2 min read

As the incredibly mild winter of 2015 makes its all too subtle transition into spring, current Asian log buying trends coupled with favorable weather conditions have resulted in an improved market position for the forest products industry in the Pacific Northwest region. Notably, we are beginning to see a significant shift in log merchandising, flow and log yard inventories.

The favorable climate during Q1 has also helped to create ideal operating conditions for regional mills. Most Westside operations competing directly with the export markets were able to fill their log yards due to below-average rainfall, and mills in the Inland region took advantage of warm temperatures and weight restriction reprieves to schedule just-in-time deliveries.

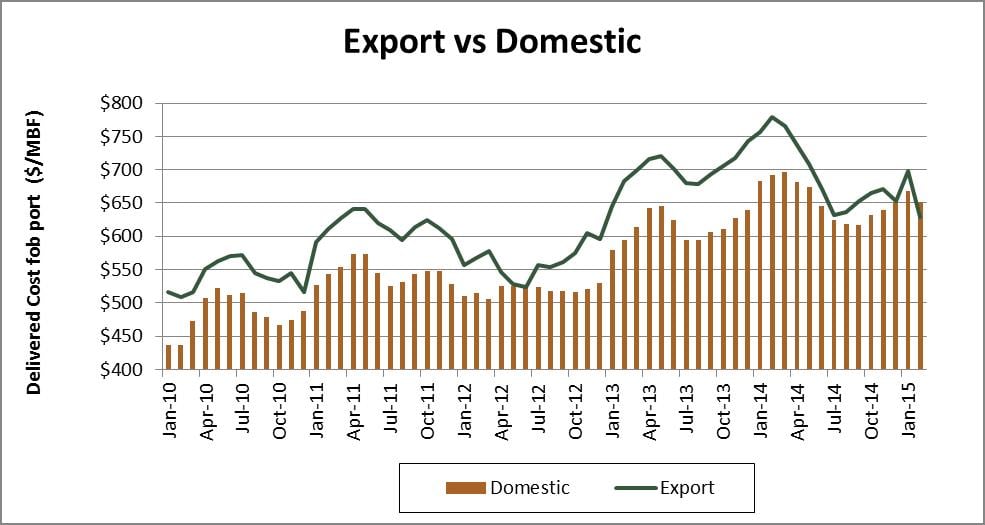

Pacific Northwest Log Markets: Export and Domestic

Few PNW exporters are sustaining steady flows of logs into their yards. Most have tightened buying activity and are carrying limited inventories as they wait for improved market conditions. As Asia continues to source logs from alternative global suppliers (a move necessitated by the relative strength of the US dollar abroad), demand for logs from the Pacific Northwest has eased and domestic mills are benefitting due to reduced prices.

Taking a closer look at the data behind this current shift in log markets, we are beginning to see a reversal of price points. As the following graph illustrates, domestic log pricing has historically “chased” the increasing demand of the export trade – a trend that ended abruptly in January, 2015. For the first time in five years, domestic log prices are outpacing export pricing.

In the near term, China’s log demand will continue to be serviced in large part by southern hemisphere producers. US domestic mills will continue to make capital improvements and increase capacity, keeping pressure on log markets encouraged by improving domestic economic numbers.

From a domestic market perspective, 2015 US housing starts data is undoubtedly the most anticipated and analyzed statistic for the forest product industry. As the following chart shows, new starts hit 1 million in 2014 and are expected to exceed that level this year. The increased shortage of existing units in parts of the US will provide real potential for construction efforts to exceed expectations. Only time will tell if the forecasts are accurate, but with cooperative weather patterns during the remainder of 2015, the indicators look promising.

Q1 2015 Weather Effects and the PNW Timber Outlook

Weather patterns during Q1 created a situation of extremes in the US. As noted earlier, the PNW had mild, dry conditions that directly benefitted the industry. Conversely, the Midwest and Northeast saw colder than average temperatures and record snowfall in some areas. What does this mean for the industry as we approach warmer seasons, and what is the takeaway for PNW timber operations?

While Mother Nature will have the final say, it would be prudent to let history be our guide. Here’s what we do know as we head into Q2 and beyond:

- Record-low regional snowpack and YTD precipitation levels will undoubtedly result in increased fire potential and a reduced summer logging season.

- Increased fire and drought conditions will foster a continued sense of urgency for cooperative groups across the western states to develop improved natural resource management strategies and be better stewards of our forest, water and other natural resources on our vast public lands.

- As lumber markets improve into the fall, weather conditions could hamper log inventories. Other global log competition factors may arise as well.

Here’s what we don’t know: just how unpredictable next winter will be.

Balanced Supply Results in Continued Market Tension

We are currently seeing a significant softening in wholesale China log markets, Japan DF exports. At the same time, overall Domestic log demand remains somewhat stable.

The imperative task for the remainder of 2015 will be balancing the existing PNW export demand and increased domestic needs with a tightening supply. We could see a reduction in harvest levels from certain private timberland owners, creating an opportunity for public timber managers to fill the need with non-exportable log and stumpage sales. As domestic mills increase lumber production to accommodate a growing (and unthawing) US construction market, we will continue to see price tension escalation as log supply tightens in late summer and early fall. As for the winter, I’d plan for more extremes.