Joe Clark

Joe Clark

Regardless of location, wood feedstock costs are the single largest variable costs of wood-consuming manufacturing projects. As such, it is imperative to have a firm understanding of timber prices (stumpage) in a supply region not only during a site selection process, but also as an ongoing operating cost within that supply region.

Stumpage price—the price paid to a landowner for the right to harvest trees from the owners’ timberland—can vary dramatically across local wood basins. Within the US South alone, stumpage prices may vary significantly across state lines and even county-to-county within a relatively compact geographic proximity. (The market differences are even more stark when compared to the Pacific Northwest (PNW) region, for instance, where tree species, average log size, units of measure and harvesting practices are unique to the region.)

However, an analysis of US South timber sales data collected by Forest2Market indicates that increases and decreases in price are typically tied to one of 5 (and a half) primary factors that affect stumpage prices, regardless of where they fall within the wood basin.

- Competition: Wood basins are generally small in size and consist of a handful of counties. Depending on whether timber is located in a highly competitive or a marginally-competitive area, pine sawtimber prices can vary by as much as $20 per ton. Forest products companies procure wood from as close to their mills as possible, sometimes paying higher stumpage prices in order to have lower delivery costs. As a result, pricing can vary greatly within a relatively compact geographic distance.

- Inventory: Maintaining an adequate inventory level is vital to managing facility production, associated costs and overall supply chain productivity; optimizing the supply chain can save money and improve efficiencies. But when inventories run low, wood-consuming manufacturers are often forced to go out on the open market where they will pay a premium for wood, as this flexibility comes at a price. This strategy, while costly, ensures that a facility obtains the required volume to operate at its preferred production level. When mills are in a situation where they are paying a premium for wood, the loggers and wood dealers that supply the mill can pay higher stumpage prices to landowners.

- Seasonality & Weather: Wet weather makes it difficult for loggers to supply as many loads of wood per day as they could during dry times. Timber stands that fall within the “wet weather tract” category can be harvested year round and, because of their accessibility, will earn higher premiums. When supply becomes constrained, prices increase. Loggers shift production efforts to wet weather tracts during months that typically see higher rainfall amounts, and wood-consuming facilities pay higher prices to maintain inventory levels.

3.5 Extreme Weather Events: While seasonal weather patterns have a recurring impact on timber prices,

purchasers must also account for unforeseen, but plausible, extreme weather events like hurricanes, wildfires,

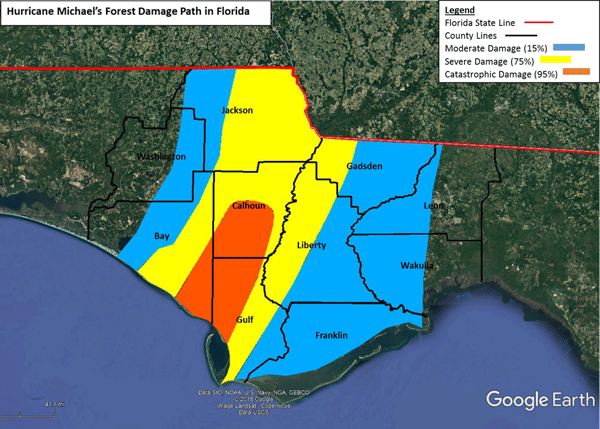

prolonged droughts, etc. that can have intense, lasting impacts on forest resources. For example, over 3.5 million

acres of timberland were directly affected from Hurricane Michael in 2018. About half of these acres were

impacted severely or catastrophically, meaning there was a 75% (severe damage) to 95% (catastrophic damage)

total timber loss in these areas. The remaining acres were damaged moderately, sustaining a roughly 15% total

damage. After an extreme weather event like Hurricane Michael, there will be both immediate and prolonged

shifts in procurement and harvesting activities, which will create increased price volatility that can last for years.

- Tract Size: The cost of transporting equipment from one tract to another is a major expense for loggers. Large size tracts of 200+ acres give loggers the opportunity to increase their weekly production by harvesting and hauling more loads per day. For this reason, tracts with more volume and acreage will often secure price premiums, especially if they include nearby access to quality roads.

- Tree Size and Quality: Pricing can often appear product-based when, in fact, the size of the tree is what ultimately matters. In general, pine logs fall into the following size categories: 5”-7” diameter at breast height (DBH) is pulpwood; 8”-11” comprises chip-n-saw, and logs that are 12” and larger are considered sawtimber. The per-ton value of trees generally increases in conjunction with log size. For example, sawtimber with a DBH of 18" commands a higher price than 12" sawtimber. Log quality can impact this, however. Lower-quality trees may be used in a less-expensive product class even though they reached the necessary DBH, so they command a lower price as a result. (Active forest management can have dramatic effects on timber quality as well.)

These ever-changing variables contribute to the complexity of the wood supply chain and marketplace. In order to better understand market price, it is important to thoroughly examine these factors in light of both short- and long-term risks and opportunities.

Forest2Market’s timber price database contains 20 years’ worth of transaction-level details from more than $6 billion in timber sales that includes 15.5 billion data points, including price and volume by timber class (pulpwood, chip-n-saw, sawtimber, etc.), weather conditions, tract size, timber quality and much more. As a result, we maintain the only database of actual timber transactions in the global forest supply chain. The depth and breadth of this data allows for unparalleled insight into wood supply chains, from the source to final consumption.