Daniel Stuber

Daniel Stuber

Forest2Market’s mission has always been to empower its participants to make exponentially better decisions through the application of industry expertise and unique datasets. We believe that market price transparency and transaction-based benchmarking are vital to optimizing and stabilizing the supply chain between producers and consumers. Demand and capital will always flow to the lowest cost producer, and with wood fiber being the largest variable cost input for the pulping process, it is imperative for producers in various regions to know their wood fiber price positions in the global market.

Forest2Market is on the cusp of producing its first wood fiber delivered price benchmark for the Baltic Rim.* As market penetration builds, we will develop a global wood fiber benchmark covering major market regions and various end products. The following data represents a portion of this metric, the new Western Hemisphere Benchmark.

*Denmark, Estonia, Finland, Germany, Latvia, Lithuania, Poland, Russia and Sweden

Benchmark Methodology

For the Western Hemisphere Benchmark, we report stemwood (i.e. tree-length pulpwood or bolts) and wood fiber chips (wood fiber chips only, not energy chips) delivered through the supply chain to the end producer’s mill gate. We then convert the price and unit of measurement to US dollars/short ton. For stemwood, we also convert the product to a wood fiber chip equivalent and add a cost of five US dollars/green ton for debarking and chipping to the chip pile. We then compute a weighted average price for all combined wood fiber.

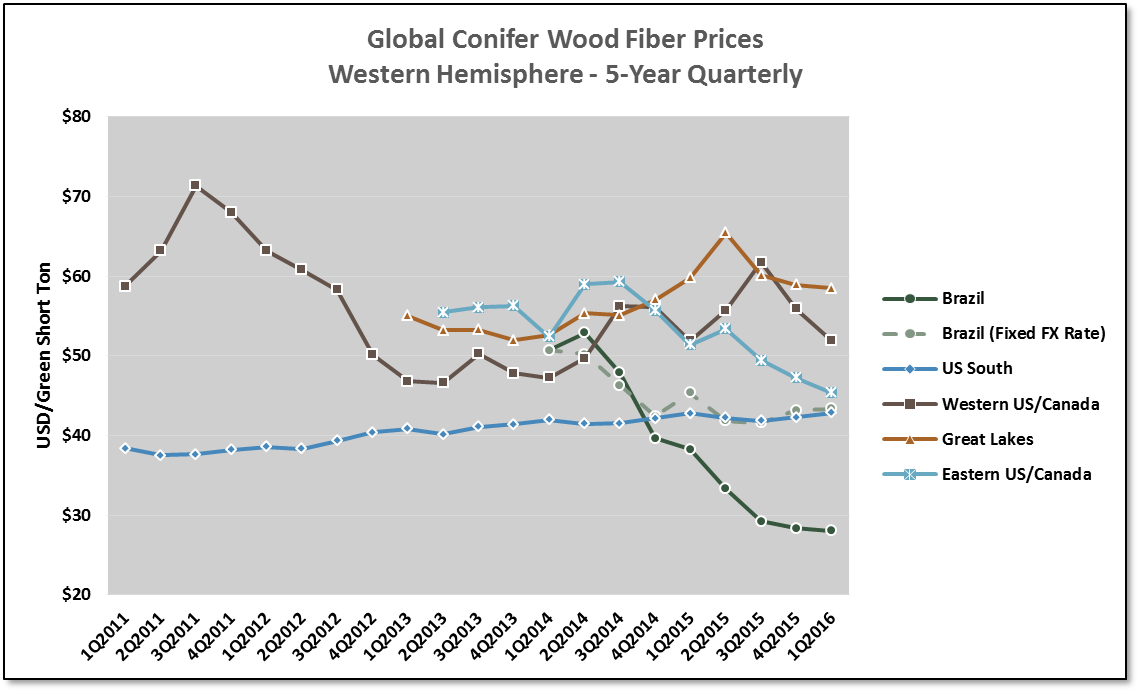

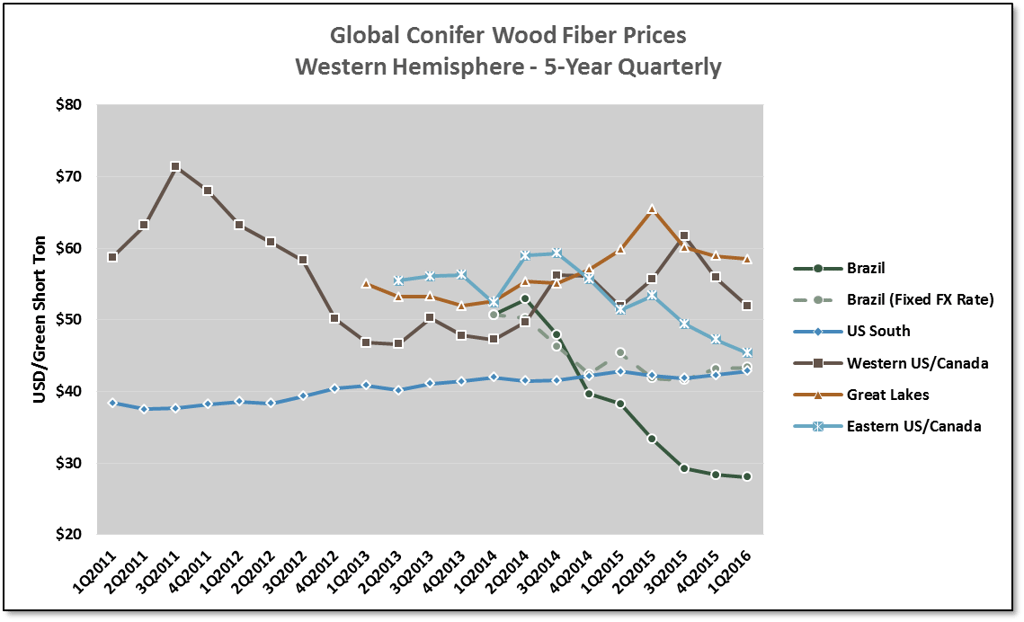

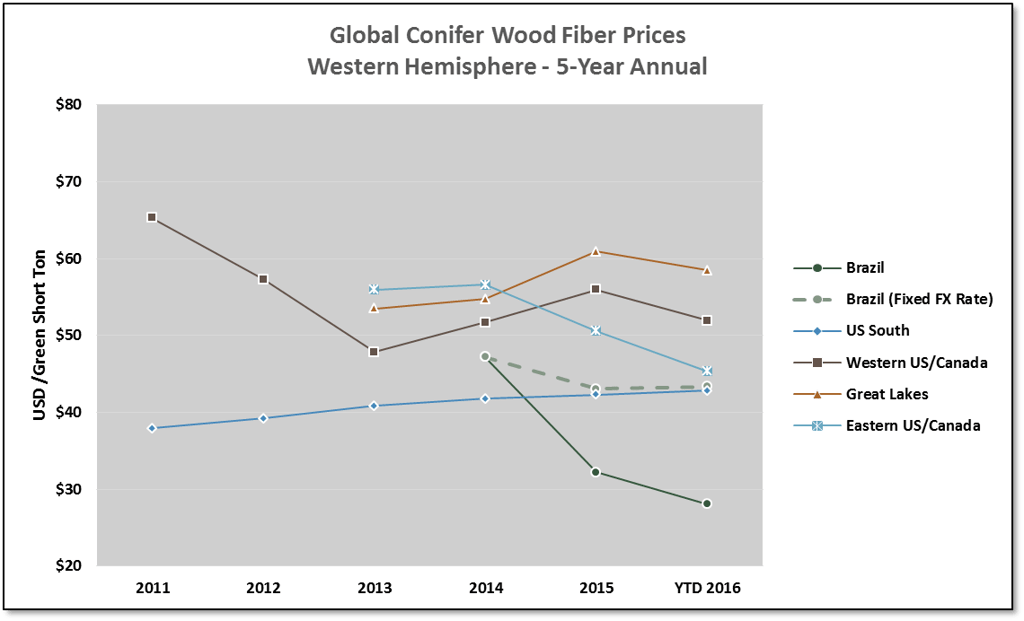

Conifer Wood Fiber

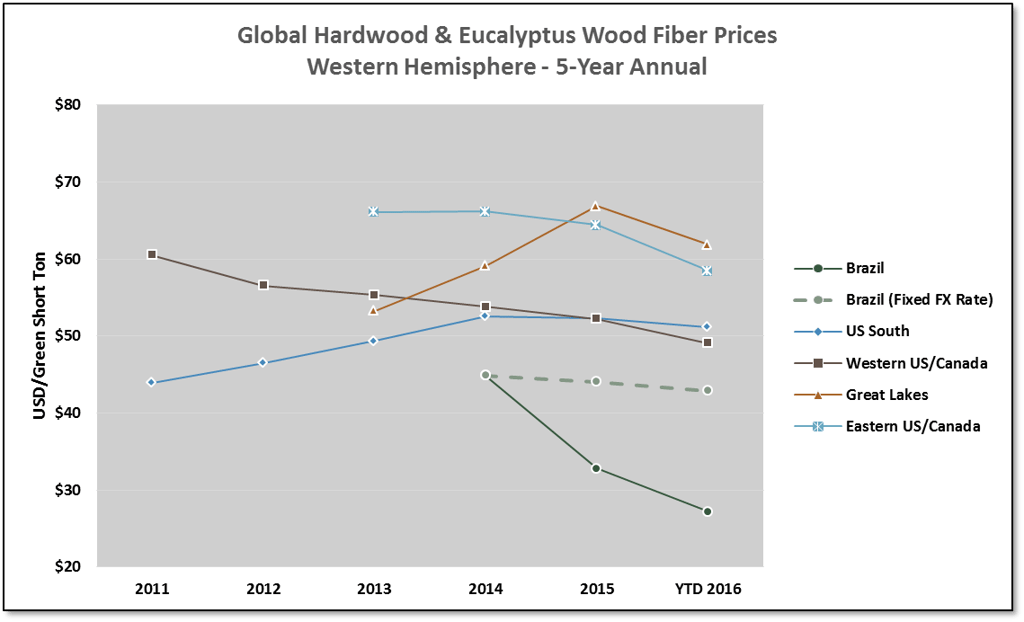

Due to current economic and political instability, as well as the strength of the US dollar (USD), conifer wood fiber in Brazil is the lowest-cost wood fiber when compared to US and Canadian markets ($28.04/ton vs. $49.63/ton North American average in 1Q2016). In 2Q2014, Brazilian conifer was trading at a point between major US and Canadian markets. Over the course of the last two years, however, prices have plummeted 45 percent primarily, the result of a 65 percent depreciation in the Brazilian Real against the USD. When holding the exchange rate constant to the 2Q2014 rate (i.e. on a Fixed FX Rate), conifer prices in Brazil tend to be on par with those in the US South ($43.35/ton vs. $42.82/ton in 1Q2016). The difference of $15.31/ton is due entirely to the exchange rate effect. In response to poor in-country markets, several Brazilian producers are making necessary changes in their management strategies in order to take advantage of export opportunities. Because the US is one of the potential export markets these producers are looking at, this will create more competition in the US market.

The most stable market for conifer fiber in the regions where we collect data is the US South. The lack of volatility in price averages in this region is largely due to the scale of the region itself; its market size dwarfs the other regions by an average factor of almost 25 times. (Individual markets within the region would demonstrate slightly more volatility.) Even with the advantages of scale, conifer wood fiber prices continue to increase in the US South. The stability and low cost of this fiber continue to attract demand, particularly for the growing containerboard and specialty pulp production sectors (e.g. dissolving pulp, fluff, rayon, etc.).

Also during this timeframe, the Eastern US/Canada conifer benchmark has traded downward, almost on par with US South prices. While the market is significantly smaller in scale and the Canadian/US dollar exchange rate is a nuance in the data itself, mill closures in the region and reduced demand have taken a toll. Since reaching a peak of $59.28/ton in 4Q2015, prices have since declined 24 percent to $45.33/ton in 1Q2016.

In the Great Lakes region, conifer prices appear to be stabilizing since reaching a high of $65.43/ton in 2Q2015 when a surge in intermediary woodyard transfers occurred as a consequence of mill inventories falling out of shape. This circumstance, combined with land ownership transfers, summer logging restrictions and a shortage of surge logging capacity, caused prices to escalate 26 percent from a low of $51.97/ton in 4Q2013. Since 2Q2015, the market has adjusted, falling to $58.46/ton in 1Q2016.

In the Western US/Canada region, the return of sawmill production during 2012, 2013 and 2014 was a welcomed relief to fiber buyers. During this timeframe, fiber buyers were able to reduce their purchases of chipmill stemwood chips and long-haul sawmill residual chips, and purchase more local sawmill residual chip supplies. After reaching a high of $71.32/ton in 3Q2011, total conifer fiber prices declined 35 percent to a low of $46.62/ton in 2Q2013 and held at this level until 2Q2014. Since this point, prices have been volatile and have steadily trended upward as US sawmills have reduced production to compensate for increased British Columbia sawmill production. US sawmills have also had to balance production with higher-priced and tight log availability due to competition from export markets. After a 3Q seasonal spike in 2015, prices began declining to their 1Q2016 average of $51.91/ton.

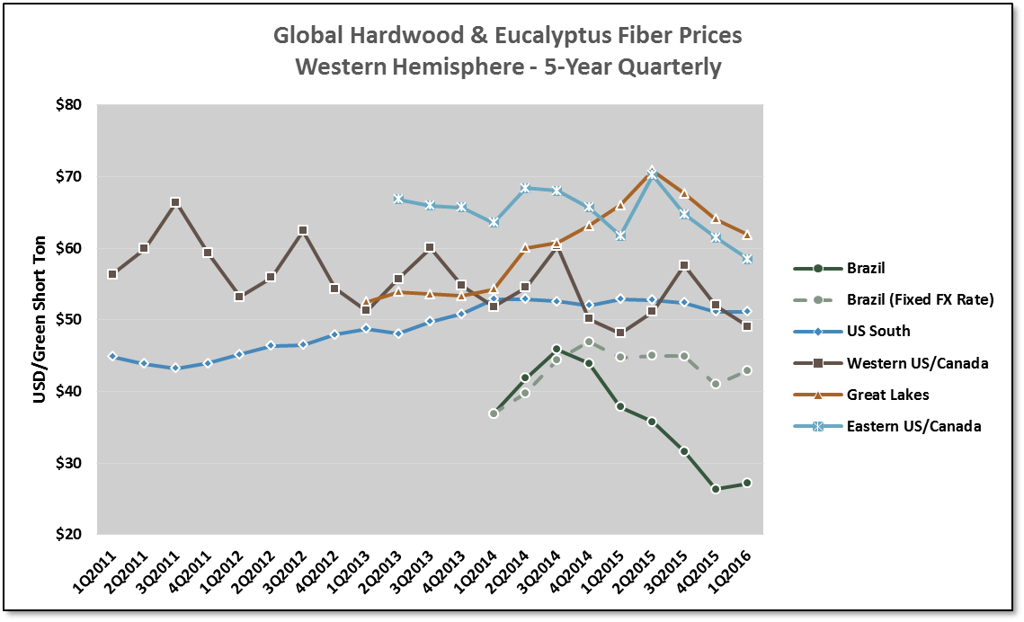

Hardwood and Eucalyptus Wood Fiber

As expected, hardwood price trends for the Great Lakes and Eastern US/Canada resemble conifer wood fiber trends, but at different price levels. It should be noted that these regional prices peaked near each other in 2Q2015: $70.25/ton in the Eastern US/Canada region and $70.86/ton in the Great Lakes region. However, since this time, declining demand for conifer in the Northeast US has caused hardwood fiber prices to decline at a faster rate than in the Great Lakes (-17 percent vs. -13 percent). Prices in the Eastern US/Canada benchmarked at $58.47/ton in 1Q2016, while Great Lakes prices benchmarked at $61.85/ton.

The Western US/Canada hardwood fiber market is a small market, roughly 10 percent the size of its conifer market. Prices experience seasonal volatility, typically peaking during the third quarter. Overall, prices have continued to trend downward as demand has declined, averaging $49.07/ton in 1Q2016.

In the US South—a region where demand for hardwood fiber has declined—prices have trended upward as available pulpwood supply has declined, a result of inventory growing into larger sawtimber diameters and less conifer clearcutting reducing come-along, residual hardwood pulpwood, and periods of excessive rainfall disrupting the supply chain. From a low of $43.20/ton in 3Q2011, delivered prices increased 22 percent to a high of $52.92/ton in 1Q2014. Since this time, however, prices have leveled off, moderating to $51.15/ton in 1Q2016.

As with conifer, Brazil’s fast-growing eucalyptus is the lowest cost wood fiber when compared to hardwood markets in North America. However, when the exchange rate is held constant, eucalyptus still maintains its low cost advantage. When removing the exchange rate effect ($15.75/ton in 1Q2016), prices were fairly level from 3Q2014 to 3Q2015, averaging roughly $45.00/ton. In 4Q2015, prices experienced a $4.00/ton correction, though the correction was short-lived, as prices increased to $42.90/ton in 1Q2016. As with conifer, the low cost on a dollar basis will provide opportunity for market pulp consumers who are able to substitute white pulp made from eucalyptus as an alternative to hardwood.

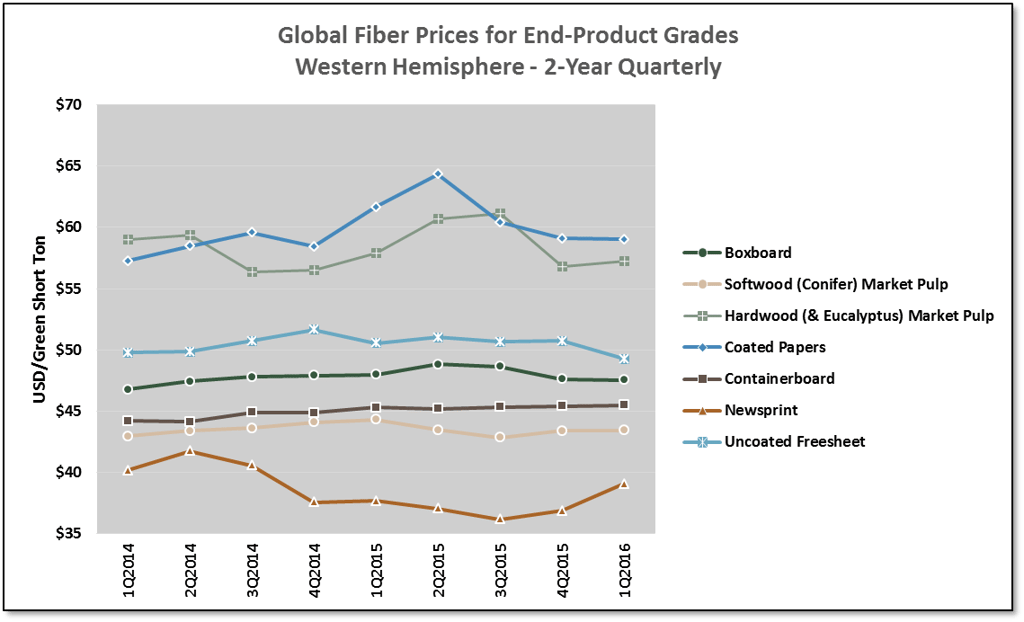

Delivered Wood Fiber Prices for End-Product Grades

An additional benefit of being able to accurately report benchmark wood fiber costs for various species and grades is the establishment of a global wood fiber benchmark for various end-products. Below are quarterly trends for these various segments based on our western hemisphere data.

We believe the Western Hemisphere Benchmark is a valuable tool providing unparalleled insights into the global wood fiber supply chain. Expanding into eastern hemisphere markets will allow us to provide a more complete global view. To learn more about our Western Hemisphere and regional benchmarks, or to subscribe, contact us.