Joe Clark

Joe Clark

We are more than a decade removed from the depths of the Great Recession and despite 10 years of solid growth, timber prices across the South have still not returned to the pre-crash levels of the early 2000s. The primary reason for this is rooted in a basic supply/demand relationship, as the trees are simply growing faster than the market for them.

While many mills were forced to adapt and improve efficiencies in the immediate aftermath of the Great Recession, many landowners simply pulled their timber off the market and waited it out in hopes that prices would trend higher in the future. This combination has caused the total volume of logs on the stump throughout the US South to rise unimpeded over the last decade. This oversupply combined with improved mill efficiencies is keeping log prices low, even as demand for lumber and sawmill production slowly increases.

The housing market remains a mystery I have yet to crack, however log data from the South points to some promising trends for southern timber owners.

Defining the Price ‘Rebound’

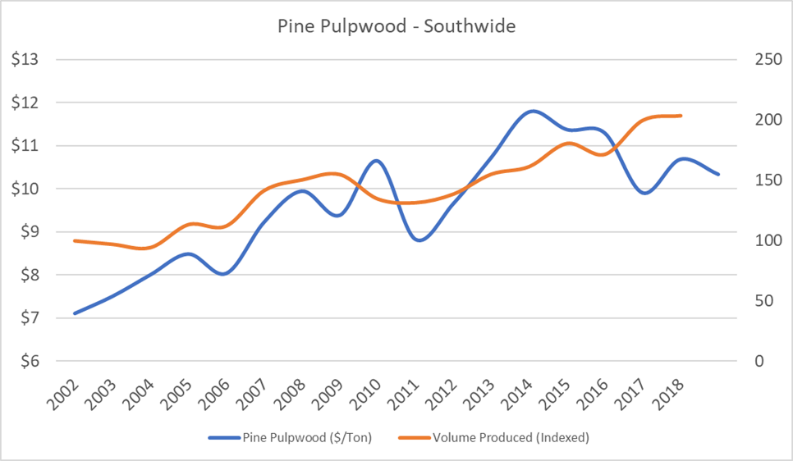

Solid wood manufacturing and demand for sawtimber has always informed the way we tend to think about the overall price driving timberland ownership and investment. While pulpwood has traditionally been viewed as a “come-along” byproduct of a sawtimber harvest, the market for pine pulpwood across the South has surged over the last decade. New demand driven by evolving markets and changing end-use products has made pine pulpwood the lynchpin that is now responsible for the overall stumpage price increase in weighted southern timber prices over the last 10 years.

As demand for pulpwood has increased, the average stumpage price has increased in tandem with production volumes. There have been some periods of volatility since 2002 driven in part by the Great Recession and weather conditions, but pine pulpwood prices have continued to trend upward. On a Southwide basis, pine pulpwood prices are up 47% while pine sawtimber prices are down 35% since 2002.

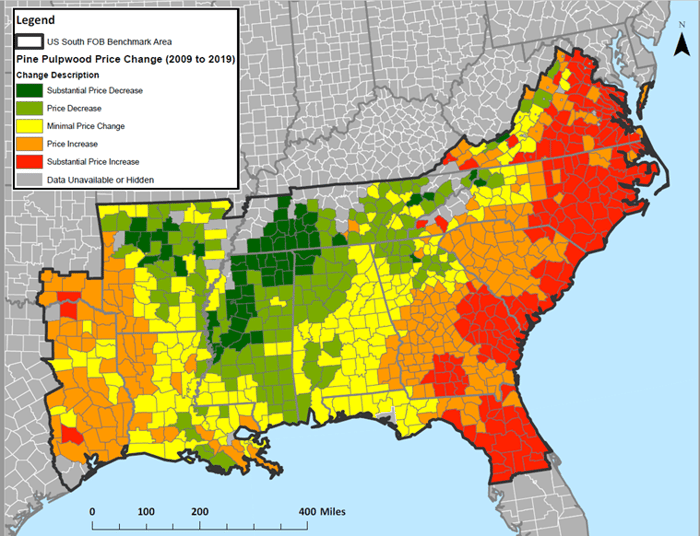

However, the recovery of the pine pulpwood market has not been consistent across the South. As the heat map below illustrates, there are pockets throughout the region with varying levels of pulpwood demand, which has affected pulpwood stumpage prices. In general, the coastal areas have been the strongest markets for the pine pulpwood revival. For example, a large swath of area from southeastern Georgia into northeastern Florida has seen pine pulpwood prices jump nearly 150% since the onset of the Great Recession.

While this trend doesn’t include the big sawtimber rally that many landowners have awaited, it nevertheless represents a new source of long-term demand for a southern a timber product that is driving the current rebound.

New Demand, New Markets

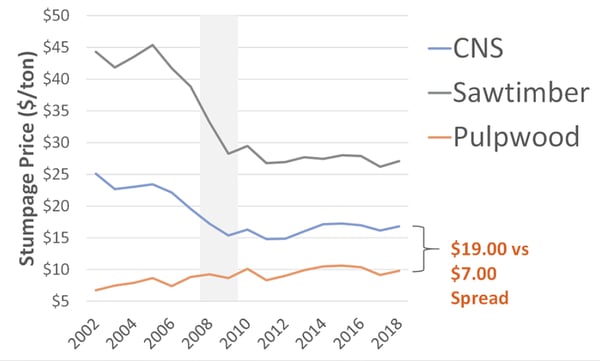

During the early years of the economic recovery, pulpwood really propped up the weighted average timber price throughout the South, and this dynamic continues as we see the market grow stronger and the gap between pine pulpwood, chip-n-saw and sawtimber has narrowed.

Notice that the trend for CNS has largely followed that of pulpwood since 2014. In especially hot markets, strong demand for pulpwood is squeezing the CNS market as some pulp mills are even choosing to reach up into the CNS category for fiber. What segments are driving this demand?

The Amazon Effect: Containerboard

Containerboard is a specific type of paperboard that is manufactured for use in the production of both linerboard (facing) and corrugating medium (fluting), the two wood fiber components that make up cardboard boxes. According to the American Forest & Paper Association, more than 95% of all products in the US are shipped in cardboard boxes, which are made from high-strength softwood fiber.

This product is very well-positioned in the growing e-commerce market, as online orders arrive in high-grade cardboard boxes to prevent damage during shipping. Since most containerboard is made from softwood fiber, the e-commerce phenomenon is sustaining demand for softwood residual chips and pulpwood as manufacturers of containerboard products prefer softwood fiber because of its strength characteristics.

Over the last several years, this segment has increased global production by nearly 2% annually and demand for containerboard is increasing at an annual rate between 2-4%. Demand trends look favorable for the future as well; e-commerce sales are expected to increase from 10.2% of all retail sales to 17.5% in 2021.

Population Boom: Fluff Pulp

High-quality fluff pulp is an absorbent material made from pine pulpwood fiber that is used globally in a variety of applications such as feminine hygiene products, baby diapers and adult incontinence products. While this is a relatively small market at 6 million tons currently, worldwide demand is increasing at 4% annually. This is a clear example of a situation where a change in customer preference has not changed the total demand for a wood raw material, but rather has shifted the demand from one product (hardwood pulp) to another (southern conifer pulp).

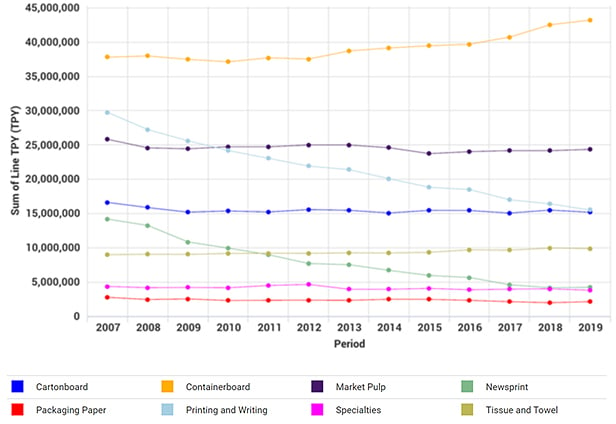

North American Pulp & Paper Production

Renewable Energy: Industrial Wood Pellets

One of the most significant developments in the southern pulpwood market over the last decade has been the addition of industrial wood pellet mills in the US South. While pellet producers consume residual chips and pulpwood, most prefer sawdust and shavings as their primary feedstock since these fine materials require less effort to process. However, the emergence of large pellet mills in many cases has made the need for pulpwood a supply necessity.

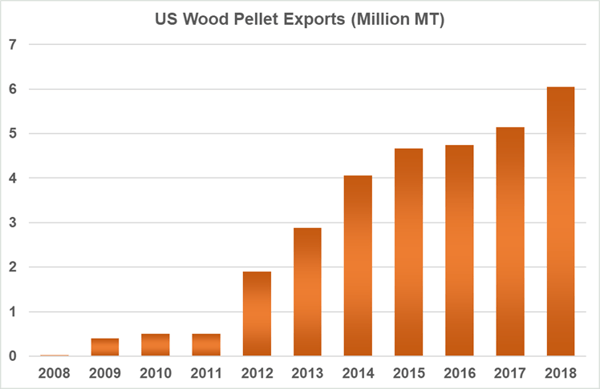

This new demand—driven by a consumer preference for more renewable energy and by European Union (EU) subsidies to support a renewable transition—has facilitated the development of large-scale wood pellet export mills in the US. UK-based companies, for instance, either offer US producers secure long-term contracts, or they purchase facilities in the US, vertically integrating into the region. Without the industrial wood pellets produced in the US, large scale coal-to-biomass conversions would have been impossible. Over the last ten years, wood pellet exports from the US have increased from less than 30,000 tons in 2008 to over 5 million tons in 2017.

US wood pellet exports to Europe are starting to slow after growing at a rapid 63% compound annual growth rate (CAGR) from 2011 to 2014; pellet export growth has slowed to 6.4% CAGR from 2014-2017. New demand flattened in 2017 and minimal EU growth is forecast in the near term, but bourgeoning biomass and wood pellet opportunities exist throughout Asia. From 2012 to 2017, wood pellet imports to Japan and Korea increased from less than 200,000 tons to nearly 3 million tons. Expectations for future demand in Asia are between 10 - 20 million tons within the next 10 years.

Southern landowners are getting better each year at increasing production and cash flow, and we will likely continue to see planting density increase and the rotation age shorten. On a Southwide basis, excess inventory will likely limit an upside price correction for the foreseeable future; the days of mid-$40/ton stumpage for sawtimber and mid-$20/ton for CNS are likely gone for now. However, there are local pockets where current stumpage prices for large sawtimber are in the range of $40/ton, and there will continue to be areas of intense competition that drive prices upward in certain procurement zones.

Despite the volatile softwood lumber market, competition for wood fiber in the US South is being redefined by strong demand for pine pulpwood, changing market preferences and an evolving forest products industry. As weighted softwood prices continue to increase gradually across the South, demand for (and access to) pulpwood will be leading the rebound for the foreseeable future. With abundant resources, class-leading low costs and the capabilities to manufacture and market a variety of wood products, the US South will remain the preferred destination for forest products investment and opportunities.