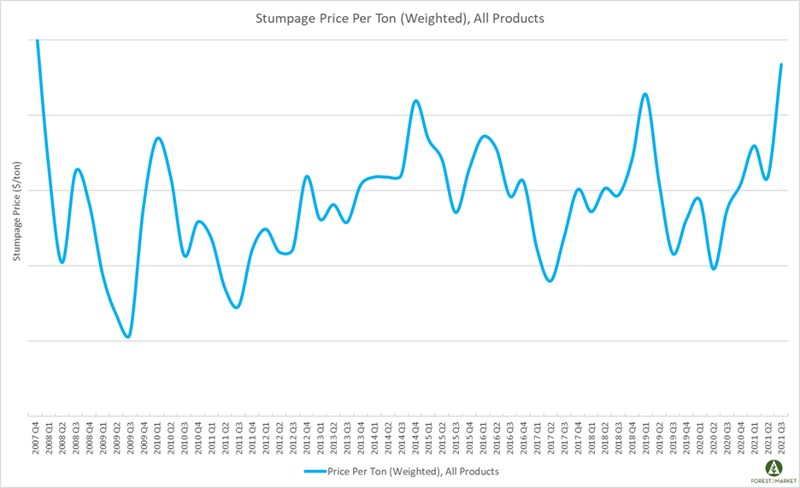

Led by insatiable demand for small pine and hardwood logs, the weighted average price for southern timber surged to a 14-year high in 3Q2021. Stumpage prices were up +16 percent quarter-over-quarter (QoQ) and +22 percent year-over-year (YoY). The last time Forest2Market’s Southwide weighted average stumpage price was this high was in 4Q2007, just before the onset of the Great Recession.

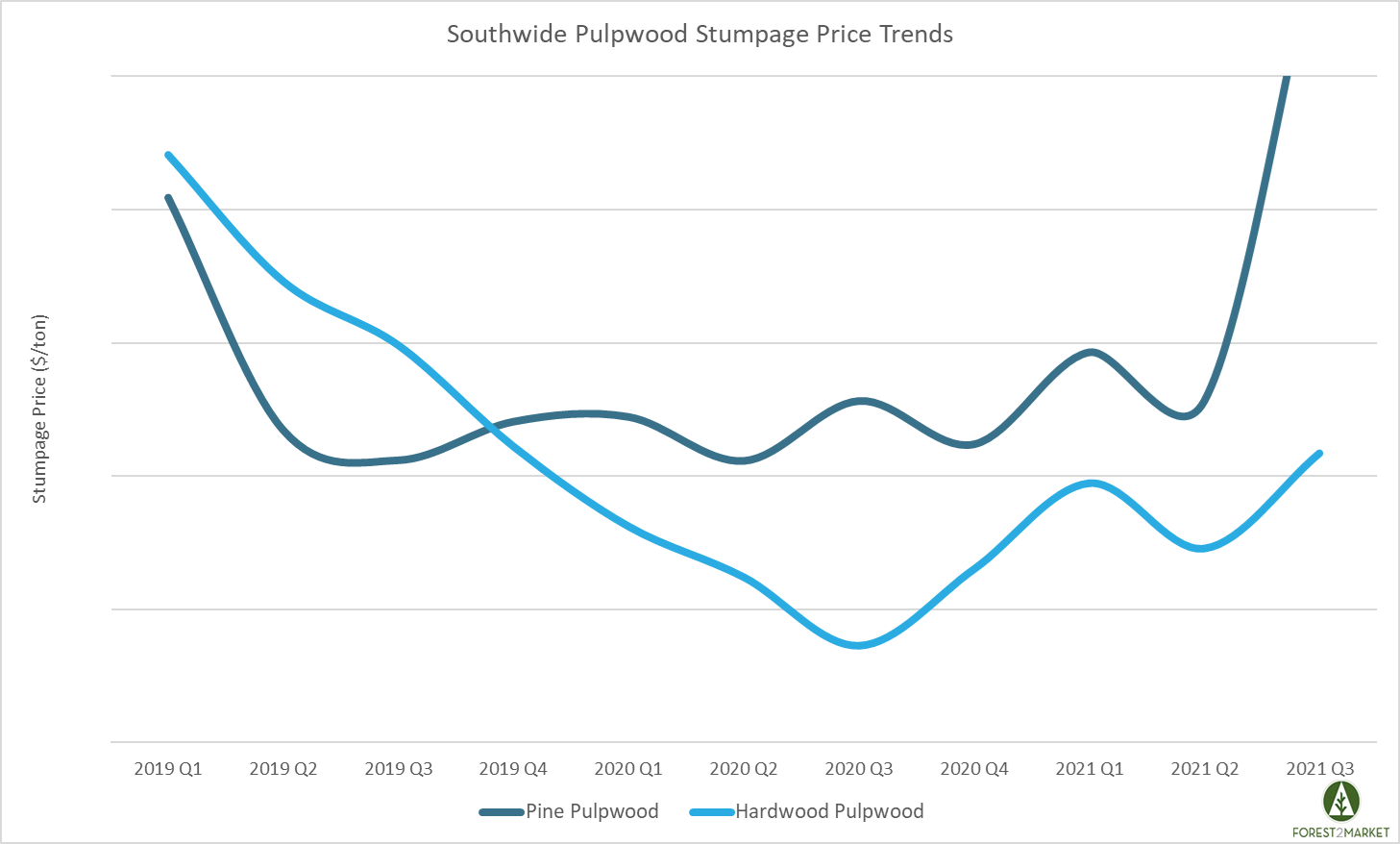

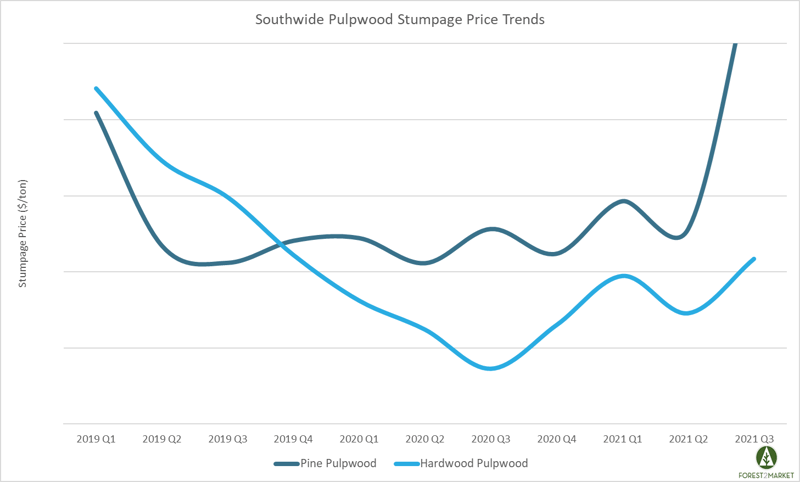

Pulpwood

On a Southwide basis in 3Q2021, pine pulpwood prices skyrocketed by an astounding +78 percent QoQ and YoY, as two of the three regions saw significant price increases for this product. Prices in the East-South surged +65 percent while prices in the Mid-South jumped +68 percent QoQ. However, prices in the West-South inched down -2 percent.

Though less severe, hardwood pulpwood demand was also strong in all three regions in 3Q; Southwide prices were up +21 percent QoQ and +55 percent YoY. Prices in the East-South were up +16 percent, +29 percent in the Mid-South, and +8 percent in the West-South QoQ.

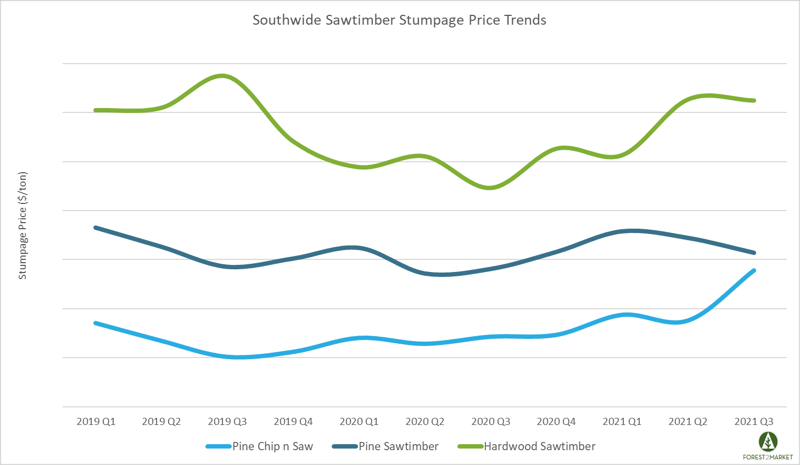

Sawtimber & Chip-n-Saw

On a Southwide basis, pine chip-n-saw (CNS) prices jumped +26 percent QoQ and +37 percent YoY; just like pulpwood products, the East- and Mid-South regions saw significant demand for this product. Prices in the East-South were up +9 percent, while prices in the Mid-South surged +33 percent QoQ. However, prices in the West-South were down -10 percent.

Pine sawtimber prices were down -5 percent QoQ, but prices were up +7 percent YoY on a Southwide basis. Prices in the East-South were up +4 percent; however, prices in the Mid-South were down -4 percent and prices in the West-South decreased -10 percent QoQ.

After experiencing an uptick in 2Q2021, Southwide hardwood sawtimber prices were largely flat in 3Q as they inched down just -0.3 percent. Prices in the East-South were down -10 percent, but prices in the Mid-South were up +9 percent and +15 percent in the West-South.

Outlook

Total precipitation across the South was up over +20 percent in 3Q, which impacted harvesting operations and drove competition (and stumpage) prices higher in many areas. In these conditions, pine pulpwood oftentimes becomes inaccessible, which is reflected in high market prices. As we recently noted, the south Georgia/north Florida wood basket was one such region in 3Q, where a combination of factors — including wet weather and intense demand — pushed pine pulpwood prices +71% and CNS prices +41% QoQ.

Though finished lumber prices are down over -55 percent from a record high achieved in May, lumber demand was insatiable in 1H2021. Per Forest2Market’s southern yellow pine (SYP) lumber price composite, prices fluctuated between $900/MBF and $1,200/MBF during 1Q and 2Q2021 — significantly higher than the historical floor price of roughly $350/MBF. While this demand didn’t materially impact sawtimber prices in 3Q, it is evident in the CNS price surge of +26 percent QoQ. Chasing record high margins, small log lumber mills throughout the South have had more flexibility to fiercely compete with other CNS consumers.

While the southern timber market has been oversupplied for a decade, stumpage prices across the South have now hit a new 14-year high as they continue to climb out of the COVID-induced hole experienced during much of 2020. Is this a temporary reaction, or a sign of things to come?

Southern timber prices are now higher than they have been in 14 years, and more price volatility is likely in the coming months. If you are not a subscriber to our Stumpage 360 database, now is the time to stay ahead of your local market with the power of transactional data.