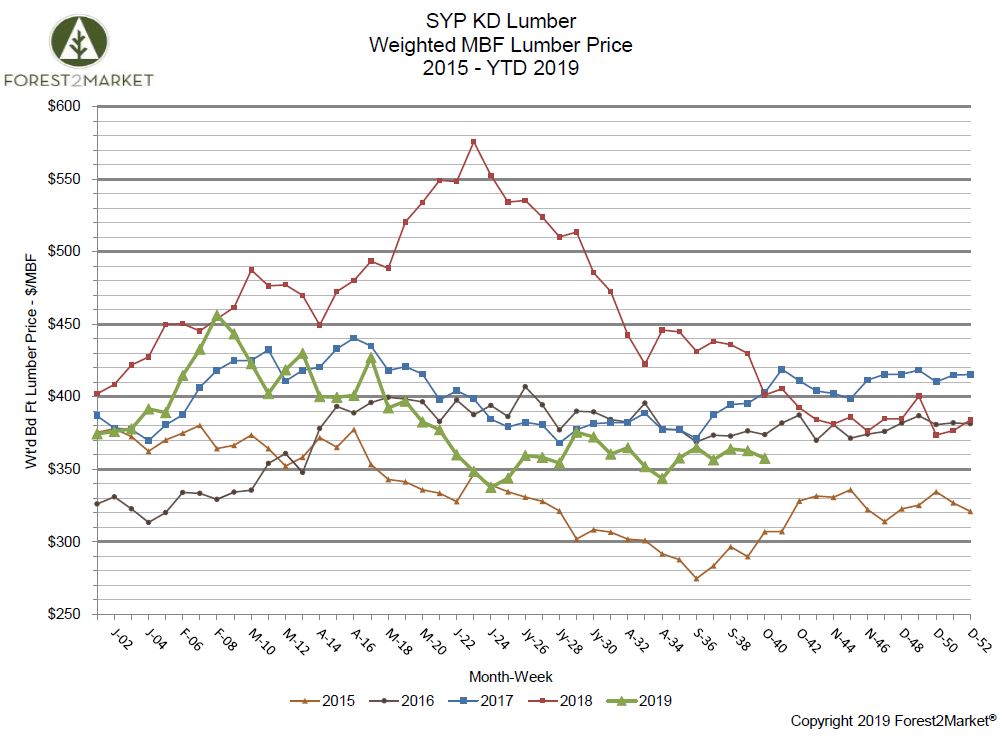

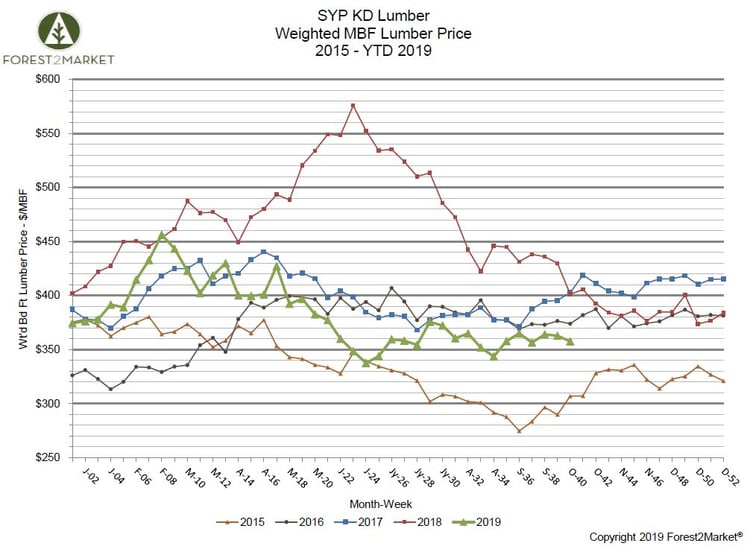

Southern yellow pine lumber prices have been relatively flat since the beginning of September, despite housing starts posting a 12-year high during the previous month. Price volatility has been minimal over the last six weeks, staying within a range of roughly $7.

Forest2Market’s composite southern yellow pine lumber price for the week ending October 4 (week 40) was $358/MBF, a 1.4% decrease from the previous week’s price of $363/MBF, and a 10.7% decrease from the same week in 2018. Price performance has decreased incrementally by quarter during 2019:

- 1Q2019 Average Price: $410/MBF

- 2Q2019 Average Price: $379/MBF

- 3Q2019 Average Price: $361/MBF

- YTD Average Price: $383/MBF

What’s Driving the Market?

While the Trump administration recently delayed most of the tariffs it planned to impose on Chinese goods and dropped other tariffs altogether, global markets nevertheless seem spooked by rising levels of uncertainty coupled with mixed economic signals.

- Forbes recently reported on the paradox emanating from current employment data: “You might have noticed, in the last several months, that a curious trend has begun to take place in economic news. Unemployment has hit a fifty year low - the last time it was this low, 3.7%, was in 1969, when the big news was not the economy but the Vietnam War. Yet if you are paying attention to the job payroll numbers, you may also have noticed that the number of new jobs created has been dropping slowly but steadily to 136,000 in September (compared to the average of about 250,000), with both July and August numbers also revised downward.”

- The U.S. manufacturing index from the Institute for Supply Management (ISM) fell to 47.8% for September—its lowest level since June 2009—marking the second successive month of contraction. (Any reading below 50% signals a contraction.)

- A surprise move by the Federal Reserve in late September resulted in a 0.25% rate cut to the federal funds rate in what was just the second rate reduction over the last 11 years; the other took place after the last Fed meeting on July 31. There are whispers that an additional rate cut could come as early as late October.

- Wall St. is developing a serious case of the jitters as we approach a major election year. As MarketWatch noted, “… while a majority of investors say that a victory next November by former Vice President Joe Biden — who held a commanding lead in pre-primary polls until recently — would be neutral for markets, 89% of respondents said a win by a Democrat other than Biden would be ‘bearish or very bearish’ for U.S. equities.”

"Why is this important? Unlike Biden, [Elizabeth] Warren is not an internationalist free-trader. Her platform of ‘economic patriotism’ stipulates countries that trade freely with the U.S. must uphold international labor standards, protect human rights, and [meet] environmental requirements,” he [Thierry Wizman, strategist at Macquarie] wrote. ‘Clearly, this would not favor building on U.S. trade ties with China, nor removing Trump-era tariffs on China.’” - The increased pressure via an impeachment inquiry by House Democrats is creating palpable concern for the political direction of the country moving forward. “House Democrats on Monday issued subpoenas for documents from the Pentagon and White House budget office as part of their rapidly expanding impeachment inquiry into President Donald Trump,” noted Politico.

After three years of solid growth, the challenges posed by the uncertainty outlined above are significant enough to cause even the most ardent economic optimist to take pause. However, it is encouraging that SYP prices have remained largely flat throughout these developments over the last couple of months.