Daniel Stuber

Daniel Stuber

A little over a year ago, we published a white paper on the future implications of inventory trends we were seeing take shape. Now that the US Forest Service’s Forest Inventory and Analysis (FIA) dataset is nearly complete for survey year 2014 (Louisiana and Virginia are still outstanding), Forest2Market has pulled the 2014 data, projected datasets for Louisiana and Virginia and updated timber inventory and age/class distribution trends for the US South.

Inventories

Pine Sawtimber

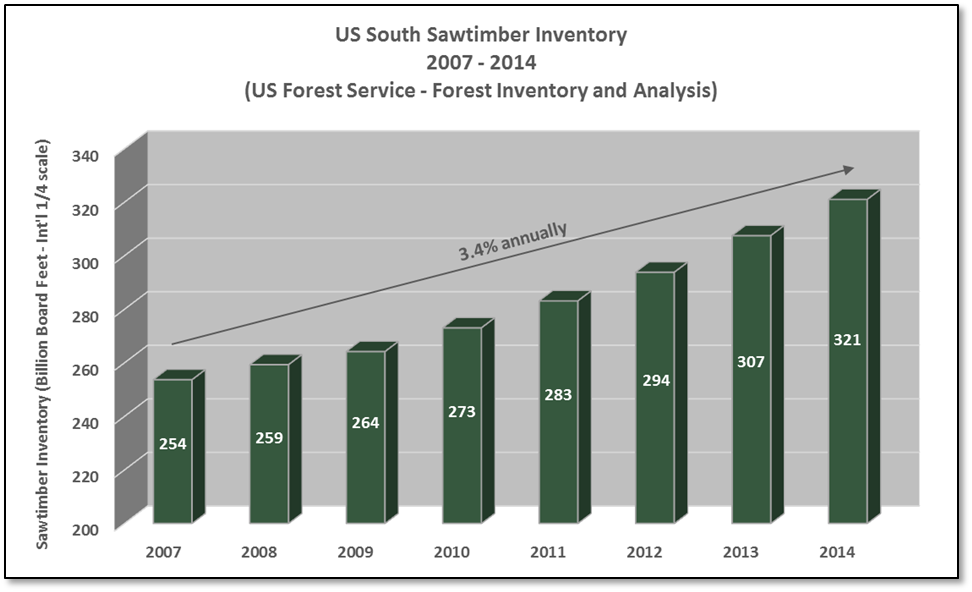

Numbers updated for 2014 continued to show a build-up of sawtimber supply and, based on the 2014 measurement cycle, pine sawtimber inventory increased to 321 billion board feet. This reflects a 4.4 percent increase over the 2013 measurement and a 26.5 percent increase since 2007 (3.4 percent annually). As observed in the chart below, the trend is accelerating; in our last report (based on 2013 data), the annual timeframe increase was 3.2 percent.

Pine Pulpwood

FIA data also reported an increase in pulpwood inventories. In 2014, pulpwood inventory measured 27.3 billion cubic feet, an increase of 1.0 percent from 2013. Since 2007, pulpwood inventories have increased 9.3 percent (1.3 percent annually). However, unlike sawtimber, the trend appears to be tapering off; the 1.3 percent annual increase from 2007 (based on 2014) was 1.4 percent in our last report (based on 2013).

Age Class Distribution

As the two charts below illustrate, the US South continued to lose both inventories and acres of younger pine through 2014. Trend patterns within the 0-10 and 11-20 age classes continued to decline, while the 21-40 age class demonstrated a steady increase.

At the acre level, the distribution for the 0-10 age class has declined from 20.3 percent in 2007 to 17.6 percent in 2014, a change of 13.2 percent (2.0 percent annually). For the 21-40 age class, the distribution of acres has increased from 23.9 percent in 2007 to 26.4 percent in 2014, a change of 10.6 percent (1.5 percent annually).

Future Implications

Future Implications

With the increase in available pine sawtimber and continued demand for younger timber in the market during the period from 2007-2014, the data confirm that there is currently more sawtimber available on the stump throughout the US South as inventories and acres continue to increase. Stumpage prices have remained relatively flat since 2009 even though lumber production has increased by 5.7 percent annually. We expect sawtimber prices to continue to inch higher in the near term.

Demand for pulpwood has slightly outpaced age/class and acreage distribution for younger timber, and prices have responded. As pulpwood supply continues to be constrained and with potential demand increasing, one has to wonder how long it will be before pulpwood price levels reach a point that the market reacts adversely. Combining this rising price scenario with the strengthening dollar could have negative implications for the immediate future. As we stated last year, the key for both buyers and sellers will be identifying future markets now and preparing to shift and optimize their sales/production to these opportunistic markets.