Joe Clark

Joe Clark

The Georgia/Florida region has long been a vibrant timber market in the US South, and it is home to a diverse group of long-standing manufacturing facilities in the area. It’s also a market that has undergone some significant changes over the last several years due to new market entrants, weather events, changes in economic conditions and shifts in timber demand.

In 2013, Austria-based Klausner announced the construction of its new Lumber One mill in Live Oak, FL, which brought an additional 300 million board feet (MMBF) of lumber capacity to the area. While the facility offered a lot of long-term promise for timberland owners and suppliers, it ultimately ran intermittently since opening and never performed at full capacity.

In mid-March, Klausner abruptly shuttered operations altogether at the Lumber One facility and is now seeking Chapter 11 protection with more than $100 million in debt.

Now, a confluence of three events is poised to have some significant, long-term impacts on the regional timber market.

Event #1

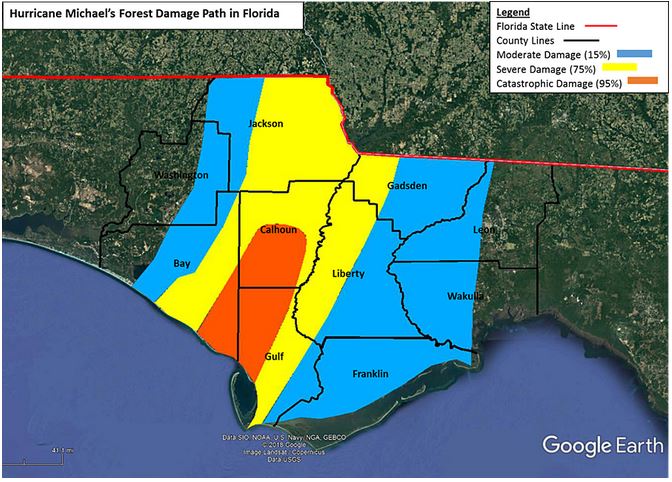

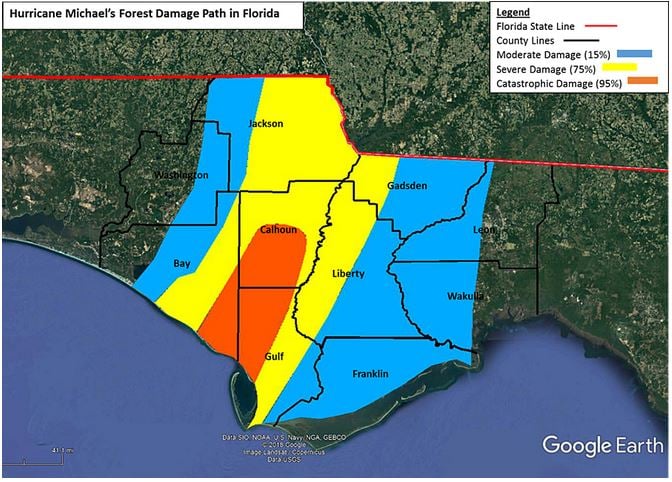

While Klausner never maximized its use of the local timber resource, the regional wood basket was ravaged when Hurricane Michael made landfall in the Florida Panhandle on October 10, 2018. The storm moved inland and quickly weakened over Georgia, but not before it caused $5 billion in agriculture and timber losses alone. Over 3.5 million acres of timberland were directly affected from Hurricane Michael. About half of these acres were impacted severely or catastrophically, meaning there was a 75% (severe damage) to 95% (catastrophic damage) total timber loss in these areas, which drastically changed the local timber market.

In the aftermath of Michael, the operational mills in the region that were most affected were forced to shift procurement strategies in a search for fiber outside of their immediate procurement zones. This created even more pressure in the Live Oak wood basin, resulting in an increase in demand and price volatility.

Event #2

Demand for the timber resource also created an additional concern when Georgia-Pacific (GP) announced the construction of its Albany, GA mill in 2018, which is also a facility capable of producing 300 MMBF/year. The mill is slated to come online in late 2020 and will bring roughly 1 million tons/year of pine sawlog consumption to the region.

As has been the case with Hurricane Michael, the impact on the Live Oak wood basin from the new GP facility will not be direct, as Albany is over 100 road miles away from Live Oak. However, with the new GP mill consuming a considerable amount of regional wood volume, procurement will reach far and will undoubtedly impact the Live Oak basin, resulting in an increase in demand/competition for its timber resources.

Event #3

It was reported earlier this month that the shuttered Klausner Lumber One facility will be put up for auction in Mid-August. It’s also reported that there is a fair amount of interest in the facility and conjecture that the mill could be up and running near the end of 2020. While this time frame for reopening is ambitious, as it’s expected the mill will need to be retooled before opening, the near-term demand from the regional wood basket will still be considerable.

With the lingering impacts of Hurricane Michael and now the potential of 2 million tons/year of log consumption impacting the region in the next several months, area timberland owners, investors and wood products manufacturers are all keeping a very close eye on these events as they unfold. There will be lots of uncertainty surrounding supply and price going forward in what is already a price-sensitive region.

Trends to Watch, Questions to Ask

Strong demand for pulpwood in the area has already caused many pulpwood consumers to reach into CNS-sized material when procuring fiber, which has helped to bolster demand for small logs and driven prices higher in the Georgia/Florida market. This shift in the market has also influenced traditional sawlog prices.

New demand driven by evolving markets and changing end-use products has made pine pulpwood a much more desirable raw material. And as demand for pulpwood has increased, the average price has increased in tandem with production volumes. There have been some periods of volatility since 2002 driven in part by the Great Recession and weather conditions, but pine pulpwood prices have continued to trend upward. As a result, this market has remained one of the higher-priced areas in the US South.

A significant amount of near-term, new demand coming online in the region will apply additional strain to the regional timber resource, which should prompt a number of concerns for regional manufacturers when new participant(s) enter the market. Questions that must be addressed include:

- What is the total volume of timber resources in the region?

- What is the makeup of those timber resources by type and age class?

- What is the growth rate and removal ratio of those timber resources?

- What is the current and projected competitive demand for the resources?

- What is the current and future sustainability of supply of the resources?

- What is the current and historical demand and price for the target materials?

- What is the forecast price for the target materials based on projected availability and demand by all consumers?

- How can I best prepare for a series of potential scenarios based on these developments?

For forward-looking consumers of wood fiber in the Georgia/Florida market, Forest2Market can answer these questions.

As a neutral, third party advisor, Forest2Market does not buy or sell timberland, timber or wood fiber of any kind; it does not manage timberland or provide credit wraps. Forest2Market is an independent source of wood and fiber supply chain expertise, and our extensive relationships and experience within the wood products industry provide us with unique insights into global markets.

- Complete, current and accurate market transactional data. The right set of data is the foundation upon which to build an effective long-term forecast. Forest2Market’s data is unique within the forest products industry, as it is the only comprehensive set of data that is collected at the transaction level; no survey data is used or incorporated. The depth and breadth of this data allows for unparalleled insight into wood supply chains, from the source to final consumption.

- A partner with detailed knowledge about ALL of the participants in the market. Forest2Market’s transactional data provides a full-spectrum view of market dynamics and includes information supplied by forest products companies, wood dealers, loggers, consultants and landowners.

- An advisor with the ability to conduct complex forest growth/yield and economic models. In order to accurately project availability, sustainability of supply and cost over the life of the project, a number of customizable tools and methodologies—as well as the ability to provide expert analysis of the results—must be utilized. Forest2Market has both the resources and the knowledge to provide expert guidance during the market transition process and thereafter.

Despite the volatile softwood lumber market, competition for wood fiber in the US South is taking place in pockets of high demand amid changing market preferences and an evolving forest products industry. Live Oak is one such pocket that is also in a region prone to severe weather disturbances, and a confluence of the events outlined above are poised to have wide-ranging impacts on the area’s timber resources in the future.