Pete Stewart

Pete Stewart

The US housing sector—a bellwether for economic health—has showed signs of stagnation (and even the prospect of reaching peak housing in this market cycle) in recent months. As I wrote last month, forecasts for housing starts are simply overblown, as there isn't much room for an increase beyond the 2018 level of 1.266 million units.

As a commodity largely tied to housing starts and broader building and construction activity, lumber prices also reflect the general health of this market via supply and demand metrics. After steady increases beginning in 4Q2017, lumber prices skyrocketed to new record highs in 2Q2018 before dropping precipitously across the board over the last four months. Southern yellow pine (SYP) lumber prices recently hit their lowest point since August 2017; Forest2Market’s SYP composite index price for mid-November was $376/MBF—a 35% drop from the record high of $576/MBF achieved in May.

Despite the one–two hurricane punch that recently impacted the US South and the continued wildfires in the Pacific Northwest (PNW)—extreme weather events that have significantly impacted forest inventories, harvests and supply—the drop in lumber prices over the last six months is largely, though not entirely, demand driven. Fewer new-home builds = less lumber.

The sudden reversal begs a serious question: Did the lumber market simply over drive its headlights in the price run-up earlier this year, or are there more structural forces at work? Several dynamics are combining to impact housing starts and, by extension, the North American lumber market.

Supply Analysis

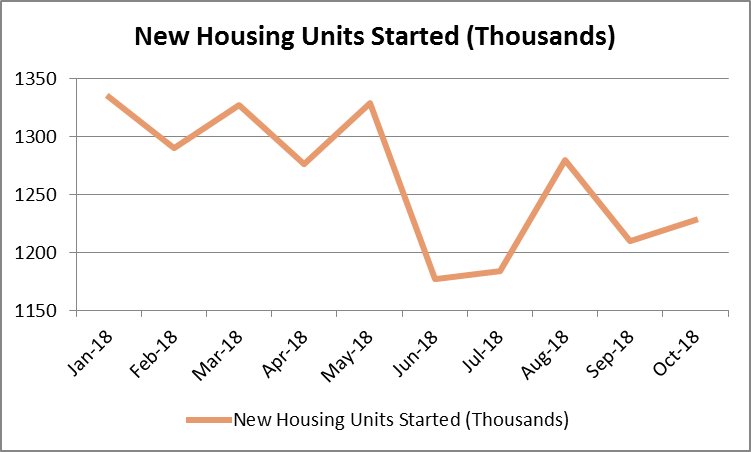

Housing starts kicked off 2018 with a bang, leading many to believe that there would be a gap in supply once the busy part of the building season hit. January starts were up 9.7 percent over December 2017 to a seasonally adjusted annual rate (SAAR) of 1.326 million units, and speculation began to drive lumber prices ever higher.

But as the meat of the building season came and went and housing starts failed to live up to expectations (now on pace at a SAAR of 1.228 million units), lumber production numbers confirm that any supply concerns were exaggerated. Both US softwood lumber production and total softwood imports have increased year-over-year (YoY). Through August 2018, US production was 23.8 BBF (+4.8%) and total imports were 10.3 BBF (+1.3%). Despite the tariffs on Canadian product, imports from Canada were only off 1.4% YoY to 9.3 BBF through August. Latin America (primarily Brazil) and European producers more than made up for the difference in Canadian volume; LatAm shipments to the US totaled 306 MBF (+8.3%) while European shipments totaled 589 MBF (+65%) through August.

We may see this trend reverse course when full 3Q and 4Q trade statistics are reported; however, those numbers will be immaterial to this analysis. The data show that domestic and import supply was ample through the price run-up that began in 1Q2018 and peaked in 2Q. Neither US production nor imports through August suggest any supply-side disruptions that would account for such a dramatic surge in price.

Decreasing Demand for Homes

“Housing is no longer a tail wind for the economy, but [so far] the headwinds are blowing very gently,” wrote Michelle Meyer, a Bank of America Merrill Lynch economist, in October. One sign of a shifting housing market is slowing demand—including buyer traffic—for existing homes. Resales earlier this fall suffered the largest drop in 2½ years to the slowest pace since November 2015. Though still high, resale price appreciation has been decelerating (below +6% YoY for the first time in 12 months) and the supply of existing homes, while still low, is gradually expanding; there were 4.4 months of supply in September, up from the year-earlier 4.2 months.

Based on the behavior of the exchange-traded fund iShares US Home Construction (ITB), which tracks a basket of 47 US homebuilders and construction-related companies, investors apparently agree with Meyer’s sentiment. As of mid-November, ITB’s share price had fallen over 34% from its mid-January peak. Builders are in a tough spot, as they have been hit with a number of challenges this year including an increase in materials costs, land and labor shortages and a shrinking appetite of prospective buyers who are willing pay up.

Real private residential investment (PRI) declined for a third quarter in 2Q2018; as a percentage of total GDP, the decline has been in place since 1Q2017. Although both metrics have receded only modestly from their corresponding recent peaks, they nonetheless paint a potentially disconcerting picture for the sustainability of this market cycle.

Increasing Inventory of Homes

Interestingly, especially since there is a general consensus that more new-home supply is needed, rising inventory is even more pronounced in newly-built homes. After meandering around an average of 5.3 months between July 2013 and December 2017, new-home inventory has trended higher in 2018 (to September’s 7.1 months of supply). In addition, the ratio between starts and new-home sales reached 1.5 in September, which is in the top 14% of monthly ratios since January 1995. The implication is that unless the pace of new-home sales picks up, starts will ultimately be forced lower.

With long-term Treasury yields helping to push mortgage rates upward, the median new-home prices less than 7% off November 2017’s record high, and resale appreciation only gradually slowing, it is entirely possible that housing demand could weaken further in coming months. Despite sustained high home prices (and surging prices in some markets) some regions are now drifting into the “buyer’s market” column.

Interest Rates

With home appreciation and mortgage rates trending higher, the reality is that many potential borrowers simply can’t make the mortgage numbers work. One way to measure the impact of inflation, mortgage rates and home prices on affordability over time is to use CoreLogic’s “typical mortgage payment,” which is a mortgage-rate-adjusted monthly payment based on each month’s US median home sale price. The number is calculated using Freddie Mac’s average 30-year fixed-rate mortgage rate with a 20% down payment, and it doesn’t include taxes or insurance. As such, the typical mortgage payment is a good measure of affordability because it shows the monthly amount that a borrower needs to purchase a median-priced US home.

The US median home sale price in August 2018 ($226,155) was up 5.7% YoY, while the typical mortgage payment was up 14.5% YoY due to a nearly 0.7-percentage-point rise in mortgage rates over that period. Tight housing inventories coupled with rising home costs are a real barrier for potential homebuyers, but a typical mortgage payment that is rising at over twice that pace is a much more serious concern, and a number of forecasts call for even higher rates next year.

Moody’s Investors Service has observed the deteriorating quality in mortgage loans noting that “The broad conditions under which loans are being granted have grown less favorable for future mortgage performance. For instance, home prices are no longer very affordable and rising interest rates are reducing refinancing incentives and prepayments.” Hence, “mortgages being originated today appear more likely to face a stressed environment within only a few years, [compared to] loans originated earlier during this long period of economic growth.”

And that’s just mortgage rates, which function independently of the federal funds rate instituted by the Federal Reserve (Fed). Though speculative at this point, the Fed is expected to raise interest rates once more this year and, potentially, three to four times next year, which will impact short-term and variable (adjustable) interest rates. Strategists warn that if the Fed tightens too much, economic growth could slump and trade wars could intensify, destroy demand and negatively impact earnings.

The potential scenarios in the wake of these rate hikes are many. However, the impacts of continued increases would most certainly discourage any expansion in new homeownership that would drive an increase in housing starts and additional demand for lumber.

Home Size

Not only have housing starts been decelerating since 2013, but home size has also been shrinking. Median floor area of new single-family completions peaked at 2,647 square feet (SF) in 2015 and has subsequently been declining on trend (to 2,426 SF in 2017). The median new home cost a record $133/SF in 2017, +30% relative to 2010. Apartments, by contrast, have been gradually expanding (2017 median: 1,096 SF) from 2013’s 1,059 SF. If these trends continue, net changes in demand for lumber and other building materials could well be negative. While the trend of slightly-shrinking single-family home sizes may seem minimal, the cumulative impact of fewer builds using less lumber is resulting in diminished demand.

How Are Mills Reacting?

The tense trade situation with China has impacted regional log prices in both the PNW and the US South in recent months. On an annualized basis, shipments of Douglas fir logs out of the PNW are slightly down and averaging $221 per cubic meter (m3)—up 14% YoY; conversely, shipments of SYP logs out of the South are up 89% while the price has dropped to $141/m3—down 13% YoY.

Volume & Price of Select Log Exports (5 Years) [1]

Domestic and export competition for logs in the PNW earlier this year drove prices to sustained highs. After watching the steady rise in prices since 4Q2017, regional lumber mills maxed out their log purchases in order to maintain inventories and beat what seemed to be a never-ending price run. But as trade disputes materialized, exports waned and the housing market sputtered, demand for logs cooled and prices have decreased as a result—much to the chagrin of many regional sawmills, who still have full log inventories that were purchased at peak prices earlier in the season. The decrease in lumber demand has driven many regional mills to reduce production; some are cutting operating hours or curtailing shifts, and others are temporarily curtailing production altogether until markets improve.

It’s been “business as usual” for mills in the US South, though, who have maintained production levels through the unstable rise and fall of lumber prices. However, these facilities have a much higher degree of flexibility than do those in the PNW. Most notably, their log yard exposure is significantly diminished because there has been very little volatility in SYP log costs, which have remained low in the wake of the Great Recession of 2008.

The Verdict

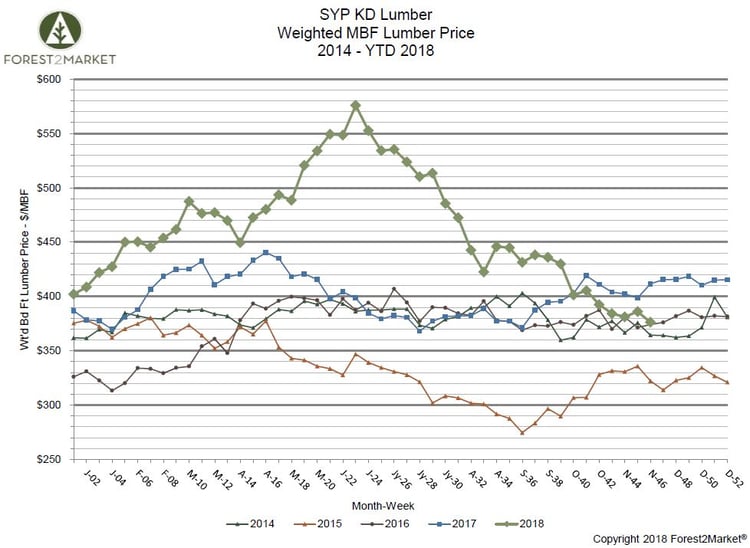

Did lumber prices really crash in 2018? Not if we take an historical view using Forest2Market’s SYP price data in the chart below. In fact, we should be asking the inverse question: Why did lumber prices spike to historical highs?

It is clear that the irregular peak that occurred from May-August was an anomaly likely driven by speculation around uncertain trade policies, overly optimistic housing start numbers and the likelihood of pinched lumber flows from Canada and the timber-constrained PNW. Yet, none of these events materialized either disproportionately or collectively to a degree that would drive prices to new highs. Remove the May-August variance, control for a more historical trend and 2018 lumber prices are really in line with historical norms and current demand.

While some of the market influences currently affecting lumber prices seem to be embedded at the structural level (trade disputes, tariffs, etc.), a cyclical decrease in demand is driving what only appears to be an extreme correction in price. This price change represents a natural return to equilibrium as market speculation has waned.

As we well know, the US housing market is cyclical—if fickle—by nature, and any commodity that is dependent on such a market will therefore experience volatility related to its cycles. To meet the modest forecasted increase in demand in the near term, there will be an estimated 6 BBF of capacity coming online by the end of 2020 via combined greenfield mill expansions and newly-rebuilt/refurbished facilities in the US South. Lower manufacturing costs in new and upgraded mills will allow producers to efficiently manufacture SYP lumber through any market valleys or anomalies in the future. As CLT and other new mass timber building products continue to gain market share, this trend will add to underlying demand for solid wood products, which will benefit producers in both the US South and the PNW.

[1] Prices are US dollars per cubic meter and are the Free Alongside Ship value at the port of export. It includes the transaction price, freight, insurance and any other charges in placing the logs alongside the carrier at the port of export. It excludes any cost of loading aboard the carrier, insurance and transportation beyond the port of export.