Joe Clark

Joe Clark

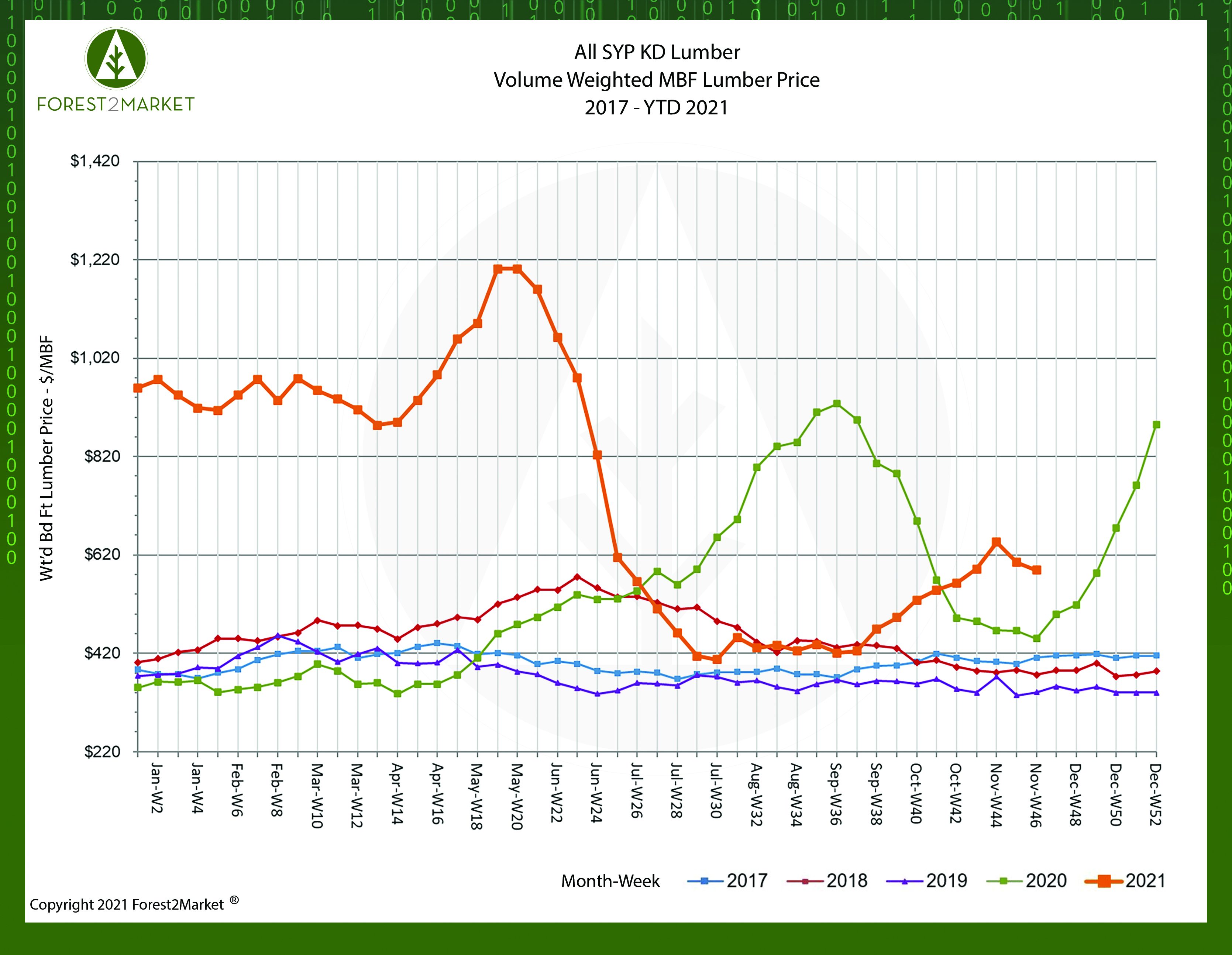

After cresting $1,200/MBF in mid-May, North American softwood lumber prices retreated swiftly. Over the course of the following eight weeks, prices for finished southern yellow pine (SYP) lumber plunged 66% before bottoming in late July; prices stood largely flat for the remainder of the summer. But by mid-September, the market began to creep higher on a weekly basis—a trend that lasted for another eight consecutive weeks as lumber prices surged 58% off the bottom.

In a departure from the steep surge in week-over-week pricing that developed in 4Q2020, prices for lumber reversed course sharply in mid-November. Forest2Market’s composite SYP lumber price for the week ending November 19 (week 46) was $589/MBF, a nearly 10% decrease from just two weeks prior.

Other price trends observed thus far in 2021 include:

- 1Q2021 Average Price: $941/MBF

- 2Q2021 Average Price: $967/MBF

- 3Q2021 Average Price: $451/MBF

- 4QTD Average Price: $590/MBF

Is SYP lumber now headed back toward a more traditional floor price that better reflects current demand, or is this just a temporary dip?

An Unsteady Market

The 2021 lumber market might best be described as an extended game of “chicken” between lumber producers and purchasers. In such a standoff, something eventually has to give.

As Fortune recently wrote, “Simple economics popped the lumber bubble: Once wood prices got up 300% above their pre-pandemic levels, buyers refused to buy. But as prices started to plummet this summer, buyers didn't rush back in. However, once prices bottomed out this summer, buyers finally returned. That pent-up demand coming back into the market… is helping to drive up the price.”

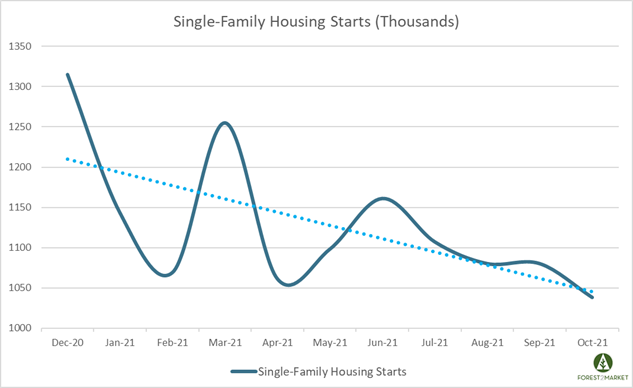

While home sales remain strong despite the higher prices, there are signs that headwinds are beginning to impact the larger housing market. After bottoming during the peak of the pandemic lockdowns in April 2020, single-family housing starts (which require the most lumber) bounced back quickly before cresting in December. Since then, however, single-family starts have been on a steady downward trend as illustrated in the chart below.

A couple of dynamics are now coalescing to further influence North American lumber prices.

- As an indication of how shortages of all building materials and labor are making it tough for builders to finish projects, the number of new house completions in October was unchanged from the prior month, which represents the lowest seasonally-adjusted level in over a year. Affordability, labor and materials challenges are being further exacerbated by supply chain and inflationary pressures, and new homebuilding simply doesn’t have much room for expansion in the current environment. The median new home sale price in October was up +18.7% MoM to a new record of $408,800, and rising mortgage rates could also become a challenge for the market in the coming months if some home buyers are priced out at the margin.

Looking a bit further down the road:

- A provision in the budget-reconciliation bill presently being considered by Congress has the potential to dramatically curtail real estate investment. “Real estate is a long-term, risky and labor-intensive investment compared with stocks and bonds,” wrote analysts Dan Palmer and David Williams in the Wall Street Journal. “Without tax incentives, real estate can’t compete with other investments for essential capital” since the proverbial investment “playing field” is not level.

- Under the House bill, taxation of real-estate operating profit (i.e., ordinary income) as well as real estate capital gains would soar above current rates. Concurrently, new limitations would be phased in to reduce mortgage-interest deductions and depreciation.

- A provision in the budget-reconciliation bill presently being considered by Congress has the potential to dramatically curtail real estate investment. “Real estate is a long-term, risky and labor-intensive investment compared with stocks and bonds,” wrote analysts Dan Palmer and David Williams in the Wall Street Journal. “Without tax incentives, real estate can’t compete with other investments for essential capital” since the proverbial investment “playing field” is not level.

Taken together, these events have the potential to significantly limit new homebuilding — and lumber demand — in the near-term. Longer term, these developments could hobble the larger housing market and, as we know from the Great Recession in 2008, forced selling in real-property markets also creates havoc in financial markets.

- US softwood lumber consumption was up 5% YTD through August, but there is currently no major gap in supply like we saw during much of 2020 and into early 2021. In fact, YTD through August, US softwood lumber production was up 3%, total imports were up 15%, and MoM inventory levels remained higher than they were last year. This suggests that available lumber supply is now more in balance with demand patterns, which should limit substantial price reactions in either direction.

However, recent trade developments have the potential to disrupt the flow of lumber from Canada. The U.S. Department of Commerce recently said it will proceed with plans to impose duties of nearly 18% on softwood lumber imported from Canada, which is twice the previous rate of 9%. (18% is the average rate; individual producers may pay higher or lower duties.) It is too early to get a feel for how this change will impact US homebuilding but one thing is certain: the American consumer will ultimately pay for higher tariffs, which in this case might result in even higher new home prices.

While softwood lumber prices nearly hit $650/MBF in October, they are now trending back down. As I wrote last month, I don’t believe we’ll see a repeat of the lumber price run-up that developed in 4Q2020. But over the next several months, I believe lumber prices will continue to demonstrate some volatility around a new floor price that is now above the $500/MBF mark.