Joe Clark

Joe Clark

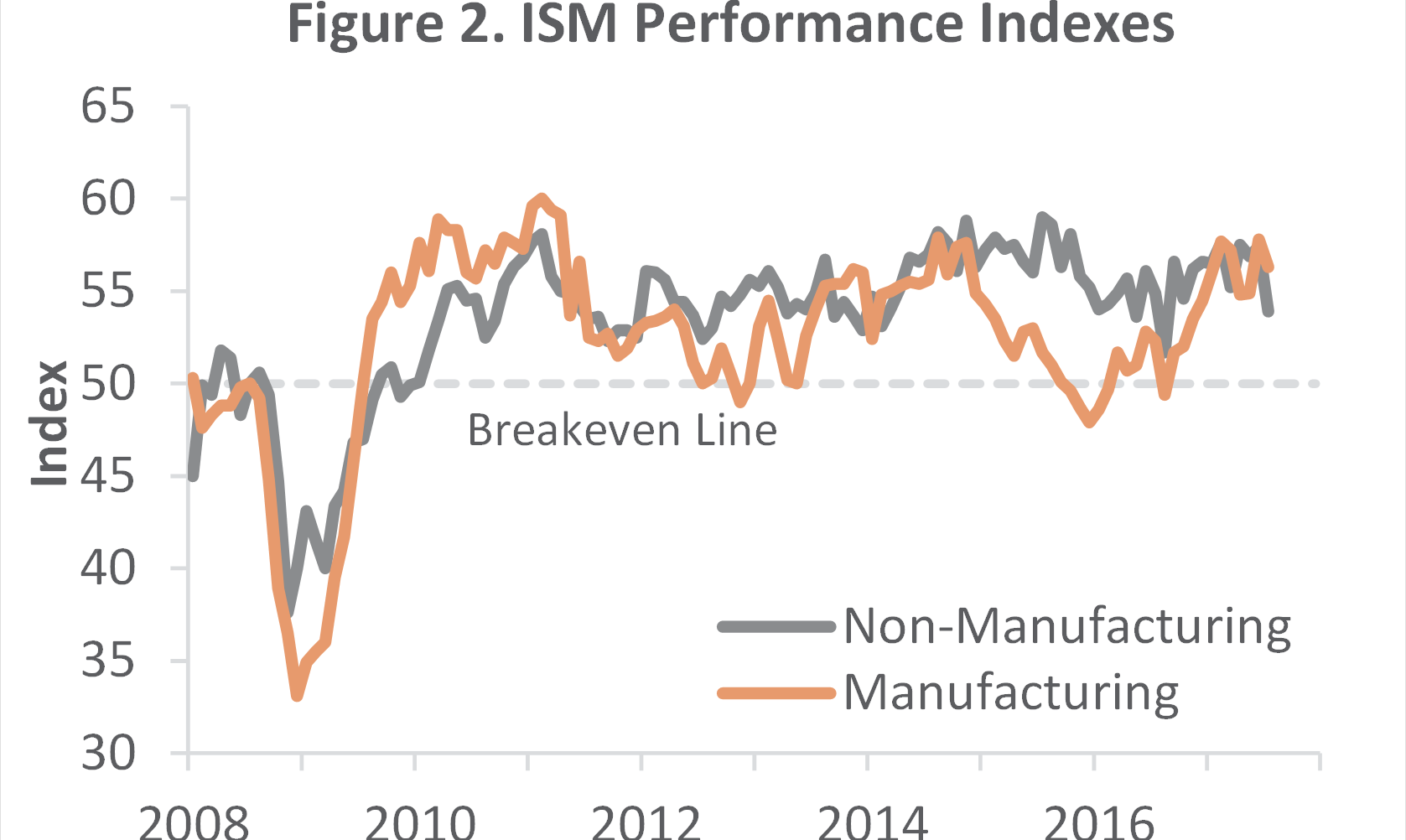

US forest industry performance in June and July was recently reported by both the US government and the Institute for Supply Management.

Total industrial production (IP) rose 0.4 percent in June for its fifth consecutive monthly increase. Manufacturing IP moved up 0.2 percent, but because factory output has vacillated in recent months, its level in June was little different from February.

The Institute for Supply Management’s (ISM) monthly survey showed the sentiment of US manufacturing softening in July. The PMI registered 56.3 percent, down 1.5 percentage points (PP) from June. (50 percent is the breakpoint between contraction and expansion.) Index/sub-index values were generally lower in July—the most notable exception being input prices.

The pace of growth in the non-manufacturing sector decelerated more abruptly (-3.5 PP), to 53.9 percent. As with manufacturing, prices paid bucked the general trend of lower service index/sub-index values. Of the industries we track, only Ag & Forestry contracted. As an aside, softwood lumber exports were indeed higher in June (+17.7 percent MoM; +1.7 percent YTD), while imports slowed (-5.9 percent MoM; -11.8 percent YTD); interestingly, imports from Canada are off 14.4 percent YTD. Of note, Mobile, AL was the second most-active export district in June (19.0 percent of US total); also, southern pine represented 36.1 percent of all softwood exports (+4.2 percent YTD).

The producer price index (PPI) increased 0.1 percent in June (+2.0 percent YoY). As was the case a couple of months ago, almost 80 percent of the MoM rise can be tracked to final-demand services, especially firms in the “securities brokerage, dealing, investment advice, and related services” sector—which is facing higher costs as a result of the Department of Labor’s Fiduciary Rule.

Forest products PPIs were mixed:

- Pulp, Paper & Allied Products: +0.7 percent (+3.3 percent YoY)

- Lumber & Wood Products: -0.2 percent (+2.9 percent YoY)

- Softwood Lumber: -3.0 percent (+9.7 percent YoY)

- Wood Fiber: +0.7 percent (-0.7 percent YoY)