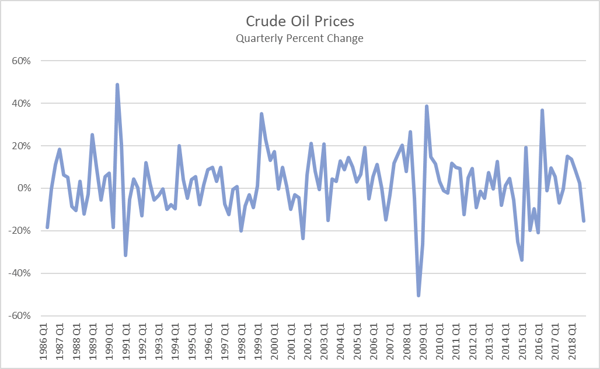

However, upon closer inspection, the details in the numbers don’t back up that assumption. The chart below shows the percent change in crude oil price from quarter to quarter over the same time period. While prices are significantly higher from roughly 2005 onward, the volatility is fairly constant.

What can this data tell us about how fuel prices impact the wood fiber supply chain? The supply and demand of logs and wood fiber is ultimately what drives the price of these products on the market, which is always independent of fuel price. However, the cost of producing the logs and fiber is not independent of fuel price, or the price of any other factor that goes into generating these products; at some level, steel, labor, tires, etc. all affect the cost of producing logs and fiber. The interplay of these shifting factors eventually impacts supplier margins.

Margins Drive Process Improvements

Forest2Market measures stumpage, freight, cut-skid-load and “margin” as cost components in its delivered price benchmarks. In the case of a wood fiber supplier, the margin component is best viewed as an unfixed indicator of supplier profitability. For example, should the price of wood remain flat between two time periods while the price of diesel goes down, the supplier makes a higher margin. In such a scenario, there is generally less incentive to improve efficiency. If the opposite happens and diesel prices surge as they did in 2007, the supplier’s margins will get squeezed.

While this scenario will temporarily impact supplier profitability, it will also force efficiency improvements in the supply chain. As a result, the supplier may find cost-cutting solutions to maintain profitability, including reducing haul distances, working longer hours, or even investing in new technology such as lighter trailers, faster processing equipment or other “game changing” solutions to keep operating costs low. This works on the consumer side of the supply chain as well, when wood price increases and supplier margins expand. Consumers have a greater need to affect efficiency improvements in their process.

What about Delivered Prices?

While Forest2Market maintains strict neutrality in reporting cost components in its benchmarks (there is no “good” or “bad” margin cost), the insights it provides into the forest supply chain allow individual participants—both suppliers and consumers—to measure their own performance against the industry average and the local market. To get a full-spectrum view of supply chain cost component performance, I will publish a follow-up installment to this blog post that analyzes delivered wood prices since 2011 compared to oil/fuel price performance.